Links to 40 detailed earnings reviews from this season

Link to my current portfolio & performance vs. the S&P 500

Table of Contents

- 1. Updated EBIT Comp Sheets

- 2. Fed Presser & Macro Data

- 3. Amazon (AMZN) – Shareholder Letter

- 4. Lululemon (LULU) – Earnings Review

- 5. Adobe (ADBE) – Earnings Review

- 6. Roku (ROKU), Amazon (AMZN), Trade Desk (TTD) & …

- 7. Uber (UBER) – Advertising & AI News

- 8. Coinbase (COIN) & PayPal (PYPL) – Stablecoin an …

- 9. Microsoft (MSFT), Alphabet (GOOGL) and OpenAI ( …

- 10. SoFi (SOFI) – Bank Regulation & Cash Coach

- 11. DraftKings (DKNG) – Updated Data Dump

- 12. Meta (META) – Glasses & WhatsApp

- 13. Frothy Markets?

- 14. Headlines

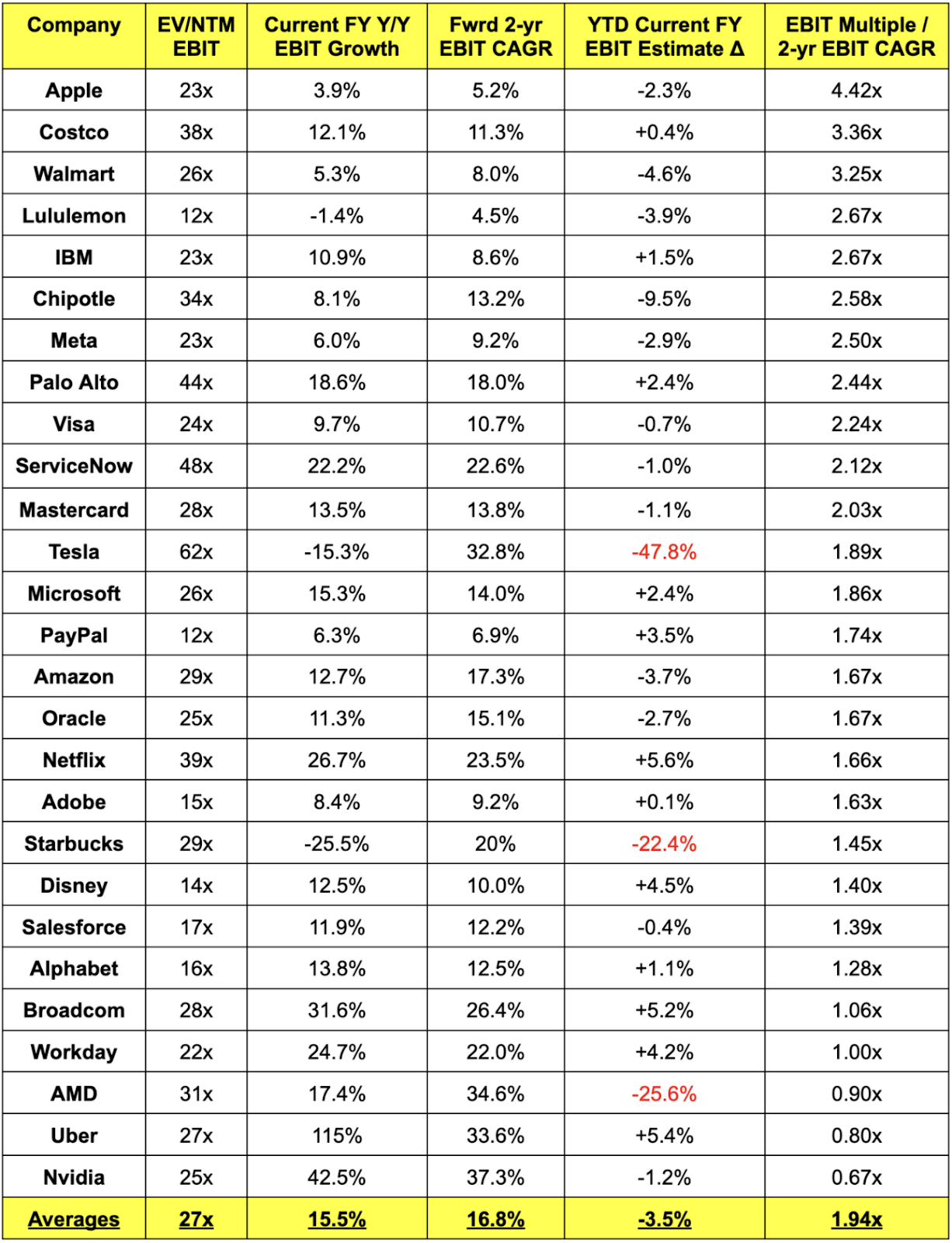

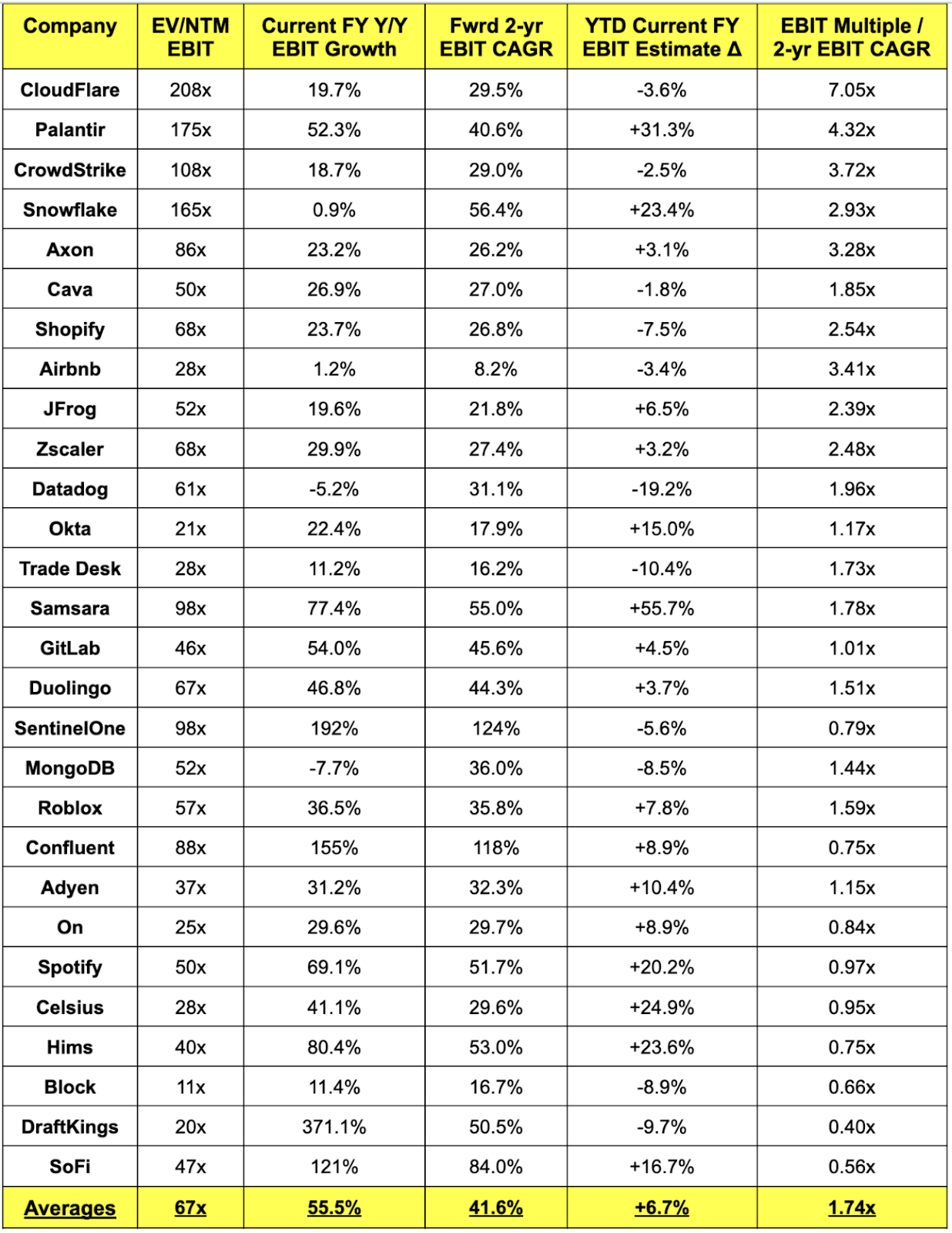

1. Updated EBIT Comp Sheets

It is difficult to offer a perfect, apples-to-apples valuation view across a diverse array of companies. Some don’t make any GAAP adjustments to EBIT. Some are inflecting to profitability, with growth rates facing abnormally easy comps. Some are lapping abnormally difficult comps. To more reliably compare, I made some adjustments for certain names. Those adjustments, along with a few pieces of added context, are found at the top of each chart.

a. Mature Growth Cohort

- The higher the number on the far right column, the more expensive the company is for this specific datapoint.

