Other reviews from this season to read:

- Mercado Libre & Datadog

- AMD & Uber

- Axon

- SoFi

- Amazon

- On Holding

- AppLovin & Cloudflare

- Duolingo

- Meta

- Lemonade

- Robinhood

- Hims & The Trade Desk

- Alphabet

- Shopify & Coupang

- ServiceNow

- Apple

- Spotify

- Palantir

- Microsoft

- Taiwan Semi

- Netflix

- Tesla

Table of Contents

a. Key Points

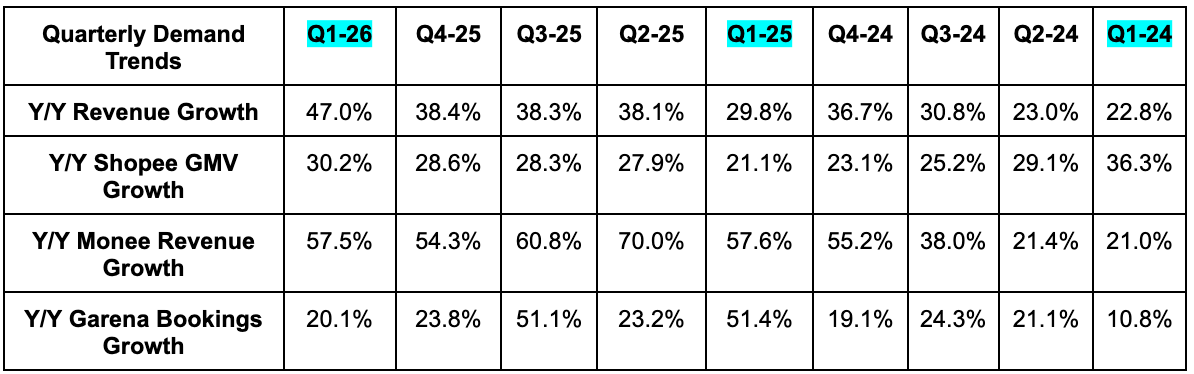

- Strong demand trends across the board.

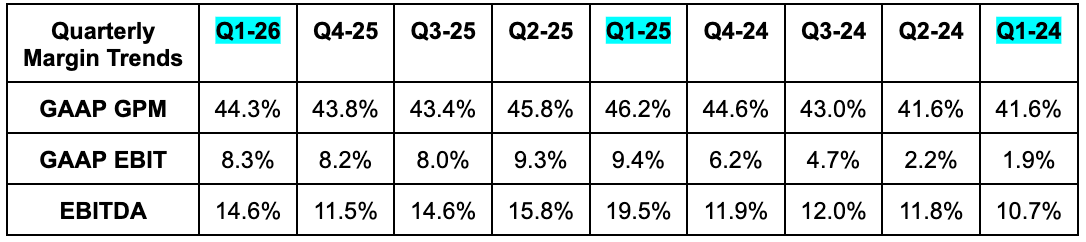

- Margin pressure from ongoing investments that look to be working.

- Stable credit health.

- Reiterated annual Shopee (e-commerce platform) growth expectations.

