Other reviews from this season to read:

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Sea Limited

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Table of Contents

a. Key Points

- Spending on growth.

- AI investments are already bearing fruit.

- A lot of credit data and margin noise this quarter.

- Reaching net income breakeven in Mexico ahead of schedule.

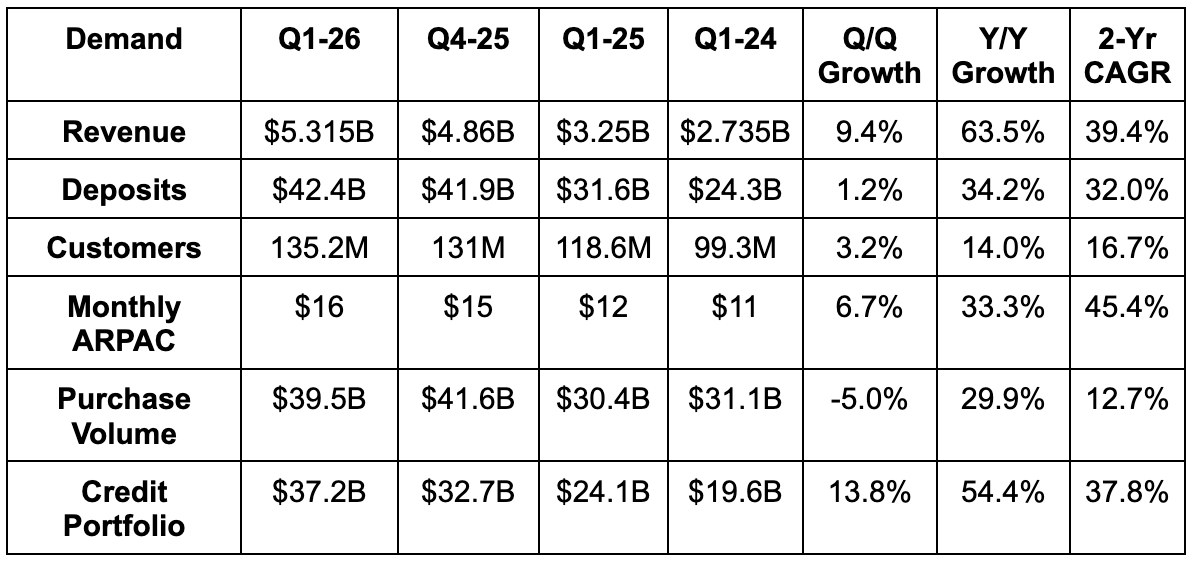

b. Demand

- Beat revenue estimate by 5.5%.

- Beat 135M customer estimate by 200K.

- Missed purchase volume estimate by 1%.

- Missed deposit estimate by 3%.

As discussed last quarter, NU introduced a managerial income statement alongside their standard IFRS income statement. This is because, under IFRS, some revenue items are reported pre-tax and some post-tax. The managerial revenue number adds back certain taxes to create a better picture of what products are driving growth. The managerial revenue number is the number they put at the beginning of the press release and they celebrated crossing $5B in revenue for the first time (accounting revenue # was $4.97B) so managerial revenue is the metric they’re focused on.

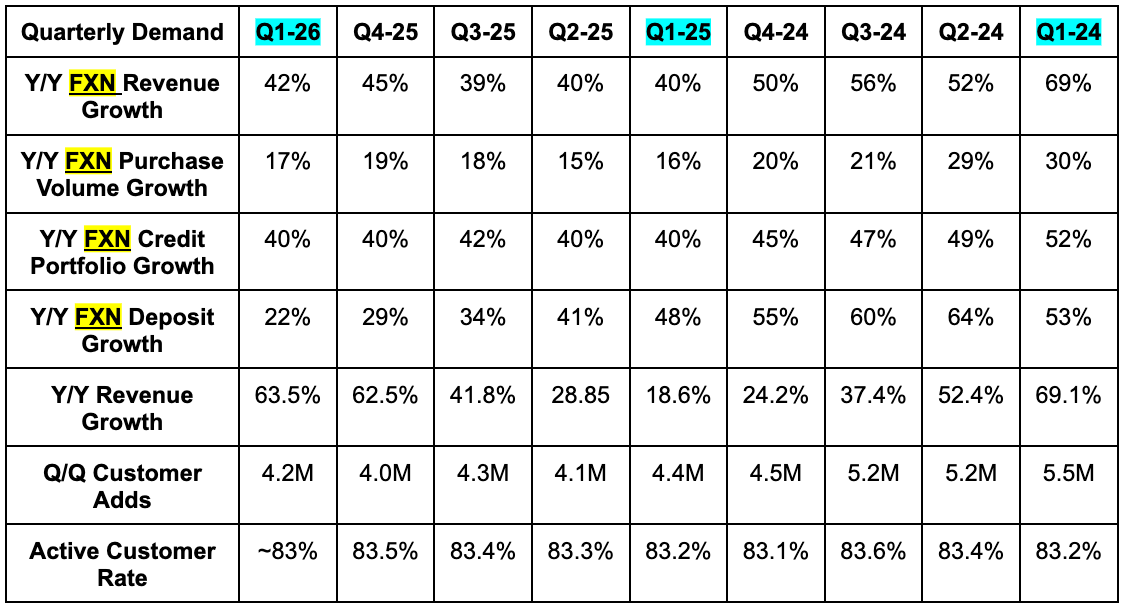

Quick note on active customer rate. They said it expanded sequentially but also said it was 83%. I just left it at 83% despite the other language indicating it might be higher.