- The rightmost column is an iteration of Peter Lynch’s PEG ratio framework. Instead of dividing P/E by one year of earnings growth, I use EBIT and divide by a compounded 2-year earnings growth rate. I’ll refer to this number as a “score.”

- Several of these companies do not make non-GAAP EBIT adjustments, while others do. Because these companies are more mature, with lower non-GAAP adjustment intensity from things like stock comp, this didn’t make much of a difference to scores.

- For Tesla, the lack of non-GAAP EBIT adjustments is more material. Had I still used EBIT, the rightmost column score would have been 7.95x. For this reason, I used EBITDA data.

b. High Growth Cohort

- The average excludes Cloudflare to avoid the outlier. Had I not done this, the average on the rightmost column would have been 1.96x.

- AXON, Hims, Duolingo, Roblox, Trade Desk, Block, DraftKings and Cava use EBITDA data. None of these firms make non-GAAP EBIT adjustments and the differences in GAAP EBIT and EBITDA multiples are much larger than for the mature growth cohort. Using EBITDA credits them with a lower multiple, but hurts them via slower 2-year profit growth, as they don’t get the stock comp leverage many of these other firms are enjoying. It’s not perfect, but in my opinion, this is the best way to present a more comparable chart.

- I skipped this year’s profit growth and used 2026 and 2027 for DraftKings. This avoided having an extreme outlier in the chart, as its score would have been 0.1x had I not done this.

- Celsius, Spotify and Airbnb make no non-GAAP EBIT adjustments. The impact for all 3 is very small, so I didn’t tweak anything.

- Celsius is also comping over -42% Y/Y profit growth, so I used 2026 and 2027 in the 2-year EBIT CAGR column. Had I not done this, its score would have been 0.35x.

- SentinelOne is growing profit 232% Y/Y this year because of an extremely easy comp. For that reason, I used 2026 and 2027 profit growth for its score instead.

- SoFi uses non-GAAP net income, as it also doesn’t make non-GAAP EBIT adjustments and as the interest line item is a core part of operations for the company.

- For Snowflake, MongoDB and Datadog, I skipped the current FY profit growth in the two-year forward EBIT CAGR column. All three are heavily investing in innovation (MongoDB also lapping non-recurring, margin-rich revenue) and all three are expected to revert back to more normal profit growth in calendar 2026. I think skipping 2025 growth gives a better picture of valuation in normal times for these firms. Had I not done this, Snowflake’s score would have been 5.95x, MongoDB’s would have been 4.86x and Datadog’s score would have been 5.50x.