b. Demand

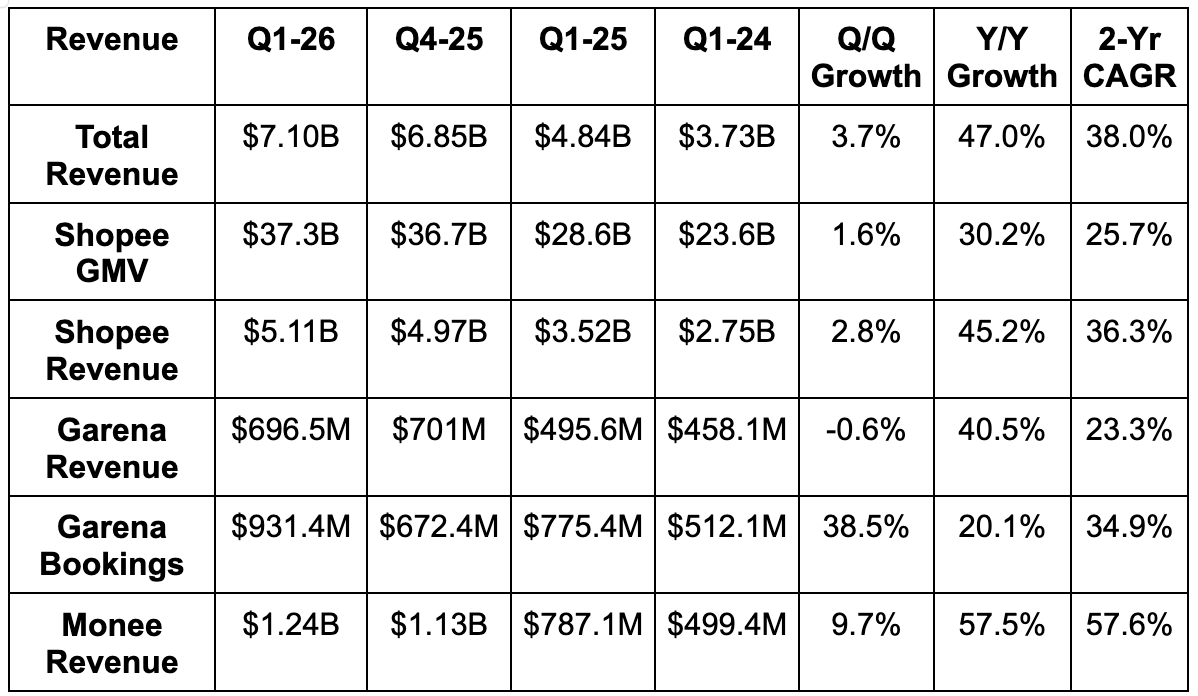

- Beat revenue estimate by 7%.

- Shopee (e-commerce) revenue beat by 8.6%.

- Monee (financial services) revenue beat by 7.6%.

- Garena (entertainment) revenue beat by 8.1%.

- Beat e-comm gross merchandise value (GMV) estimate by 2.5%.

c. Profits & Margins

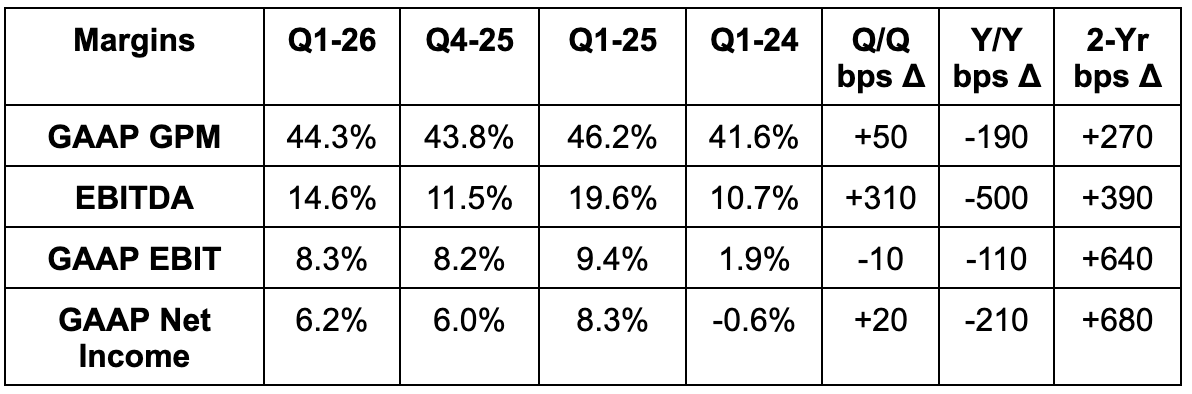

- Beat EBITDA estimate by 15%.

