Today’s Piece is Powered by Savvy Trader:

In case you missed it, the following content was published during the week:

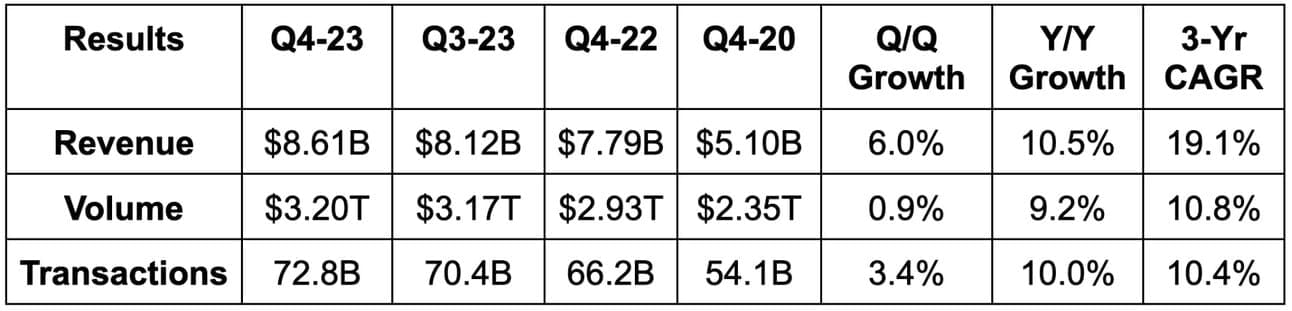

1. Visa (V) — Earnings Review

a. Demand

Visa beat revenue estimates by 0.7% & beat its guidance by 0.5%. Its 19.1% 3-year revenue compounded annual growth rate (CAGR) compares to 18.8% Q/Q & 11.0% 2 quarters ago. For the full year, revenue roughly met guidance.

b. Margins

Visa beat $2.24 GAAP earnings per share (EPS) estimates by $0.09. That represents about 21% Y/Y growth and 3-year EPS compounding of 27.7%. For the full year, EPS rose by 17% which met loose guidance.

c. Balance Sheet

- $20 billion in cash & equivalents.

- $20.5 billion in total debt.

- Dividend payments rose 17.1% Y/Y.

- Share count fell 2.1% Y/Y. It bought back $12.1 billion in stock for fiscal 2023 vs. $11.6 billion Y/Y.

- Visa added another $25 billion in buyback capacity. Pristine balance sheets are a wonderful thing.

d. Guidance

Visa sees fiscal year (FY) 2024 as being the most “normal” year that it’s had in a while. That was interesting to hear. It has lapped variant comps and the exit of Russia while inflation “continues to moderate” across core markets. Its outlook currently assumes no recession in 2024, and also no headwind from the resumption of student loan payments. It hasn’t seen any material impact to date from these payments restarting.

For the full fiscal year, Visa expects low double-digit revenue, volume and transaction growth, roughly 10% operating expense growth and low teens EPS growth. All of this was better than expected. Through the first 3 weeks of October, U.S. payment volume growth slowed to 5% for both credit and debit. The fall from 6% in September and this past quarter is mainly due to fuel disinflation.

Growth is expected to be the slowest in Q1 and to accelerate throughout the year. In the first quarter, revenue growth is expected to be 6%-7% with operating expenses (OpEx) rising in the “high single digit range” and EPS rising ~10% Y/Y.

e. Call & Presentation Highlights

Macro:

There are few companies in the world with a better sense of consumer health than Visa. According to leadership, consumer spend “across all segments” has been remarkably stable all year. Its data “indicates no behavior changes across consumer segments.” Volume growth even accelerated throughout the quarter. Again, it did slow into October, but that was via welcomed fuel disinflation.

Partnership Momentum:

Visa continues to rapidly add to its list of financial institution and enterprise partners. New FinTech deals rose 25% Y/Y while transit system deals rose 30% Y/Y. Importantly, 40% of the transit system deals include multiple value-add services. These high margin software upsells bolster the overall unit economics of Visa while lowering churn.

Visa Connect is its product connector between bank and FinTech partners to enhance access to digital-first tools. It enjoyed 70% Y/Y bank client growth. Transactions under this program doubled Y/Y.

This quarter, Visa signed an agreement with Tencent for cross-border and its peer-to-peer payments product called Visa Direct. The deal brings Visa Direct’s “wallet endpoints” to 2.5 billion.

Visa renewed its credit contract with Shinhan Card (largest issuer in Korea). Shinhan also added cross-border and data analytics services as part of the agreement. It also inked a new Citibank deal in 60 countries for a commercial business card and 20 value add services. Relatedly, IBM will use Visa (and Citi) for its new commercial card.

Finally, Visa renewed its U.S. Bank agreement while adding consulting and co-marketing products to the deal. Along those lines, Visa’s largest clients continue to utilize more of its products. As of this quarter, its largest cohort uses 22 Visa products, which is up 8% Y/Y. The more they use, the longer they’ll likely stay and the more revenue they’ll generate.

