Table of Contents

- 1. Duolingo (DUOL) — Earnings Review

- 2. Datadog (DDOG) – Earnings Review

- 3. The Trade Desk (TTD) — Earnings Review

1. Duolingo (DUOL) — Earnings Review

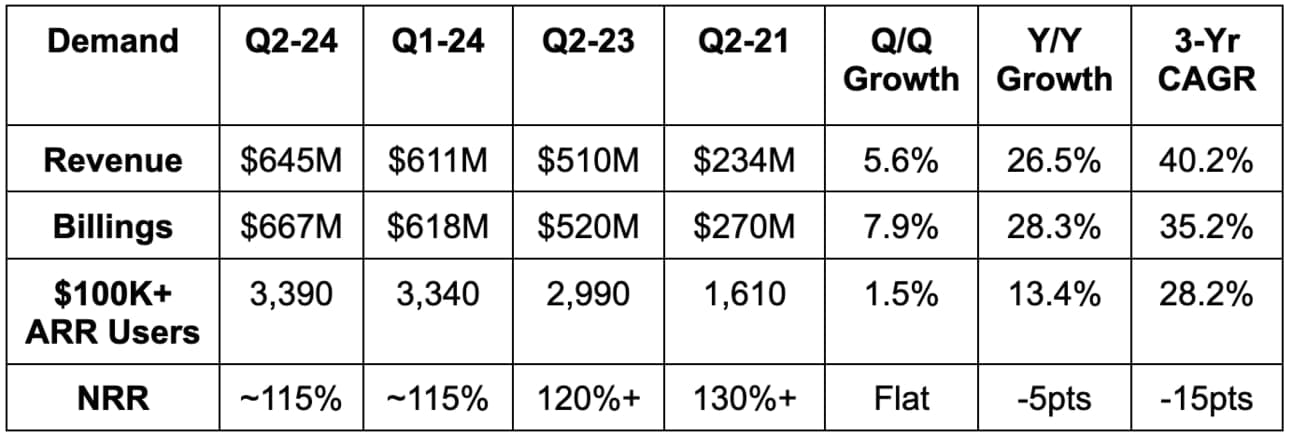

a. Demand

- Beat bookings guide by 5%.

- Foreign exchange neutral (FXN) bookings growth:

- 50% subscription bookings FXN growth vs. 47% actual growth.

- 41% total bookings FXN growth vs. 38% actual. It thinks its core subscription business will continue to outgrow other segments.

- Beat revenue estimate by 0.7% & beat guidance by 0.8%.

- User metrics were also all ahead of the widely ranging estimates that I saw. Monthly active users (MAUs) crossed 100M, with accelerating Y/Y growth. Daily active user (DAU) growth also accelerated.

- Other revenue rose 9% Y/Y due to a weak advertising and in-app purchase environment and lack of focus here (really just cares about subscriptions).

