Table of Contents

- a. Key Points

- b. Demand

- c. Profits & Margins

- d. Balance Sheet

- e. Guidance & Valuation

- f. Call & Release

- g. Take

a. Key Points

- Fantastic subscriber growth was driven by broad-based content success.

- Margin outperformance is a direct byproduct of outperforming revenue.

- It’s raising annual guidance despite incremental foreign exchange (FX) headwinds.

- Ad-based subscribers are on pace to reach critical mass this year.

- Expansion beyond the core content niche is going well across the board.

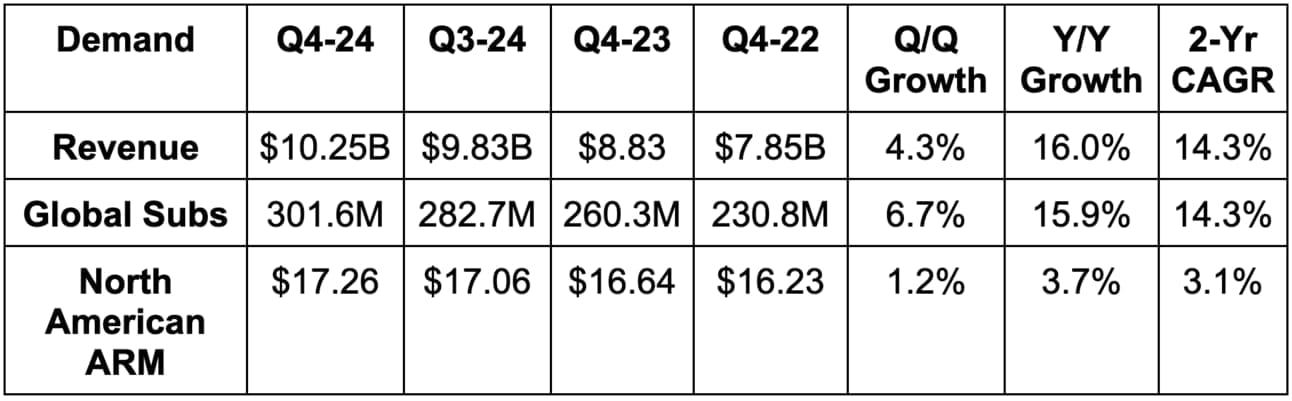

b. Demand

- Beat revenue estimates by 1.5% & beat guidance by 1.2%. Again, this was despite foreign exchange (FX) headwinds that materially worsened during the quarter and so far in Q1. More later.

- Beat 17% FX neutral (FXN) growth guidance with 19% Y/Y FXN growth.

- Overall average revenue per member (ARM) rose 1% Y/Y and 3% Y/Y FXN.

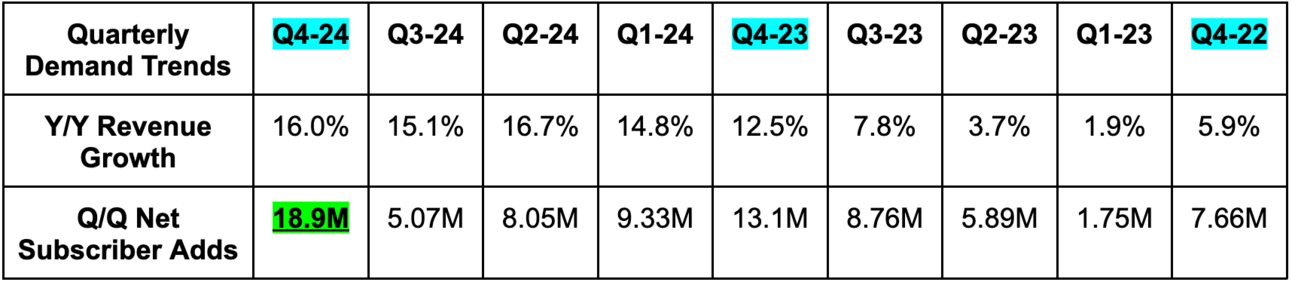

- Nearly doubled net new sub estimates.

