a. Demand

Lemonade guided to the following:

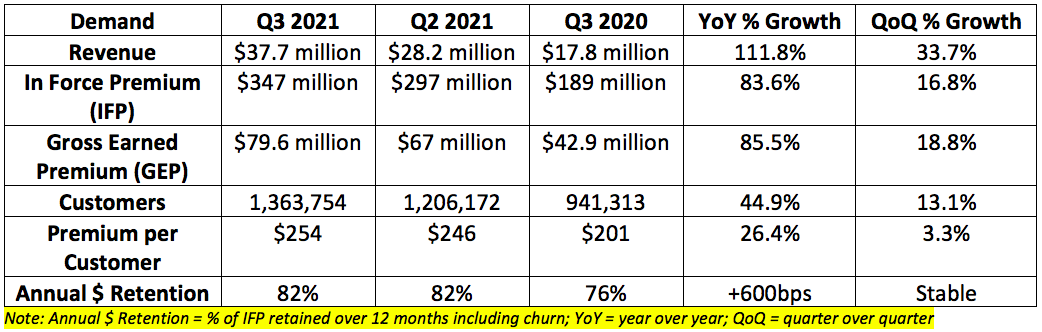

- $32.5-$33.5 million in revenue. It posted $37.7 million beating the midpoint by 14.2%.

- $336-$339 million in IFP. It posted $347 million beating the midpoint by 2.8%

- $76.5-$77.5 million in GEP. It posted $79.6 million beating the midpoint by 3.4%

13.1% sequential customer growth accelerated briskly vs. 10% sequential customer growth last quarter. Lemonade continues to enjoy healthy net customer additions each quarter:

b. Profitability

Lemonade was expected to lose $1.16 per share. It lost $1.08 per share beating expectations by $0.08. It was also expected to lose $53.4 million in adjusted EBITDA. It lost $51.3 million beating expectations by 3.9%.

*Note that last quarter’s gross loss ratio was severely impacted by the Texas Freeze. This made the sequential comparison uniquely easy and should be taken with a grain of salt.

The adjusted gross profit margin decline during the quarter is due to the higher YoY loss ratio as its newer products proliferate — newer products initially come with higher loss ratios. The loss ratios and unit economics on its original renter product both continue to improve but that segment is also (encouragingly) becoming a smaller piece of the business.

The adjusted gross margin still compares extremely favorably to the 21.1% it posted in the same period for 2019 — this is partially due to the same accounting change that hurt revenue growth for the last 4 quarters but also due to improving unit economics.

c. Guide Updates

Lemonade guided to the following for the 4th quarter:

- $380-$384 million in IFP

- $88-$89 million in GEP

- $39-$40 million in revenue (1.2% ahead of analyst expectations)

Lemonade directly addressed the worsening EBITDA outlook in the shareholder letter and explained the change with the following reasons:

- Conservative assumptions on how quickly marketing efficiency recovers.

- Pulling forward 2022 operating costs to support its accelerated car launch timeline (now with 49 state licenses and Metromile’s data in hand). All customer facing teams have been staffed ahead of launch for car to train and prepare them for all the expected growth.

d. Lemonade is Buying Metromile

Lemonade is buying Metromile — a car insurance-technology company — in an all stock deal for an equity valuation of $500 million fully diluted or just over $200 million when netting out Metromile’s cash.

Lemonade was especially interested in Metromile’s expertise with telematics and precision sensors and all of the data coming from the 400 million road trips these sensors have taken. Metromile is a trailblazer in leveraging its customer’s training data to predict losses per mile driven. The tangible result is Metromile customers saving 47% by switching to it with loss ratios within 10% of GEICO and Progressive. It even lowered its user’s premiums by 16.2% in real-time during 2020 to adjust to lower driving rates and to avoid overcharging — talk about refreshing.

This savings and fairer pricing is powered by embracing pricing based on precision (tracking and recording data on driving behavior) rather than proxies (credit scores and marital states). With an estimated 2/3 car insurance customers paying 30% too much in premiums, this downward cost pressure is important. Despite telematics driving so much savings — or perhaps because of it — 96% of incumbent car policies do not use any sensors at all with the remaining 4% generally underweighting the signals.

Lemonade’s own brand-new car product does leverage telematics to help quantify risk — but it’s a newbie in this endeavor and competing in a dauntingly competitive space. Metromile’s more established product here — in the words of Co-CEO Daniel Schreiber — “will vault Lemonade over the most time and cost intensive parts of the journey.”

It would’ve taken Lemonade years to scale its auto business to get it to a point of maturity where loss ratios were competitive — this purchase allows Lemonade to avoid that growing pain process. With these acquired assets, Lemonade jumps from merely embarking on aggregating and analyzing data to better quantify loss per mile to being a seasoned veteran in doing so overnight.

“The riskiest 5% of drivers are 10X more likely to crash [vs. the average]. Most insurers can’t tell who is who but Metromile is able to identify these drivers with unrivaled precision. This deal allows us to skip over the riskiest part of our car ambitions: growing Lemonade Car before our data models season.” — Daniel Schreiber