- Beat Shopee EBITDA estimate by 2.4%. Shopee EBITDA margin was 4.2% vs. 7.5% Y/Y due to aggressive investments to fortify its value proposition in 2026.

- Beat Garena EBITDA estimate by 33%.

- Missed Monee EBITDA estimate by 6.6%.

- Beat GAAP EBIT estimate by 16%.

- Missed GAAP $0.70 EPS estimate by $0.03.

- Lower Y/Y non-operating income & a higher tax rate both hurt EPS.

d. Balance Sheet

- $4.04B cash & equivalents.

- $264M borrowings. $1B convertible notes.

- 0.2% Y/Y dilution.

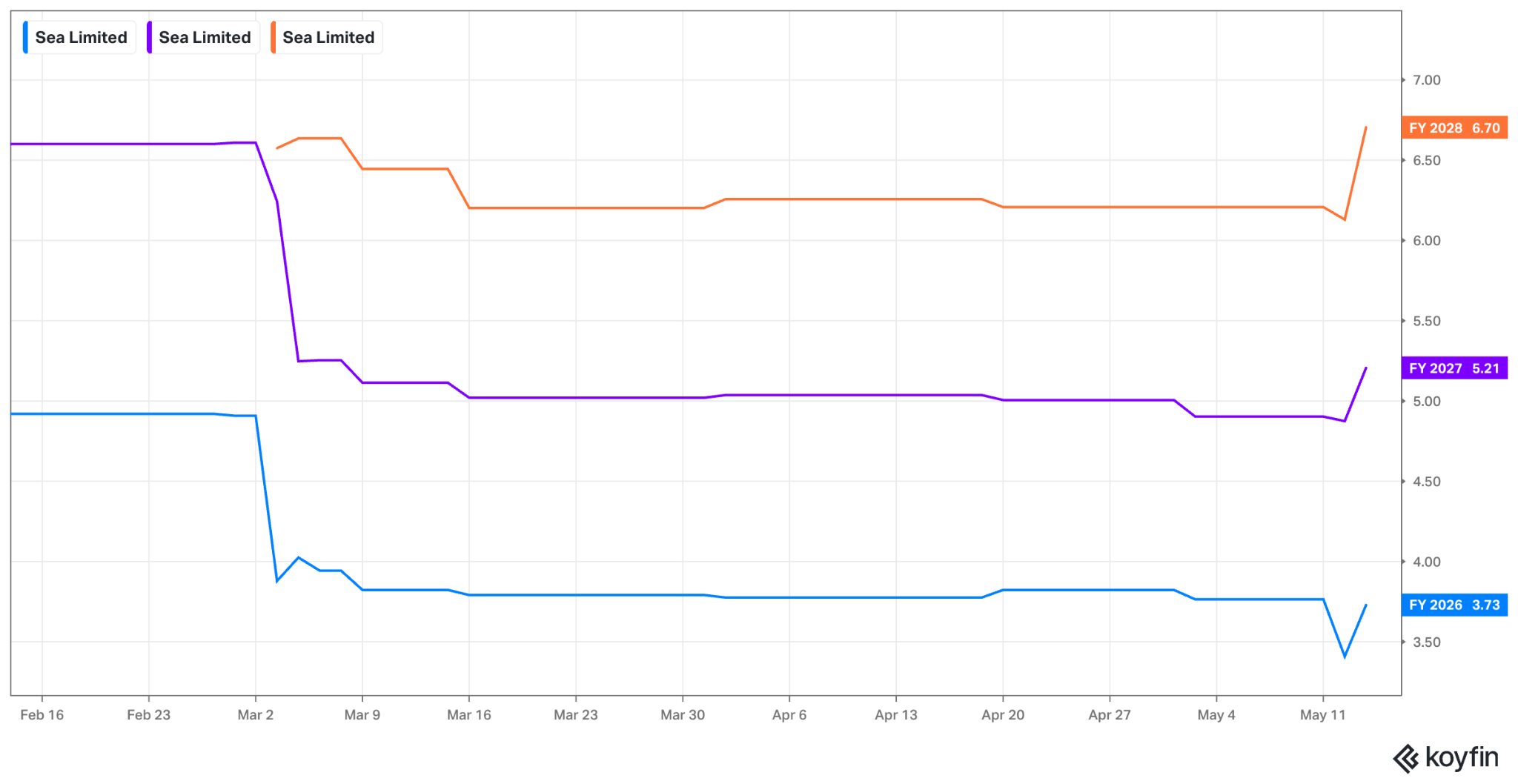

e. Guidance & Valuation

SE reiterated expectations for 25% Y/Y Shopee GMV growth and flat or better Shopee EBITDA compared to last year. Like virtually all of the e-commerce companies we cover, SE remains firmly in investment mode for 2026. They’re beginning to see expected efficiency gains percolate from all of these projects, and expect those encouraging signals to meaningfully build with time. It’s full speed ahead on building their brand, expanding globally, enhancing their fulfillment footprint and advancing their credit business. And this is why margins are currently contracting. Just like for MELI, these decisions are the right ones, in my opinion. Their runways and positioning are too strong not to be grabbing land as quickly as they can right here and right now. There’s a large list of fragmented and inferior competitors for this company to displace in Asia and Latin America, and MELI and AMZN are pushing hard to take that for themselves. They firmly expect to reach their long-term goal of EBITDA at 2%-3% of total GMV.

SE trades for 26x forward EPS. EPS is expected to grow by 18% this year, 40% next year and 28% the year after.

f. Call & Release

Shopee:

Shopee is performing well. Active buyer growth accelerated from 15% Y/Y to 16% Y/Y compared to last quarter, while engagement per buyer also accelerated from 10% Y/Y to 12% Y/Y during that period. Monetization of all this traffic also accelerated compared to Q4, with ad revenue sequentially moving from 70% Y/Y to 80% Y/Y growth thanks to more advertisers and higher spend per customer.

