1. Apple (AAPL) – Earnings Review

Apple needs no introduction.

a. Demand

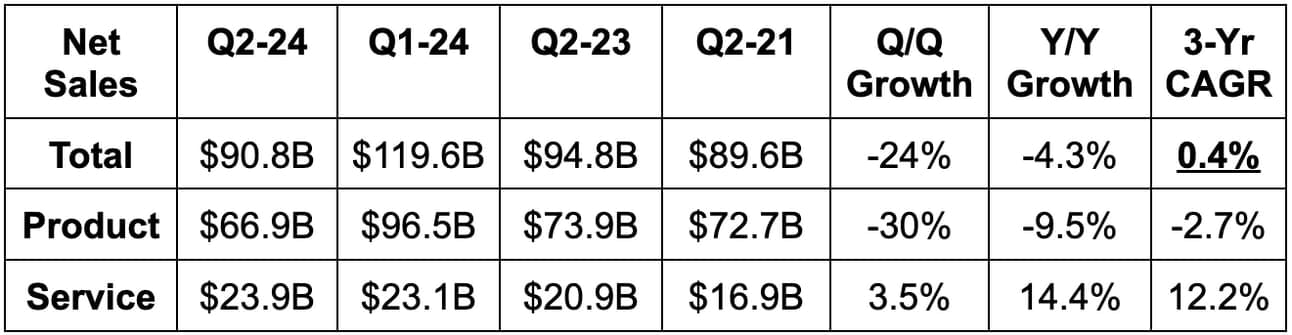

- Beat revenue estimates by 0.2% & missed guidance by 1.6%.

- Services growth of 14% Y/Y was much better than its 11% Y/Y guide.

- Product revenue was light.

b. Profitability & Margins

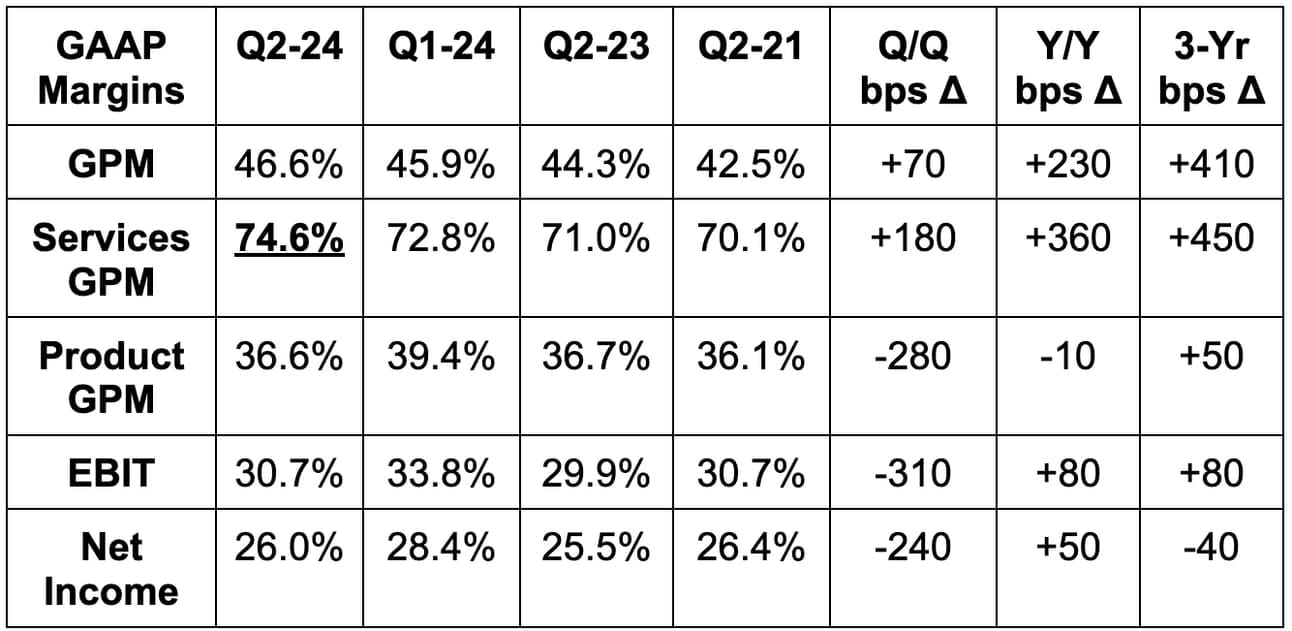

- Slightly beat GAAP gross profit margin (GPM) estimates & slightly beat identical guidance

- Beat EBIT estimates by 0.7% & missed guidance by 1.8%. EBIT fell slightly Y/Y.

- Beat $1.51 GAAP EPS estimates by $0.02. GAAP EPS was flat Y/Y.

- Operating cash flow generation was $22.7 billion vs. $28.6 billion Y/Y.

c. Balance Sheet

- $67B in cash & equivalents; $95B in non-current cash equivalents.

