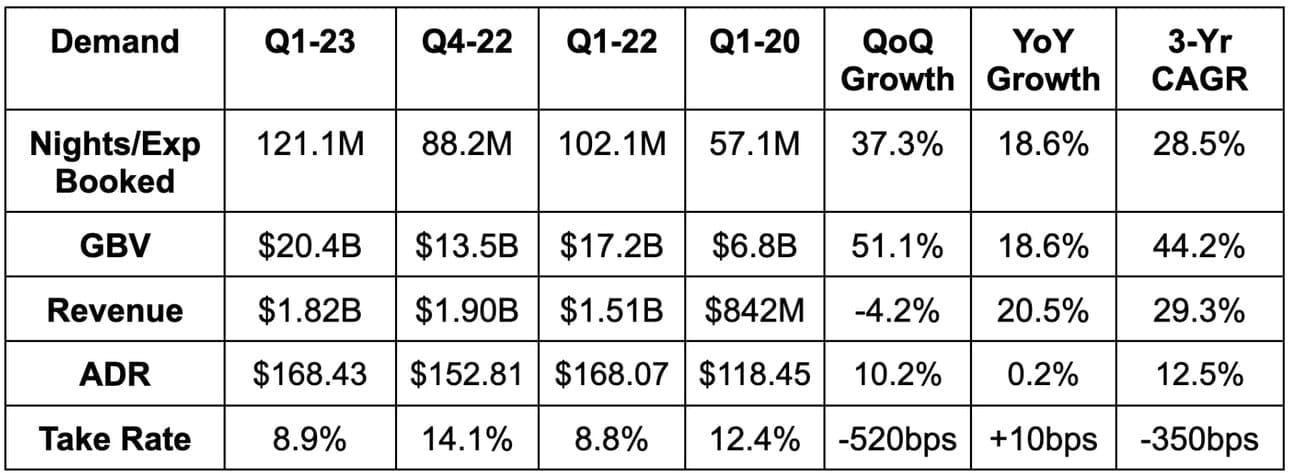

1. Demand

- Beat revenue estimates by 1.7% & beat its guidance by 1.7%.

- Beat gross booking value (GBV) estimates by 1.5%.

- Roughly met abstract nights booked guidance and slightly missed estimates.

Demand Context:

- 90% of Airbnb’s traffic continues to be direct and unpaid. It’s great to be a verb.

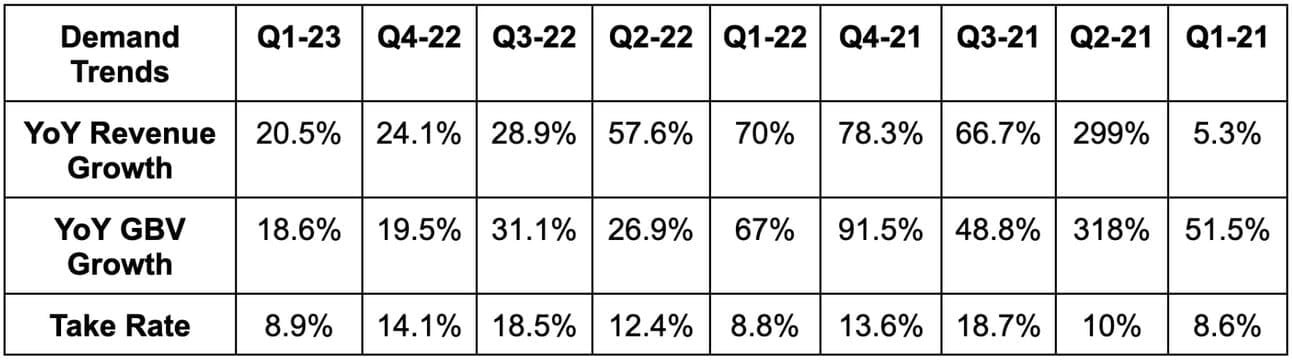

- Very easy 3-year pandemic comps this quarter. That’s also why Q1 2021 - Q2 2022 saw growth far outpacing the company’s long term trend.

- Q1 is seasonally weak for take rate and revenue with that seasonality absent the last few years due to strange pandemic comps. It has now normalized.

- Supply growth has now accelerated in every quarter since Airbnb went public. Supply rose 18% YoY vs. 16% YoY last quarter. This is a major key to any sustainably healthy marketplace. It helps mightily with controlling nightly rates thanks to less listing scarcity which, in turn, juices demand. Active bookers set a new record high to balance this accelerating supply growth with robust demand.

- Both urban and non-urban supply was up 18% YoY.

- High density urban nights booked rose 20% YoY. Urban nights represented 48% of total vs. 46% YoY.

- North American cross border nights booked growth accelerated from 31% YoY last quarter to 34% YoY this quarter. Overall cross-border nights booked rose 36% YoY as global travel makes a comeback.