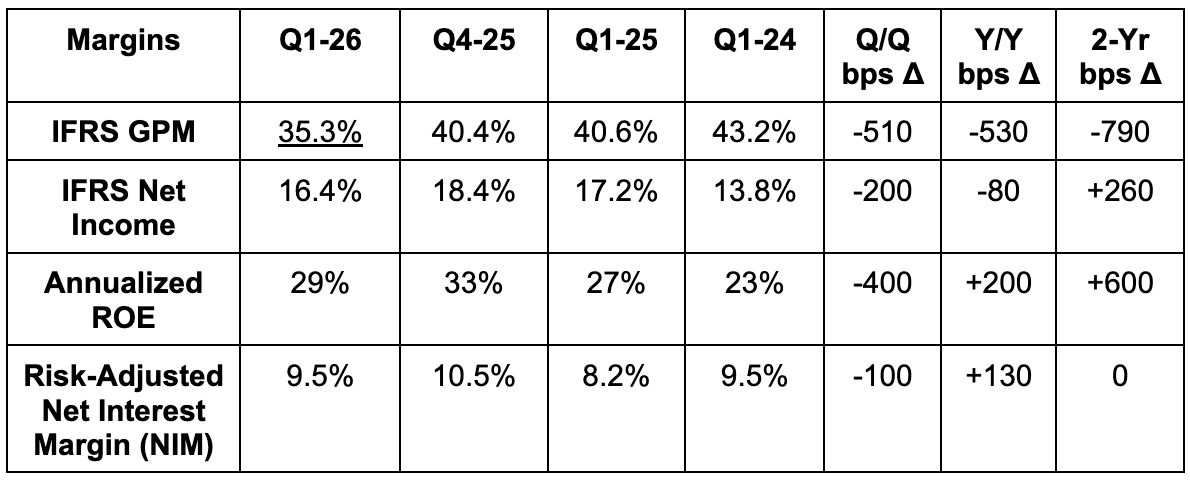

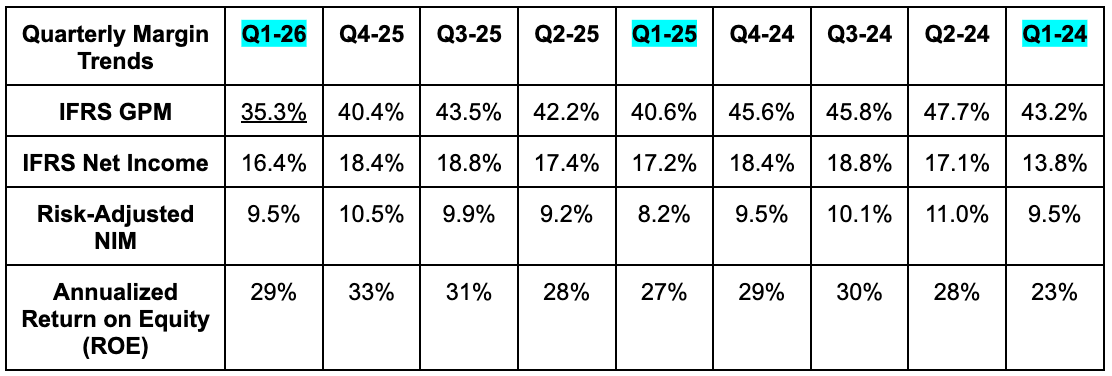

c. Profits

- Missed 43.8% GPM estimate by basis points (bps; 1 basis point = 0.01%).

- Missed $928M net income estimate by 6%.

Gross profit was heavily impacted by rapid credit growth and expansion to riskier cohorts amid rising underwriting confidence. Riskier cohorts do not bother me as long as the risk is priced correctly. If this sounds exactly like MELI’s fintech performance to you, you’re right.

As I often talk about, Brazil and Mexico are two of the most attractive financial service markets on the planet. They feature a blend of large populations with higher GDP per capita than many areas of the world, familiarity with smartphone and internet usage, and relatively low adoption rates to capitalize on. Right now, this means heavy, heavy front-loaded provisioning for credit issuance, which makes GPM look temporarily ugly along with material hits to risk-adjusted net interest margin (NIM) and return on equity (ROE). They clearly communicated their plans to do this three months ago, as the company embarked on a 4-6 quarter investment phase to fortify their positioning and turbocharge global expansion. No surprises here.

Last quarter, we were told the efficiency ratio (non-interest OpEx / revenue) progress consistently seen over the last several years would temporarily pause to incur costs associated with employees returning to office international expansion and AI investments. These worsened the efficiency ratio for the quarter by 100 bps. Despite that, the efficiency ratio for the quarter came in at 17.6% vs. 21.4% Y/Y. This unexpected progress helped offset some of the temporary GPM weakness. This was related to two items. ⅓ of the impact was via structural AI efficiency gains that are not a one-off event. The rest was related to cost timing that will normalize throughout the year. This will lead to 2026’s efficiency ratio still coming in relatively unchanged Y/Y at 20%. I expect improvements to resume in 2027 (unless the U.S. debut goes amazingly well) and support more net income margin expansion. As we’ll see later in the piece, there are other GPM-level tailwinds that will help neutralize the remaining 2026 OpEx headwind.

One more thing to note. They expect the losses associated with international expansion to be somewhat offset by lower tax bills that will buffer some of the net income hit. This should allow net income to keep steadily growing in the near-term.