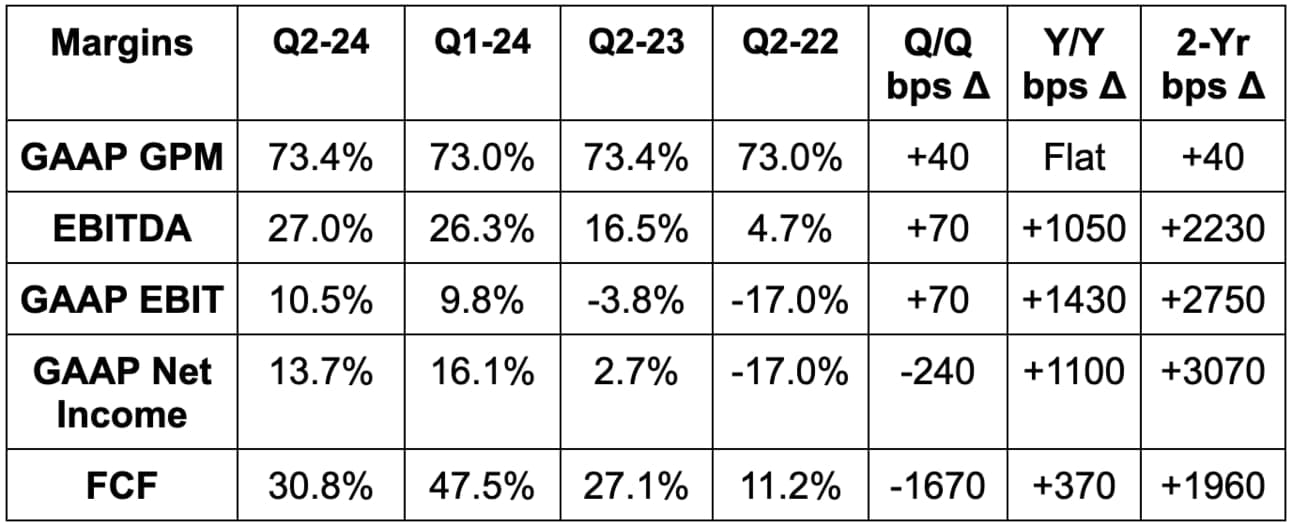

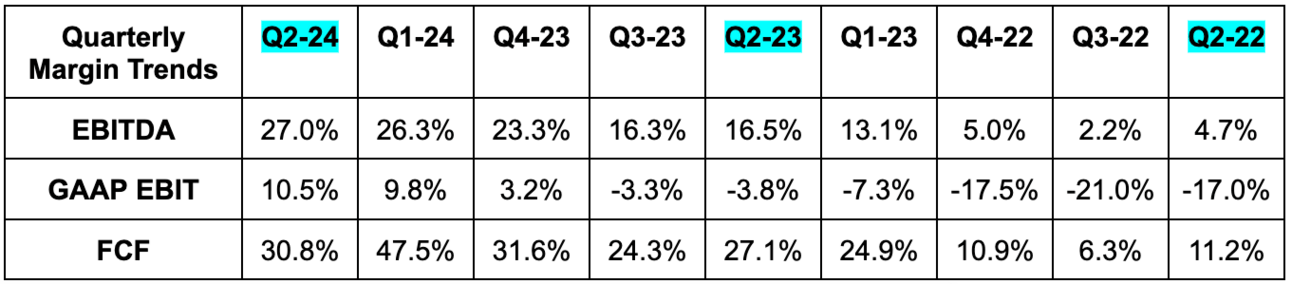

b. Profits & Margins

- Beat EBITDA estimates by 24% & beat guidance by 26%.

- Doubled $9M GAAP EBIT estimates.

- Beat $0.32 GAAP EPS estimates by $0.19.

- Beat $0.85 EPS estimates by $0.16.

- Met GAAP GPM estimates.

For Y/Y non-GAAP operating cost leverage, general & administrative (G&A), S&M 2 points and R&D 6 points. Fixed cost leverage, thanks to outperforming revenue, was the main driver here. Non-GAAP OpEx metrics remove the leverage benefit from lower stock comp as it moves further away from the IPO. I think that offers a better picture of structural margin expansion.

c. Balance Sheet

- $888M in cash & equivalents.

- No debt.

- Stock comp rose 13% Y/Y. Guided to 1% to 1.5% dilution for the year.

d. Annual Guidance & Valuation

- Raised annual bookings guide by 1.4%.

- Raised annual revenue guide by 0.5%, which slightly beat estimates.

- Raised annual EBITDA guide by 4.8%, which beat by 3.3%.

It sees growth in the second half of the year slowing as expected. It enjoyed a few unique tailwinds last year (Barbie and favorable FX) that will not recur during the second half. Still, its guide implies 28% Y/Y bookings growth, and leadership is always conservative. Q/Q EBITDA margin is expected to fall due to more hiring.

e. Call & Letter

More Success:

Elite execution came from the same recipe that has powered this annoying owl’s success since well before the IPO. It has the largest dataset in language learning by a country mile. Its team is as obsessive with split testing as I am with researching companies. It exhaustingly toys with variables to gain basis points of engagement, teaching efficacy and retention progress. These basis points add up.

This is why 90% of its revenue growth comes from organic channels rather than paid marketing. This is why it continues to see DAUs as a % of MAUs aggressively jump from 29% to 33% Y/Y and this is why results look so impressive. Chegg and Babbel fixate on paying for growth; Duolingo fixates on building a better product and letting growth naturally follow. It spends very little on marketing on a relative basis vs. these two, yet continues to compound while they falter.

The top-of-funnel remains wonderfully strong and Duolingo continues to enjoy a strong cadence of returning lapsed users. As an important aside, this is why alt-data for downloads (that shows recent slowing) is irrelevant; it’s a byproduct of Duolingo having well over 500M downloads and a larger portion of its DAU growth coming from people who have already downloaded the app.

Social media impressions rose 190% Y/Y and 20% of its DAUs now have year-long streaks. They’re hooked. All of this contributes to its expectation of maintaining 50%+ DAU growth for the foreseeable future. At this scale and in this environment… that growth is absurd.

Duolingo Max & GenAI:

Duolingo Max is live for 15% of its DAUs, and uptake so far has been very strong. This helped drive the beat and raise, but the vast majority of the financial impact here will not be felt until 2025. GenAI continues to be the secret sauce for this subscription tier’s early traction. In the coming months, it will introduce a new GenAI-powered tool to have real-time conversations with its characters. This has been among the most requested features for Duolingo, and GenAI makes the cost of building it possible.

That leads us to another interesting point. Many assumed GenAI would kill this bird… I said not so fast… results point to GenAI augmenting operations, if anything. Like the new conversational tool and its radio podcasting project, the tech is shrinking years of content creation time down to a few months. DUOL’s preferred OpenAi partnership is helping too. Expedited timelines allow Duolingo to actually pursue these opportunities. It allows it to upgrade how fun, valuable and engaging its content is.