- $105B in total debt.

- Dividends were roughly flat Y/Y, but Apple just approved a 4% boost.

- Share count fell 2.4% Y/Y. It added another $110 billion to its buyback program. This is worth about 4% of its gigantic market cap and represents a dollar figure larger than Bulgaria’s GDP. Casual.

d. Guidance & Valuation

Apple guided to low single digit revenue growth for next quarter. Sell-side was expecting 1.2% Y/Y growth, so I think we can call this a small beat. To me, “low single digit” means 1%-3% and so 2% growth at the midpoint (4.5% Y/Y growth on an FX neutral basis). It sees services growth remaining in the low double digits. Guidance implies that iPhone revenue will again decline Y/Y next quarter. Its gross margin guidance was 46% and in line with expectations, which means implied gross profit guidance was slightly ahead. GPM guidance assumes some memory input cost inflation. Taken together, and assuming the revenue guide means 2% Y/Y growth, EBIT guidance of $24 billion was in line. The guide assumes no change in macroeconomic dynamics.

Apple trades for about 24x-25x next 12 month (NTM) earnings with low single digit earnings growth expected over that time period.

e. Call & Release Highlights

Demand Overall:

Apple set a new revenue record in 12 countries this quarter. That list includes important growth markets like Spain, Mexico, India and multiple Middle Eastern nations. For product revenue specifically, the weakness needs more context. Apple is lapping a Q2 2023 period in which supply chain recovery unleashed pent-up demand. That unleashing added $5 billion to Q2 2023 iPhone revenue results. Last year’s pull-forward means this year’s tough comp. This is why iPhone sales fell 10% Y/Y. Excluding this atypical comp item, iPhone revenue fell by 0.7% Y/Y. iPhone revenue did grow in Mainland China, as it enjoyed the top two selling smartphones in that country (per Kantar research). Surprising, after all of the negative alt data we’ve seen. But? Alt-data is usually anecdotal and noisy. Outside of China, iPhone was the top seller in the U.K., France, Australia, Germany, Japan and (obviously) the USA. Per 451 research, this product maintained its 99% customer satisfaction rate.

Apple was asked about the China opportunity over and over again during the Q&A. Leadership remains confident in the opportunity and has several initiatives in place to improve performance in what it calls its most competitive market.

Outside of the iPhone, Mac and iPad both maintained 96% customer satisfaction rates; Mac revenue rose 4% Y/Y and iPad fell 17% Y/Y. Declines in iPad were due to comping over strong product launches. Wearables, Home and Accessories fell 10% Y/Y due to successful launches in the Y/Y period (just like with iPad). Active Install bases for ALL hardware products in ALL geographies set new records.

I get that many think hardware growth is going to be hard to find for Apple in the future. I don’t really agree as an innocent bystander. 50% of iPad buyers and 67% of Apple Watch buyers this quarter were brand new to the products. There is still a runway here to complement faster, higher-margin services growth. And hardware comps will get easier.

From a services point of view, the 14% Y/Y revenue growth metric was excellent. Apple Pay, streaming, brisk paid account growth and overall engagement strength all helped drive this outperformance. It expects this momentum to remain strong.

Year to date, revenue is roughly flat. This is being hurt by foreign exchange (FX) headwinds and one less week of sales vs. the Y/Y period. Apple could really use a growth re-acceleration in the coming quarters to make the growth multiples look a bit less steep vs. others. Fortunately, that acceleration is expected. Sell-siders see Apple exiting the year at +5% Y/Y revenue growth — with more acceleration thereafter.

By Geography:

- The Americas revenue fell slightly.

- Europe revenue rose slightly.

- Greater China fell 9% Y/Y.

- Japan fell 13% Y/Y.

Vision Pro:

Apple remained steadfast in its optimism surrounding this product. I’ve seen multiple 3rd party reports saying it’s cutting production targets due to underwhelming demand and high return rates. While that’s not ideal, it’s also not surprising considering this is the very first iteration of a new computing form factor. Building product-market fit will take time for Apple… just like it has for Meta. I envision headsets being mocked, criticized and disregarded until the technology is miniaturized enough to drive ubiquity. I demoed the Vision Pro, and it’s just not comfortable to wear for long periods of time. That will change as Apple and Meta make these headsets look more and more like a pair of glasses over time. When that happens (I think it will), the mocking will quickly shift to rapid adoption. Give it time.

50% of the Fortune 100 is now exploring how to build apps on this hardware.

Capital Expenditures (CapEx):

As is usually the case, we got a lot less color on CapEx plans compared to every other mega-cap. Apple can get away with this (Wall Street darling as it should be) and it makes sense to avoid oversharing when it can. It did remind investors that its broad supply chain does allow it to share some CapEx intensity with 3rd parties. This includes data center CapEx, and could help curb growth in this expense compared to others.