Its end-to-end logistics network, like for Amazon and Mercado Libre, is the gas to this thriving marketplace’s engine. They’ve carefully built a massive footprint throughout Southeast Asia and increasingly Brazil to match world-class selection with reliable delivery, compelling pricing and a slew of merchant services to handle the end-to-end fulfillment process (via SPX Express).

Their instant and same-day delivery network in Indonesia is developing as hoped for, with 35% growth in order volume fulfilled within this quick window. Cost per order also fell by 20%, as SE shows economies of scale can help more expensive fulfillment services grow efficiently enough to make rational sense. It’s also helping them add more perishable inventory and build on the quality of its ecosystem. This includes new partnerships with large Indonesian convenience store and pharmacy chains, with their 7,000 offline stores now offering inventory within SE’s marketplace. This is accelerating e-commerce penetration rate gains in that market.

All in all, 33% of SPX Express deliveries are now executed within 24 hours, which is far higher than deliveries relying on 3P operators. As SPX rises as a percentage of total volume fulfilled, service speed should just keep improving – which always feeds higher conversion rates.

In Taiwan, 50% collection point footprint expansion fostered a 12% reduction in average buyer waiting time and 10%+ Y/Y GMV growth (they didn’t get more specific than that). While its whole business is expanding nicely, momentum across its e-commerce markets is strongest in Brazil. That’s where growth is the fastest, while SE maintains some level of undisclosed profitability there despite being in an investment phase. They added 3 new fulfillment centers (5 total) and cut delivery time by a full day while accelerating merchant growth as a result. This is also helping them become a more serious player in big ticket and bulky items, where MELI’s lead is largest.

