1. Lululemon Athletica (LULU) -- Q4 2022 Earnings Review

a) Demand

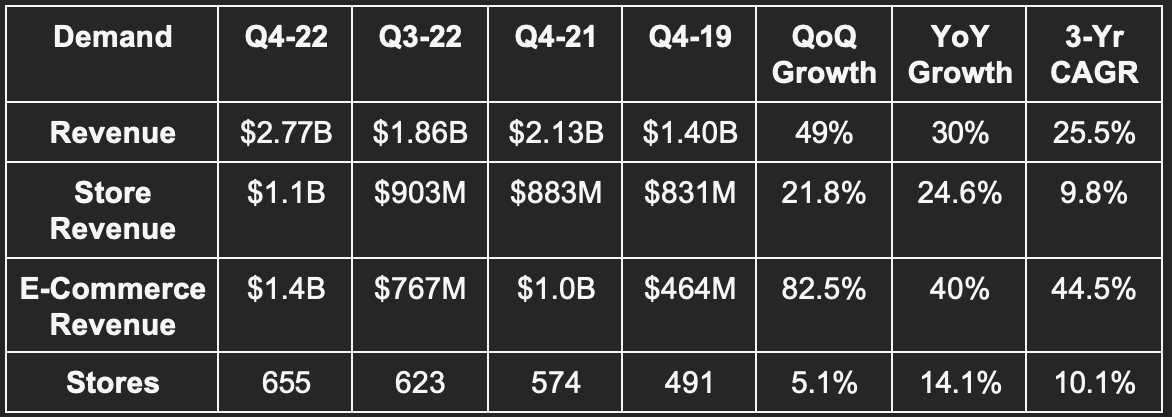

In January, Lululemon updated its revenue guidance from $2.63 billion to $2.68 billion. It beat this raised guidance by 3.4% and beat the subsequently raised analyst estimate by 2.6%.

Lululemon saw inventory rise by 57% YoY when excluding a Mirror inventory impairment and 50% YoY with that impact. This compares to guidance of 60% YoY inventory growth. Lower growth is preferred here.

More Quarterly Demand Context:

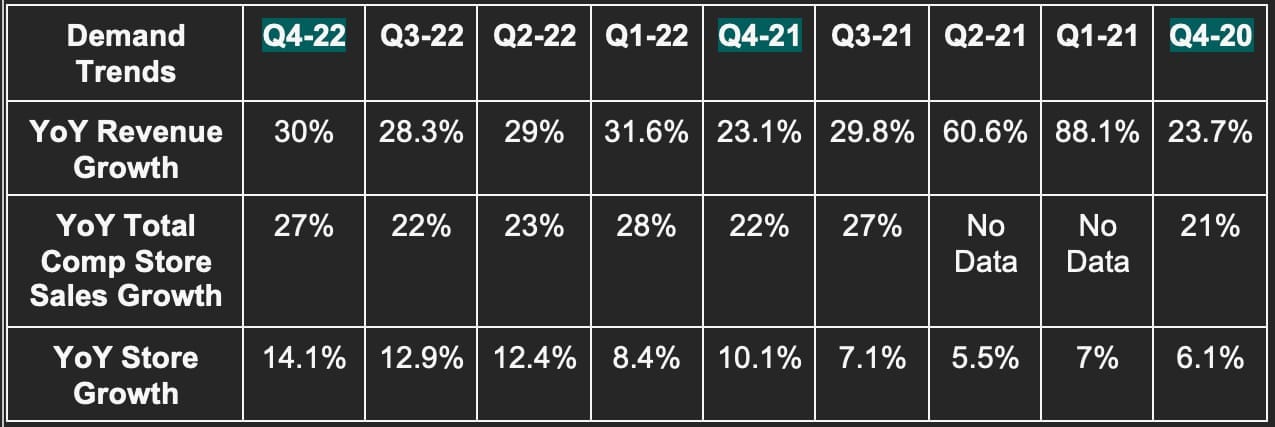

- 30% YoY growth was 33% currency (FX) neutral.

- Revenue rose 29% YoY in North America and 35% internationally.

- 27% YoY total comp store sales growth was 30% FX neutral.

- Direct to consumer (DTC) represented 52% of sales vs. 49% YoY.

More 2022 Demand Context:

- Revenue rose 30% YoY for 2022 with total comp store sales rising 25% YoY.

- It opened 81 stores during 2022.

- Three Year Compounded Annual Growth Rates (CAGRs):

- 23% for women; 26% for men; 44% for accessories; 46% for e-commerce.

- New and existing guest transactions rose in the mid 20% range.

- Store productivity is above 2019 levels. Store traffic rose 30% YoY and has compounded at a 3-year rate of 7%.