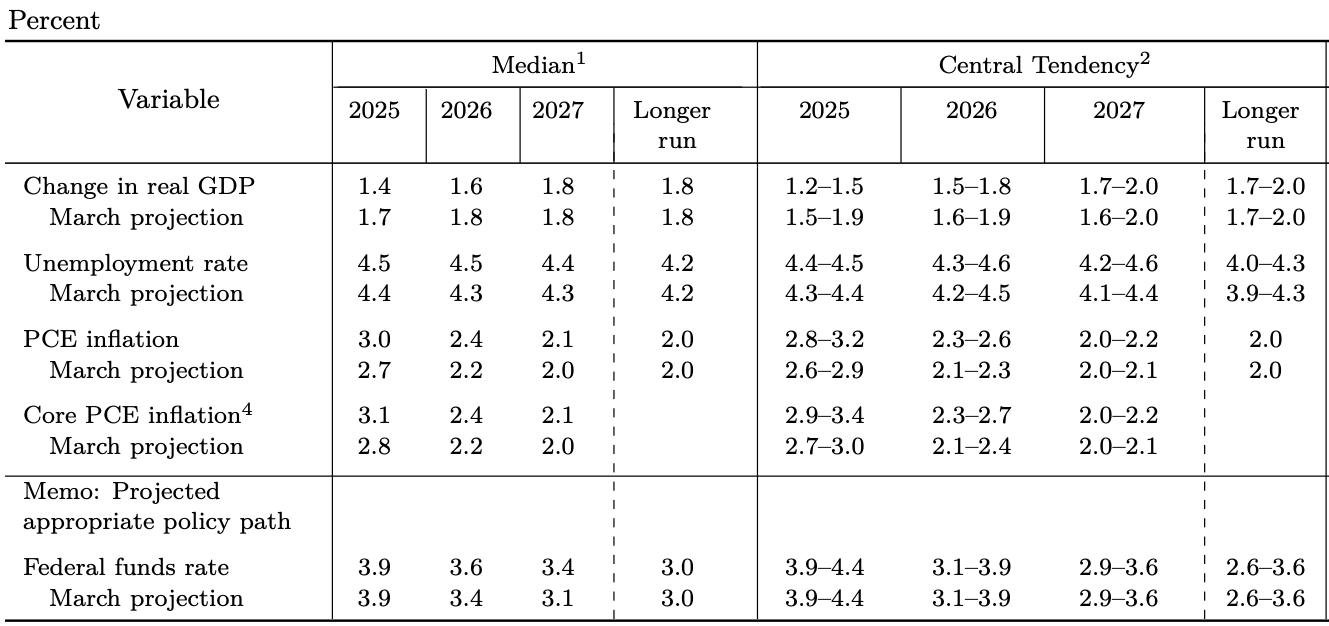

2. Fed Presser & Macro Data

Changes in Economic Projections vs. March 2025 Meeting:

- Took GDP estimates down 0.3 points for 2025, 0.2 points for 2026 and maintained projections for 2027.

- Brought unemployment projections up 0.1 points for 2025 and 2027 and up 0.2 points for 2026.

- Brought PCE projections up 0.3 points for 2025, up 0.2 points for 2026 and up 0.1 points for 2027.

- The Fed still sees roughly 2 rate cuts this year, but now just 1 cut in 2026. It also still expects 1 rate cut in 2027.

Changes to the Fed Statement vs. Last Meeting:

- It said unemployment “remains low” instead of “has stabilized at a low level in recent months.”

- Changed economic uncertainty “increased further” to “diminished but remains elevated.”

- Removed “judges that the risks of higher unemployment and inflation have risen.

Powell Presser – Inflation & Policy:

The themes of this event were “uncertainty” and ‘cut tariffs and we’ll probably cut rates.’ Powell acknowledged “tons of progress” towards its 2% inflation target, with three consecutive months of favorable readings after a more challenging January and February. At the same time, that progress has stalled a bit due to wildly fluctuating tariff expectations. Potential tariffs have led to survey-level and market-level inflation expectations moving higher. At the same time, key market indicators for longer-term inflation expectations remain in very good shape… and survey-level fears have dissipated since tariff concerns peaked in April.

