1. Progyny Leadership at a Bank of America Conference

“Overall the mood of the market for our selling season has normalized. Benefits managers and consultants are back to building programs at a more typical level.” — CEO David Schlanger

Progyny is enjoying more large enterprise selling opportunities this year vs. last year to coincide with this normalization. These large accounts sharply pulled back amid Covid-19 and are now expressing interest in Progyny’s benefits at a clip running above internal company expectations.

Two variables are contributing to this positive development:

- Primarily, economic re-opening

- Secondarily, the extremely tight labor market places added pressure on employers to stand out in attracting talent. Females making up a larger and larger % of the workforce merely amplifies this.

The proliferation of LGBTQ+ parenthood demand creates a compellingly sustainable long term growth tailwind for the company.

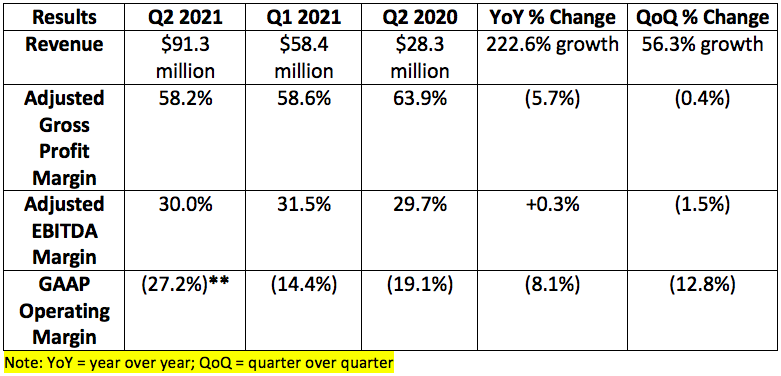

Progyny’s EBITDA margin on incremental revenue in this current quarter continued to greatly outpace the company’s business as a whole, pointing to continued expansion here.

Progyny’s net promoter score (NPS) for fertility and Rx is +81. NPS is a metric gauging the satisfaction of Progyny’s clients with the product.

Just to remind investors, Progyny is already the fertility benefits manager for behemoths such as Amazon, CVS Health, Microsoft, Google, Uber, PayPal, Unilever and so many more.

Cross-selling activity of Progyny’s fertility benefits and Rx benefits solutions has already reached the company’s full year target for 2021. Progyny believes eventually 100% of clients will be using both.

Schlanger reiterated that growth for 2022 will be similar to the company’s 2021 annual midpoint guide of 50.5%. Analysts were expecting growth to be closer to 45% for 2022 before this guidance was issued.

Progyny offered more color on the dip in utilization rate it saw at the beginning of July:

- The dip was across all specialties (not just fertility) pointing to a more macro cause.

- Progyny’s utilization rate bottomed in the beginning of July at around 88% of expected levels. It has since rebounded to 90%.

- Clinics believe this is via pent-up travel demand and NOT the delta variant as folks make up for 18 months of not being able to vacation. The dip was not geography specific hinting at this issue not being related to regional outbreaks.

- The forward guidance assumes Progyny’s utilization rate gets back to 92%-95% of normal levels.

“We do believe this [utilization rate dip] is a summer phenomenon that will correct itself relatively rapidly.” — Schlanger

2. Ayr Wellness earnings

“We will continue to think big in terms of footprint, products and branding and we will continue to deliver on those big plans.” — Founder and CEO Jonathan Sandelman

a. Results

**$52.3 million in one-time expenses and non-operating adjustments accounted for the $24.9 million GAAP operating loss. Without these non-recurring charges, GAAP operating margin would have been a lofty 28.9%.

Note that a large chunk of this Q2 2021 revenue was realized via inorganic growth and new store openings. The company will continue to be rationally aggressive with M&A going forward. Still, some of its markets generated same store sales growth of 50% in the quarter and organic wholesale growth also contributed.

“We’re able to buy great companies at EBITDA multiples of 5 or 6 growing over 100%. Premium beverage brands growing between 5% and 8% trade at EBITDA multiples of 25 to 30. We are investing.” — Sandelman

b. Guidance Updates

The lack of an EBITDA guidance raise in light of the revenue raise is due to “accelerating investments in branding, new markets and growth.” Margins are expected to trough and move higher in the coming quarters as new projects mature.

c. Operational Highlights

Ayr announced a deal to purchase 100% of Cultivauna LLC — the owner of Levia cannabis seltzers and water-soluble tinctures. The deal is for $10 million in cash and $10 million in shares up-front with an incremental $40 million available in shares based on internally set 2022 and 2023 revenue targets. I personally love seeing proceeds tied to the realization of operational goals. This keeps interests aligned.

“With Levia and CannaPunch, we have 2 of the top-selling beverage brands in the United States.” — Sandelman

Since Levia launched in Massachusetts 6 months ago it has become the top selling THC drink in the market eclipsing 80% total market share.

“The easiest move for CPG to enter the cannabis world will be in the beverage and the can business. Who knows it better than big beer? With their massive distribution and bottling it would be an obvious move.” — Sandelman

Ayr is supply constrained in the states where it operates. It quickly sells out everything it makes.

Ayr made 2 additional M&A moves during the quarter and the details can be found here.

Ayr’s entrance into Illinois pushes its population footprint to 85.7 million Americans thanks to the Herbal Remedies purchase and its affiliate (Land of Lincoln) winning a key license.

The company expects to quickly return to cash flow positive as all of its M&A and capital expenditures come online.

Ayr sold its brands in 280 stores during the quarter up 3x year over year.