- Digital traffic rose 45% YoY and has compounded at a 3-year rate of 40%.

b) Profitability

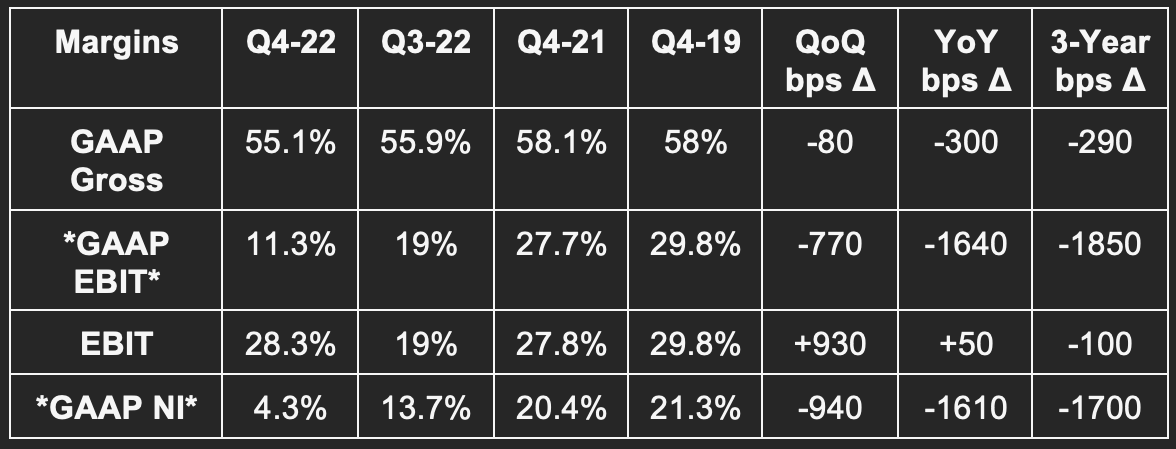

- Lululemon guided to its adjusted gross margin falling by 100 bps as part of its January update. It beat this expectation by 30 bps.

- Missed GAAP EBIT estimates by 58.4%. This includes a $408 million Mirror goodwill charge. Non-GAAP EBIT, which excludes this impact, beat estimates by 3.5%.

- Missed $4.25 GAAP EPS estimates & its identical guide by $3.31 due to the same Mirror goodwill charge. Non-GAAP EPS, which excludes this charge, beat $4.25 estimates by $0.15.

- Beat free cash flow (FCF) estimates by 29.5%.

More Margin Context:

- GAAP margins were hard hit by a $442.7 million Mirror goodwill impairment charge. This stemmed from disappointing hardware sales for the segment and a shift in go-to-market strategy explained below.

- Adjusted gross margin ex-Mirror impairment was 57.4%. This was hurt by 50 bps of FX headwinds.

- SG&A actually enjoyed 50 bps of FX YoY benefits for the quarter.

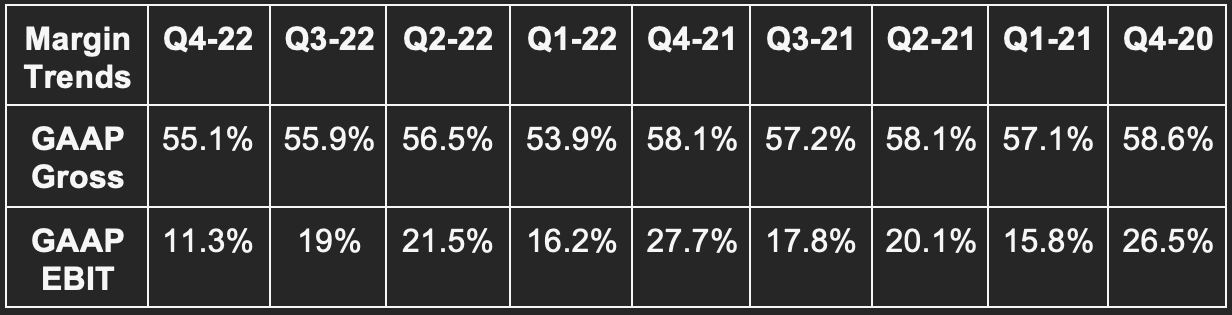

- GAAP Gross margin for 2022 fell from 57.7% to 55.4%.

- GAAP EBIT was flat YoY due to the mirror impairment charge. Ex-impairment charge, EBIT rose 30% YoY. Similarly, GAAP EPS fell from $7.49 in 2021 to $6.68 in 2022. This is all related to Mirror. Ex-impairment charge EPS rose 29.2% from $7.79 to $10.07 YoY.

c) Balance Sheet

- Lulu generated $838 million in FCF during the quarter. This allowed it to greatly bolster its cash position which now sits at $1.2 billion.

- Bought back $69 million in stock this quarter vs. $17 million QoQ & $321 million YoY.

- It has about 75% of its $1 billion buyback left.

- It has $393.5 million available in credit capacity.

- Inventory rose 50% YoY but fell 16.9% QoQ. Q3 2022 was supposed to be the “high water mark” for its inventory position which looks to be the case. Leadership guided to inventory continuing to normalize with YoY growth rates here matching revenue for the 2nd half of the year. It’s encouraging to see Lululemon execute this normalization with quite modest rises in discount rates.

d) Forward Guidance

Q1 2023:

- Beat revenue estimates by 3.4%.

- Beat $1.65 GAAP EPS estimates by $0.31.

- “Significant GPM expansion” via lower air freight charges and promotional normalization. Gross margin estimates sharply rose from 53.9% to 56.8% following the call.