- The yield for this week’s 5-year treasury inflation protected securities (TIPS) auction was 1.65% vs. 1.702% last auction.

“Uncertainty” was Powell’s favorite word of this event. The Fed simply doesn’t know if tariffs will even cause a one-time spike in prices. If that does happen, they also don’t know how sticky that spike will be. That has a lot to do with the final level of implemented tariffs and how enterprises and governments manage them. That’s hard to model. What isn’t hard is reading between the lines of what Powell is saying. The Fed would likely be cutting rates right now without a tariff overhang. And for this same exact reason, the conviction Fed members have in their rate projections is abnormally low. They feel well-positioned to wait a bit longer and see what the actual impact ends up being. They do not feel the need to cut ahead of that clarity. With economic growth and unemployment looking resilient, I think that is valid in the near term. At the same time, I do not think draining more liquidity via continued quantitative tightening (QT) is necessary and feel that maintaining the current size of the balance sheet would be appropriate. Bond markets are not flushed with liquidity and inflation has come down more than enough to make that decision. So yes, I get rate cut patience, but no I do not agree with more QT.

This week:

- The Export Price Index M/M for May was -0.9% vs. -0.1% expected and 0.1% last month.

- The Import Price Index M/M for May was 0% vs. -0.2% expected and 0.1% last month.

Powell Presser & Some Data from This Week – Unemployment & Consumer Health

The employment market is “in balance” when it comes to supply and demand. Wage inflation is gradually moderating, yet still at a healthy rate modestly above overall inflation. That’s what we want. Inflation cooling beyond the levels of wage disinflation to drive real income growth and purchasing power (without an overheating economy).

- Core retail sales for May came in at -0.3% M/M growth vs. 0.2% expected and 0% last month.

- Retail sales for May came in at -0.9% M/M growth vs. -0.5% expected and -0.1% last month.

- Initial Jobless Claims were 245,000 vs. 246,000 expected and 250,000 last report.

- Continuing Jobless Claims were 1.945M vs. 1.940M expected and 1.951M last report.

Powell Presser & Some Data from This Week – Economic Output:

Powell thankfully talked about the Q1 GDP reading being a direct byproduct of import front-loading. He rightfully cited private domestic final purchases (excludes net exports, inventory and government spending) and how that growth remained at a resilient 2.5% Y/Y clip. The negative GDP reading was a weird one-off event related to tariffs. Not a sign of our economy structurally decaying.

- Industrial Production M/M for May came in at -0.2% vs. 0% expected and 0.1% last month.

- The Philly Fed Manufacturing Index for June was -4 vs. -1.7 expected and -4 last month.

3. Amazon (AMZN) – Shareholder Letter

Jassy sent out a new shareholder letter on AI’s transformation of Amazon’s business. He reviewed how GenAI and agentic AI are already improving Alexa and shopping discovery (AI shopping assistant up to tens of millions of users). He spoke about new tools like Lens (take a picture to search), its Buy for Me shopping agent and size recommendation tools are enhancing its marketplace. He discussed AI advertiser tools with 50,000 merchant users, its chips and model tool work via Bedrock and SageMaker, as well as how dramatically AI is already enhancing fulfillment efficiency.

And while AI is touching basically everything Amazon does, they’re just getting started. Jassy views AI agents as the real frontier of software-level value creation. They’re going to keep rapidly innovating in this area, with constant updates to existing agents and so many more new ones coming. Notably, this should eventually shrink its corporate headcount needs over time, which will provide another layer of margin expansion for this behemoth.

AI is fiercely competitive. But? With Amazon’s world-class cloud infrastructure and data scale, its high-quality chips and plenty of internal talent, this company should clearly be one of the winners.