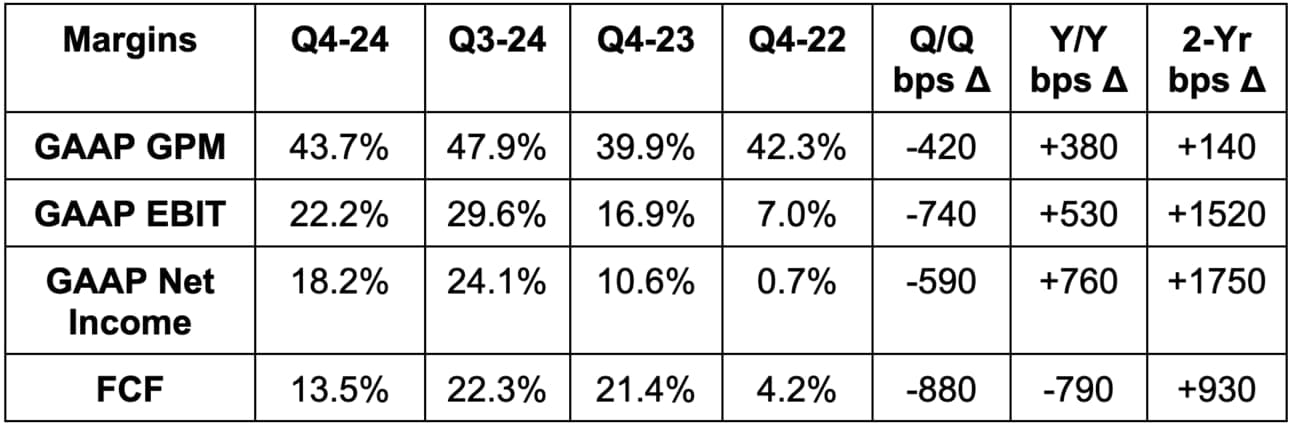

c. Profits & Margins

- Beat EBIT estimates by 2.4% & beat guidance by 3.8%. EBIT outperformance was encouragingly driven by revenue outperformance rather than less compelling factors like content spend timing or cost cutting.

- Beat FCF estimates by 30%. FCF is very lumpy on a quarterly basis, as it is tied to content spend timing. While the beat was strong, I think it’s best to focus on annualized FCF generation.

- Beat $4.20 GAAP EPS estimates by $0.07 & beat guidance by $0.04.

d. Balance Sheet

- $9.6 billion in cash & equivalents.

- $15.7 billion in total debt.

- Share count fell by 1.5% Y/Y.

e. Guidance & Valuation

For Q1, revenue guidance missed by 0.7%, EBIT guidance missed by 5.8% & the $5.58 EPS guide missed by $0.39. Q1 weakness came from timing of price hikes and advertising seasonality. To make this even less concerning, the full year guide was quite good:

For 2025, Netflix raised revenue guidance by 1.1%, which beat expectations by 0.9%. This would be positive regardless of the macro backdrop, but it’s even more impressive when considering that context. Since the company’s most recent guidance, FX headwinds have led to an incremental $1 billion in revenue headwinds after hedging. Without this, annual revenue guidance would have been raised by 3.2%. FX headwinds also negatively impact its profit generation. But? It still raised annual EBIT margin guidance from 28% to 29%, which beat 28.4% margin estimates by 60 basis points (bps; 1 basis point = 0.01%). In EBIT dollar terms, this represents a 4.9% raise to previous guidance and a 3.2% beat vs. consensus estimates. Finally, its $8 billion FCF guide missed estimates by $800 million. This guide includes $800 million in unique tax charges mentioned for the first time this quarter. Without this headwind, FCF guidance would have met estimates.

There was some skepticism from a few people about how this annual guidance could be so positive while Q1 was slightly negative. Are they just too optimistic about Q2-Q4? I don’t think so. I think the timing & taxation items make a lot of sense here. I also don’t get worried about this quality team effectively guiding results. They love to underpromise and also run a subscription business with fantastic churn dynamics and decades of operating history. Visibility should be as good as it has been in previous years. If there’s a risk to this annual guide, it’s more likely to the upside than the downside.

Other 2025 guidance notes:

- Continues to expect 100% Y/Y advertising revenue growth.

- Demand will be powered by mostly member growth and a bit of ARM growth.

- This was the last quarter that Netflix will disclose members every 3 months. Going forward, it will mention milestones and publish a twice-per-year engagement report. The first will come in Q2.

EPS is expected to compound at a 20% clip for the next two years. FCF is expected to compound at a 27% clip for the next two years. Estimates should rise in the coming days following these results.