“We continue to see strength and momentum across the business so far in Q1.” -- CEO Calvin MacDonald

2023:

- Beat revenue estimates by 2.4%. Its revenue guide implies 15.5% growth which is slightly above its longer-term target despite comping vs. 30% growth in 2022.

- Beat $11.30 GAAP EPS estimates by $0.31.

- EBIT margin to rise by roughly 30 bps vs. 10 bps of expansion expected.

- Will open 45-50 new stores with 30-35 openings happening abroad and most of those being earmarked for China.

- Gross margin to expand by 150 bps YoY due to freight benefits and stabilizing markdowns. This implies a 56.9% margin vs. analyst estimates calling for 56.2%. These estimates rose to 57.3% following the report.

- CapEx to rise sharply to $670 million YoY in 2023 due to distribution center investments, store openings and remodels. It is building a new facility in LA and expanding capacity in Columbus and Toronto. This will be a temporary margin headwind.

It remains fully on track to execute on its Power of Three x2 plan which calls for 15% compounded revenue growth and modest operating leverage through 2027.

“While we are mindful of the ongoing macro uncertainties and we continue to plan the business prudently, we're excited with our sales trends in Q1 and also the benefits we expect to realize in 2023 from lower air freight and our new Lululemon Studio model… We can invest into our growth pillars while delivering operating margin in 2023 slightly ahead of our goal.” -- CFO Meghan Frank

e) Call & Release Highlights

Market Share Gains:

Lululemon took 230 bps of incremental YoY market share within its adult active apparel category. This rapidly rose from 130 bps of share gains last quarter. It was its largest quarterly gain in 3 years which is according to 3rd party research from NPD Group -- not per internal data.

Growing Brand Awareness & International Traction:

Since April 2022, Lululemon raised its brand awareness in the following geographies as follows:

- From 19% to 24% in Australia.

- From 7% to 9% in China. China revenue rose 30% YoY as the country opened up and so business vastly accelerated into 2023. A tough December due to lockdowns held back results here for the quarter.

- From 14% to 16% in the U.K.

Change in Subscription & Mirror Strategy:

Lulu is shifting away from go-to-market Mirror hardware growth investments. It is launching a brand-new digital fitness app this summer, with a lower subscription price, which will become the focal point of this refreshed approach. It’s pivoting away from Mirror investments as falling customer acquisition cost (CAC) has not been meaningful enough to justify continued spend. By removing hardware needs associated with accessing the digital content, it hopes to remove friction associated with becoming a member and to, in turn, accelerate growth.

Its Essentials members tier (which is a free loyalty program) is already seeing “robust new member growth.” This growth is “significantly exceeding expectations with 9 million members in just 9 months.” Lulu does NOT offer discounts through this program… just other perks like early product access. These members engage with the brand more frequently, spend 9% more (all incremental) and retain more reliably.

“Since our acquisition, the at-home fitness space has been challenging. While members love our content, hardware sales did not match expectations. As we continue to invest prudently in this business, we are evolving the model from being focused on hardware-only to offering content through a digital and app-based solution as well. We think the lower cost of entry will allow us to more easily migrate and attract guests into it.” -- CEO Calvin MacDonald

On Mark Downs:

- The firm “managed business very well through a highly promotional environment.” Discount rates were just 40 bps higher than 2019 and stable YoY.

- Importantly, as it moved through the holiday season, regular price sales “returned to normal levels.”

“We don’t drive top line growth through discounts or promotions and have no intentions to do so. We run a full-price business with markdowns strategically used to clear seasonal and other select products. This will remain our approach.” -- CEO Calvin MacDonald

Footwear:

There was not much color offered on the progress of this product expansion. Leadership told us that they’re “pleased with the performance and guest response.” It will debut its first road to trail running shoe this year while debuting its first men’s shoe in 2024. It’s hard to imagine it would be moving ahead with these plans if this endeavor was not going well.

f) My Take

Besides a one-off Mirror impairment charge due to some ill-advised M&A, this was a flawless quarter for Lululemon. Share gains were robust, margins are set to materially expand and both new and core products and geographies continue to provide ample opportunities. I also love the decision to bite the bullet on Mirror hardware and focus on stickier subscription packages. It’s the right move and shows a willingness and openness from leadership to right previous wrongs.

This is the hottest brand in its category with no slowdown in sight despite being a relatively luxury-goods seller amid hectic macro. This climbed into a top 5 position for me this past week and I’m entirely fine with that.

2. SoFi Technologies (SOFI) -- M&A Rumors

For several months, SoFi leadership has hinted at wanting to fully own its purchase mortgage business and to vertically integrate the back-end processes that it entails. Partners were struggling with timely funding (often taking up to 90 days) which was forcing SoFi to hold off on aggressively investing into the segment.

Well? There are new rumors swirling that SoFi will buy Wyndham Capital to fill the void of this backend cohesion. Three Twitter accounts were all over this news and I wanted to give them credit for their excellent research. To DataDInvesting, Vadim Kotlarov and Trust_In_Noto, wonderful work. Thank you to all three of you.