- New Nequi partnership in Colombia enables the “first digital wallet there” to tap-to-pay.

- New epiFi partnership in India to target high net worth individuals with consumer credit products.

- New Razer Pay partnership to allow debit card holders to directly buy bonds and mutual funds.

- Renewed its contract with Shopify for its merchant credit and debit tools.

- Its CyberSource (fraud and security management) segment closed deals with 2,600 clients this year including Costco and Alaska Airlines.

Growth Metrics:

- Y/Y Volume growth:

- 9% growth globally vs. 9% growth last quarter and 10% growth 2 quarters ago.

- 6% growth in North America vs. 6% growth last quarter.

- 11% growth in Rest of World vs. 12% growth last quarter

- 18% cross-border ex-intra Europe growth vs. 22% growth last quarter.

- Commercial payment volumes rose 12% constant currency Y/Y.

- Visa Direct saw 19% Y/Y growth in transactions and 30% Y/Y growth ex-Russia (where it exited last year).

- Card-not-present growth of 9% Y/Y compares to 3% Y/Y card present growth. This divergence depicts e-commerce and service-based spending enjoying easier Y/Y comps vs. brick and mortar shopping.

FedNow:

Visa is now a certified provider for the FedNow program. This means its institutional clients can use FedNow and the Visa network to transmit funds in real time.

Travel:

Visa’s travel index vs. 2019 levels actually improved Q/Q. Travel volumes rose by a robust 26% Y/Y for the quarter. It continues to enjoy healthy travel growth across most of the globe. Outbound travel from Mainland China has been the slowest to recover, but is now showing signs of life.

f. Take

Like Bank of America, JP Morgan and Mastercard (as we’ll see below), this quarter points to continued consumer resilience. People are still spending. While loss rates are creeping up, they’re still under 2019 levels for non-sub-prime credit bands. Consumer balance sheets are in worsening, but still good shape and that will likely remain the case while the employment market remains so strong.

Considering consumer spending is over 70% of North American GDP, this should mean continued economic resilience overall. While that may mean one more rate hike or a longer pause, it should also mean a more favorable demand backdrop than some seem to think.

2. Mastercard (MA) – Earnings Review

a. Demand

Mastercard met revenue estimates and roughly met its revenue guidance. Purchase volume of $1.88 trillion also slightly surpassed expectations. Cross border growth met estimates. Its 19.4% 3-year revenue CAGR compares to 23.4% Q/Q & 12.8% 2 quarters ago.

b. Margins

Mastercard beat EBIT estimates by 0.4% and beat $3.23 GAAP EPS estimates by $0.16.

c. Guidance

For next quarter, Mastercard guided to low double digit revenue growth vs. 13.3% Y/Y growth expected. This includes a 50 bps foreign exchange (FX) tailwind while a 300 bps FX tailwind was expected. Its revenue guide would’ve been well ahead of consensus if the expected FX boost came to fruition. It also sees roughly 8.5% OpEx growth next quarter.

Quarter to date, Y/Y switched volume growth slowed from 14% to 11%, Y/Y switched transaction growth slowed from 15% to 12% and Y/Y cross-border growth slowed from 21% to 20%. The slowing is being driven by lapping its NatWest contract win, timing of social security payments and other comp headwinds. Mastercard did not cite the same fuel disinflation headwind that Visa did.

d. Balance Sheet

- $7 billion in cash & equivalents.

- $15.5 billion in debt ($1.3 billion is current or due within 12 months).

- Share count fell 2.5% Y/Y. It bought back $1.9 billion in stock with $4.5 billion left on its current plan.

- Dividend payments rose 13.6% Y/Y.

e. Call & Presentation Highlights

Macro:

Like Visa and others, Mastercard cited continued “resilience” in consumer spending. The strong labor market continues to support volume growth while credit and savings health is still in reasonable shape. Things are slowly getting more fragile… but they’re bending rather than breaking. Its forward guidance assumes this same level of “resilience” and stable macro headwinds play out next quarter.

Y/Y Growth:

- 5% North American volume growth vs. 6% Q/Q & 9% 2 quarters ago.

- 13% Rest of World volume growth vs. 16% Q/Q & 18% 2 quarters ago.

- 13.4% Y/Y revenue growth overall was 11% Y/Y growth FX neutral. Notably, FX helped revenue growth by 100 bps less than assumed. Mastercard would have beaten estimates had the impact been as expected.

- By bucket, value added service revenue rose 17% Y/Y and payment network volume rose 12% Y/Y.

- Its cyber security and marketing solutions were cited as standouts for the value-added service segment.

Y/Y Assessment (fees charged to other pieces of the value chain) growth:

- Domestic growth of 11% vs. 10% last quarter and 7% 2 quarters ago.

- Cross-border growth of 28% vs. 27% last quarter and 33% 2 quarters ago.