Some argue that real-time translators will kill it, but as leadership reminded us, that technology is a decade old. Furthermore, Duolingo caters to learners wanting to immerse themselves in a new language. Its users are trying to gain an edge in an interview room for a job or to impress a cute girl. Talking to someone through a phone is not a replacement for that.

“We’re not particularly worried about GenAI replacing us.”

Co-Founder/CEO Luis von Ahn

Family Plan & Getting More Social:

Since Duolingo added a dedicated Family Plan team last quarter, traction here has accelerated. 20% of its subscribers are now on this plan and retention benefits are notable.

It also keeps adding more social tools. It created the “Friend Streak.” This allows friends to share their learning journeys and even nudge each other with reminders to do their lessons. Duolingo does this nudging on its own, but now it has found a creative way to motivate passionate learners to do that for them. Making Duolingo more social has consistently delivered engagement gains and this time should be no different. Early results for this launch are “excellent.”

Going Global:

Duolingo has operationalized a global growth playbook in under-penetrated markets. It’s very similar to what Airbnb has done to accelerate volume in its less mature geographies. Duolingo starts with a bit of performance advertising, adds marketing directors, builds up its social presence and then lets things blossom from there. In Japan, this led to 93% Y/Y DAU growth and 58% Y/Y bookings growth. It sees many more markets like this one, and added marketing managers in France and Korea as a result. What a luxury it is to sell a digital product that is deeply relevant across the entire globe.

Advanced English:

Duolingo’s multi-year push to deliver more advanced English content continues. It now has this content in all 20 of its English courses and added a standalone English course for its top learners. It’s getting better at starting students (with widely ranging experience levels) at the right level of difficulty, but thinks there’s more work to be done there.

Macro:

“There's a lot of uncertainty in the external world. When we look at our numbers, we're not seeing anything. Our consumers don't seem to be reacting to anything. There's nothing worrying. In the past, we've had similar situations where there's uncertainty in the world. And when we look at our consumers, we just can't see anything. We don't really know why that is. I'm not going to say that we are recession-proof. We just don't know because we've never really gone through a recession. Because we have such a good free tier, people who can’t pay us are just using that.”

Co-Founder/CEO Luis von Ahn

Math and Music:

Growth for both of these newer products was called strong. Duolingo does not monetize new products until a few years of content creation, product-market fit and scaling.

f. Take

Duolingo is one of one in its combination of growth, GAAP margins, strong cash flow, rapid leverage and a large opportunity. When you add a sub-40x non-GAAP earnings multiple to that, I think there’s quite a bit to like. I continue to think this is the most underrated team in public markets and continue to be amazed by how well it performs every single quarter. Its core business is thriving, new products provide more growth prospects in the years ahead and this company keeps killing it. Go owl go.

2. Datadog (DDOG) – Earnings Review

Datadog 101:

Datadog is a dominant player in the data observability space. Observability simply refers to the practice of monitoring an entire software ecosystem to track issues, vulnerabilities and performance. Other players within this area include the hyper-scalers, Splunk, Elastic, CrowdStrike (through its Humio acquisition) and many more. Datadog splits its observability niche into 3 smaller buckets: infrastructure monitoring, log management and Application Performance Monitoring (APM).

Infrastructure monitoring: provides a holistic view of assets like servers and networks. It automates the collection of traffic and overall usage insights. That means it can more expediently fix and uncover infrastructure issues.

Log (or record of event) management: manages “timestamped records of events” occurring across the entire infrastructure. This also facilitates faster issue remediation and optimization of performance. These logs are organized and utilized within infrastructure monitoring and other use cases to identify things like customer service issues. Log management encompasses the collecting, maintaining, and leveraging of log data. This product routinely supports infrastructure monitoring, BUT there’s a key difference between the two. Log management handles event-based data, while infrastructure monitoring (as the name indicates) handles infrastructure-based metrics.

Application Performance Monitoring (APM): tracks app performance and uncovers/prioritizes performance issues to be remediated.

These three product categories closely tie together to form its “unified platform.”

Because Datadog already handles network viability, security is a wonderfully relevant growth adjacency. Products like Cloud Infrastructure Entitlement Management (CIEM) for example, ensure identity controls are strict and minimum access permissibility is in place. There’s a lot of competition here, but Datadog is no slouch. CIEM diminishes risk of identity attacks in a cloud environment. Its Security Information and Event Management (SIEM) product allows for “long term data log visualization for security investigations.”

“At Datadog, we're focused on helping our customers observe, secure, and take action on their complex systems."

Co-founder/CEO Oliver Pomel

a. Datadog Demand

- Beat revenue estimates by 3.4%.

- Beat billings estimates by 4.6%.

- Total customer count rose 10% Y/Y.

- $100,000+ annual recurring revenue (ARR) customers now represent 87% of total revenue and that continues to climb.

- 11% of its clients are now using 8+ products vs. 7% Y/Y.