- Cross border = 45% of total nights booked vs. 39% YoY and 51% pre-pandemic.

- Revenue FX neutral (FXN) growth was 24% YoY.

- ADR FXN growth was 3% YoY.

- Latin America is its fastest growing region with nights booked up 2x since pre pandemic.

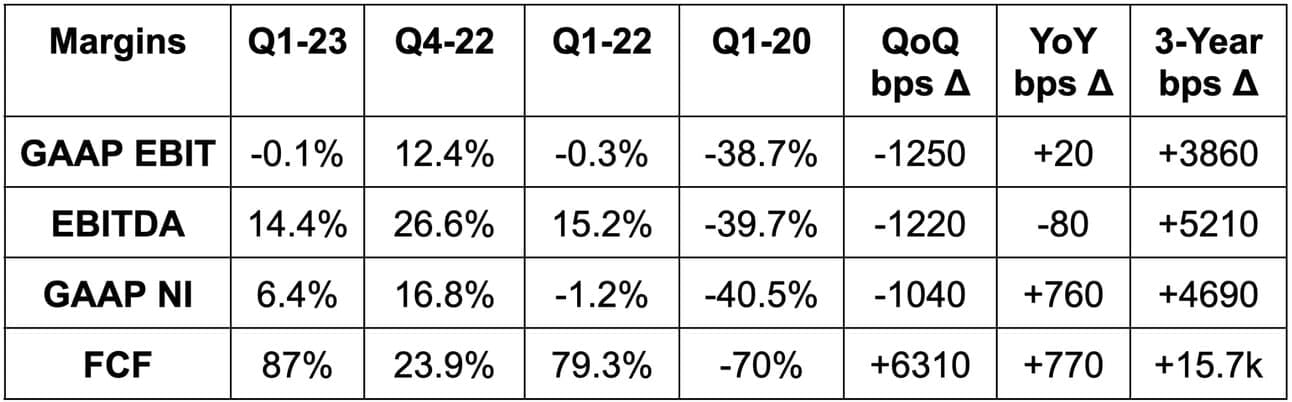

2. Profitability

- Beat EBITDA estimates by 1% & beat its guidance by roughly 0.8%.

- Beat -$10.6 million GAAP EBIT estimates by $5.6M.

- Beat $0.10 GAAP EPS estimates by $0.08.

- Beat FCF estimates by 55%. There were other consensus estimates from different sources that Airbnb beat by a much wider margin.

More Margin Context:

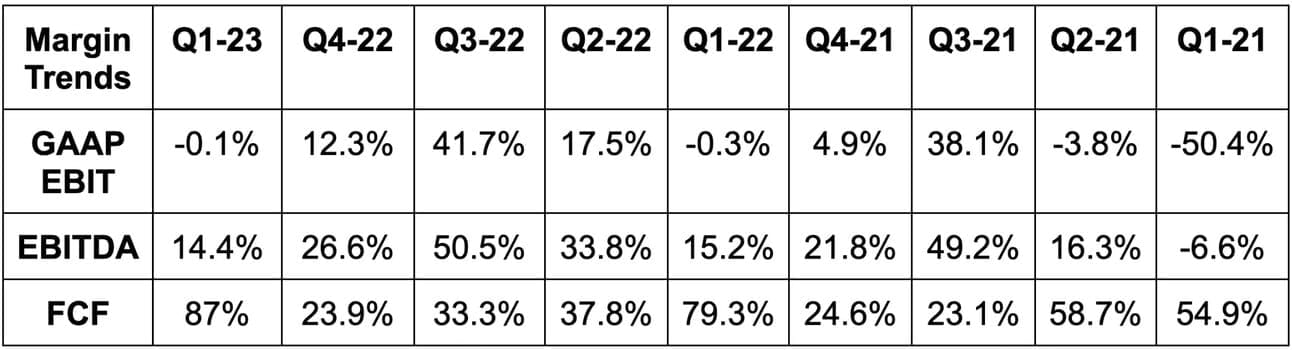

- Airbnb has rapidly morphed into a FCF machine. Its trailing 12 month FCF margin is 44%. HOWEVER, Q1 is always its best FCF quarter due to collection on unearned fees from bookings to take place throughout the year. An 87% margin should not be extrapolated for future quarterly estimates.

- Net income is better than EBIT due to interest income. This revenue bucket helped Airbnb generate its first positive net income Q1 ever.

3. Balance Sheet

Airbnb tore through its $2 billion buyback program in under a year thanks to rapidly growing FCF generation. So? It added a new $2.5 billion buyback program this quarter. Buybacks this quarter were more than double stock compensation dollars and diluted shares fell slighty YoY.

It has $10.6 billion in cash and liquid assets and nearly $2 billion in long term debt.