- Transaction processing growth of 14% vs. 16% last quarter and 12% 2 quarters ago.

Deal Momentum:

- Webster Bank is using Mastercard as its exclusive payment network. It will also use its marketing and security services.

- Won Citizens Bank’s debit business.

- Launched an “ultra-high net worth” credit suite for Citi’s Singapore and Hong Kong customer base. It signed a new Citibank deal to “forge a new card partnership in 60 countries” as well.

- Barclays and Mastercard launched a new Xbox credit card.

Newer Opportunities:

Open-loop transit momentum remains strong. Open vs. closed loop simply means payment collection lets consumers use their choice of card or digital wallet vs. forcing a specific option. It launched open-loop systems in Toronto, Philadelphia, Pakistan and the Netherlands this quarter.

Tokenized transactions (means that data is anonymized with a digital token similar to hashing) have doubled over the last 2 years. New deals here include a Mercedes program allowing customers to pay for gas from within their cars.

Maestro card is Mastercard’s old debit card system. It’s being replaced by “Debit Mastercard” to enhance fraud prevention, cross-border compliance and contactless payment capabilities. It’s sunsetting Maestro cards in Europe and will move 100 million cards to the new format in the coming years.

New Flows:

Commercial growth within new payment flows was “strong.” This is where Mastercard works with enterprises to embed intuitive financial service products into their own platforms. It’s working with Oracle to add its virtual card tech for handling supplier billing and business purchases. It’s also working with SAP to add its commercial payments software. This is really where open banking comes into play. Open banking refers to freer 3rd party data sharing to uplift risk management and underwriting capabilities. By sharing data between Mastercard and giants like SAP, firms can enjoy more meaningful insight gleaning to make product interfaces work better and to price services more appropriately.

In value-add services, Safety Net, its fraud prevention tool, surpassed $20 billion in savings over the past year. This is another area where open banking helps to enrich datasets and thus minimize loss, fraud and chargeback rates. It’s now actively using AI models within these products to “create real time predictive risk scores” on a per transaction basis.

Its personalization and test to learn capabilities are also being globally recognized. For the third straight year, Gartner ranked it as the leader in this category for its “superior dynamic yield personalization activities.” This basically means Mastercard is better at creating custom products for important clients than others in the space. It partners with Aldi and Dunkin here to constantly test new product iterations.

Switched or not Switched, that is the question:

A switched transaction means the transaction is routed through software that connects different parts of the payment ecosystem. This means customers who utilize Mastercard as a primary network can tap into various other gateways and card networks. The “switch” is what sends this processed payment to the appropriate piece of the value chain. Switched transactions enhance security and flexibility for consumers. Furthermore, a switched transaction is higher margin for Mastercard than processing a check for example. As of this quarter, 65% of its transactions were switched by Mastercard vs. 55% 5 years ago.

f. Take

This was a fine quarter and was eerily similar to Visa (if not a little bit weaker). Mastercard, like Visa, is an elite company. We have decades of revenue compounding at sky high margins to prove that point. This result did not deviate from that consistently positive theme. It’s performing about as well as anyone can expect while macro uncertainty runs rampant. What we heard from the team echoed what we’ve heard from other consumer giants. The consumer and economy are both strong as employment markets stay robust. Still, that same consumer and economy are on growingly precarious footing.

Savvy Trader today is the only place where readers can view my current, complete holdings. It allows me to seamlessly re-create my portfolio, alert subscribers of transactions with real-time SMS and email notifications, include context-rich comments explaining why each transaction took place AND track my performance vs. benchmarks. Simply put: It elevates my transparency in a way that’s wildly convenient for me and you. What’s not to like?

Interested in building your own portfolio? You can do so for freehere. Creators can charge a fee for subscriber access or offer it for free like I do. This is objectively a value-creating product, and I’m sure you’ll agree.

3. ServiceNow (NOW) – Earnings Review

a. Demand

ServiceNow beat its subscription revenue guidance by 1.4%. It also beat consensus estimates for total revenue by 0.7%. Its 25.8% 3-year revenue CAGR compares to 26.2% Q/Q and 26.1% 2 quarters ago. Finally, the company signed an impressive 83 new $1 million contracts vs. 70 Q/Q & 69 Y/Y.

b. Margins

ServiceNow beat EBIT estimates by 9.8% and beat $2.55 EPS estimates by $0.40.

c. Annual Guidance

ServiceNow slightly raised its full year subscription revenue growth guidance from 24.75% Y/Y to 25.5% Y/Y. The raise was via strong Q3 performance and not easier currency conversion rates. It also raised its EBIT margin guidance from 26.5% to 27.0%. It reiterated FCF and subscription gross margin guidance.

Guidance assumes no improvement to current macro headwinds.

d. Balance Sheet

- $7 billion in cash & equivalents.

- $1.5 billion in debt.

- The company expects 1.5% Y/Y share growth for 2023.