Shopee – Deepening Engagement:

The loyalty program also continues to impressively scale. It's up to 10M members after adding nearly 3M members in just the last 90 days. Overall, these members consistently deliver a 10%+ average GMV boost (up to 40%) and account for nearly 20% of total volume in its core Asian markets. This is really important. It’s how you build habits, deeper loyalty, higher retention, stronger lifetime value and all of the other good things that coincide with successful loyalty program adoption for giant marketplaces. It’s the highest quality part of this business and it is rising expeditiously. That will certainly continue following a Brazil launch last month.

Their content partnerships are also amplifying Shopee’s success. Live streaming + short-form video orders rose 50% Y/Y and reached 25% of total physical orders as Southeast Asian markets remain more developed from a streaming commerce perspective than the Western World. Interesting to think about what kind of tailwind this could be for North American and European leaders if they can crack this code as well. And we’re now seeing that rapidly play out for titans like Google and Meta – two close partners for Shopee and Sea Limited. YouTube orders were up 100% Y/Y and Meta Family of Apps (FOA) affiliates rose 30% sequentially to 4.5M while the relationship expanded to Indonesia.

Show me the Monee:

Monee had a standout growth quarter for the company. Like MELI, they’re revving the credit origination engine, with 71% Y/Y principal outstanding growth to reach $9.1B. Their delinquency rates were also encouragingly stable on a sequential and Y/Y basis at 1.1%. No deterioration here despite the torrid pace of proliferation, 4.9M first-time borrowers and 35% Y/Y total borrower growth to reach 38M. Really good risk management here. Loan size per customer continues to rise as SE debuts localized credit products in Brazil and grows more confident in underwriting. Like other marketplaces with credit products, this company has the luxury of dense repayment history data from their customer base, and pairs that with short duration credit to maintain flexibility and resilience across cycles. They’re able to very quickly pull back when need be.

Going back to Brazil for a moment, like for Shopee, this is the fastest-growing (also the newest) fintech market for the company. They just crossed $1B in loan book size (+250% Y/Y) and enjoyed a noticeable uptick in interest following the aforementioned introduction of more locally relevant credit products. Their buy now pay later (BNPL) is now up to 10% of Shopee GMV as of Q1 and new licensing in the nation will allow SE to keep introducing more products to keep augmenting the already strong value proposition.

- Off-Shopee (different merchants) BNPL volume is now 20% of the overall portfolio.

Garena:

Performance across its legacy Free Fire and Arena of Valor games was strong. And while there are some programs and initiatives helping demand, that’s always the case. They do not see rising strength for this segment as a “one-off,” but a culmination of the work done and investments made to position Garena for better days. Those better days are now here.

They’re starting to get better at building promotions and limited-time themes for broader audiences, which is allowing them to extract more value from the same amount of work and appeal to more gamers. This year, that included a Ramadan theme that they elected to make more subtle so that it looked like a desert concept to people who don’t celebrate or know much about that holiday. This drove 70% Y/Y social media impression growth to reach 120B. Elsewhere, collaborations with popular content creators and brands also continues to fuel growth for the segment, with a “Jujutsu Kaisen” collaboration driving 700M views and healthy incremental interest.

- Quarterly Active Users (QAUs) continued to rise modestly Y/Y to nearly 667M while Quarterly Paying Users (QPUs) rose by 12% Y/Y compared to 15% Y/Y growth last quarter. This helped bookings per user rise 20% Y/Y.

AI:

AI-powered search and product recommendation enhancements led to a 14% Y/Y conversion in purchases, as this company joins others like META in showing they can turn investments into tangible engagement and monetization gains in their ecosystem. Not speculative or hoped-for value creation. Concrete value creation. On the cost side, they’re now up to 80% of customer service queries fielded by AI. This is already delivering a 30% cost-per-contact reduction… meaning more room to invest in core growth initiatives rather than having to spend so much on maintaining the business you’ve already won.

Looking ahead, they’re testing consumer and merchant-facing AI shopping assistants, with plans for ongoing AI-inspired ad targeting upgrades to turbo-charge that segment’s already great progress.