Today’s Piece is Powered by Savvy Trader:

1. Airbnb -- Starwood & Greystar

Airbnb is expanding its Airbnb-Friendly Apartments program to more landlords and buildings. This week, it announced the addition of Starwood Capital Group and Greystar Real Estate (2 massive landlords) to the initiative. The program involves landlords permitting renters to use their living quarters for Airbnb hosting on a part-time basis. Renters enjoy the added income, and landlords enjoy a powerful top-of-funnel for new renter demand by adding this perk. Airbnb will be displaying these buildings on its app for renters searching for apartments to lease. Considering its massive scale, this will be a demand driver to reduce both marketing spend and vacancy rates for landlords.

Many, many landlords do not allow short-term subleasing. That reality offers these participating players a real point of differentiation for attracting tenants. Specifically, nearly half of all renters pay more than 30% of their salary on rent. This makes secondary income streams like this one enticing -- especially as remote work and a nomadic lifestyle become more popular. To attract these landlords, Airbnb has created “visibility and controls” and “a framework to get landlords comfortable with this.” Its software ensures landlords always know who is hosting and how many guests are staying with easy enforcement actions to take against rule violators.

Airbnb is going very slowly with the rollout of this project to ensure it works perfectly for landlords. It wants to change the negative perception associated with short term rentals to one that centers on incremental revenue opportunities rather than added asset risk. Its insurance program works wonders in facilitating this as well. Today, Airbnb-Friendly Apartments covers 230 buildings across 38 U.S. cities with plans to grow from here and expand globally. If the initial launch goes well with Starwood or Greystar, there could be many more buildings to come from these two alone.

And According to Co-Founder Nate Blecharcyzk, there’s a large backlog of landlords ready to join. A short report published this month offered a main bear case that landlords would cut Airbnb entirely out of operations and vertically integrate the services. Well? Here we have two of the most capable landlords in the country turning to Airbnb instead.

2. Uber Technologies (UBER )-- Cannabis, Robots and Liquidity

a) Cannabis & Pets

In a world of perishable goods delivery, the cannabis delivery opportunity is a potentially lucrative extension of Uber’s operations. Federal regulation in the U.S. doesn’t allow for its participation today, but it’s legal in Canada -- and Uber is taking advantage. This week, it announced a new partnership with a popular cannabis marketplace called Leafly. I guess this is Uber’s way of saying Happy 4/20.

Between Leafly and Weedmaps, these two companies essentially own the e-commerce shopping space. And now Leafly will merge this market power with Uber’s leading delivery capability. I’m bullish on the cannabis opportunity for Uber as regulation continues to open up. The timeline there is about as unclear as things get, but legalization in the U.S. is a “when not if.” 68% of all Americans (and a majority of both wings) support it.

Uber Eats also added PetSmart and its 1,600 locations as a store delivery option this week. The Eats segment is fixated on allowing consumers to have whatever they want as fast as they want. Both of these news releases are part of building out that vision.

b) Robots

Uber and a robotics delivery company called Cartken are expanding a newer partnership. With Cartken’s technology, Uber Eats consumers in Fairfax County’s Mosaic District in Virginia can have goods delivered by autonomous robots. Autonomy will be a massive piece of Uber realizing its full margin and service quality potential. Drivers are expensive and unpredictable; robots are cheaper and fully controllable. I know this sounds insensitive to the drivers who will ultimately be displaced, but it is a reality.

Uber is already morphing into a cash printer before our eyes through needed cost base rationality and tighter focus/execution. Autonomous delivery would be another large margin augmenter.

c) Russia

Uber has officially exited Russia. It sold its remaining stake in Yandex.Taxi to Yandex for $702 million. Uber entered the market in 2017, sold off its delivery equity in 2021, and finished the liquidation process this week.

Between this and the $400 million created last week via selling part of its Careem business, Uber has added over $1 billion in cash to its balance sheet. The rumored spin-off of its freight business would add even more. As it inflects to profitability, its balance sheet continues to look healthier and healthier. It still has a few billion in investments that it could liquidate if it so chooses… but there’s no pressing need for any sales today.

Savvy Trader is the only place where readers can view my current, complete holdings. It allows me to seamlessly re-create my portfolio, alert subscribers of transactions with real-time SMS and email notifications, include context-rich comments explaining why each transaction took place AND track my performance vs. benchmarks. Simply put: It elevates my transparency in a way that’s wildly convenient for me and you. What’s not to like?

Interested in building your own portfolio? You can do so for free here. Creators can charge a fee for subscriber access or offer it for free like I do. This is objectively a value-creating product, and I’m sure you’ll agree.

There’s a reason why my up-to-date portfolio is only visible through this link.

3. Lululemon Athletica (LULU) -- Mirror

Lululemon acquired Mirror for $500 million during the heat of the pandemic. Stay at home orders fostered a remote fitness boom which Mirror greatly enjoyed. Like for Peloton and others, the end of the pandemic conversely led to a sharp mean reversion in demand.

To combat this, Lululemon has been shifting its subscription and fitness content partnerships to a more software-heavy approach which doesn’t rely on Mirror hardware as an access prerequisite. It also took a $442 million goodwill impairment charge (nearly 90% of the original purchase price) as part of this pivot. Customer acquisition cost (CAC) for Mirror users is simply not compelling enough to keep investing -- it’s throwing good money after bad and weighing on Lulu’s overall margin profile.

The newfound hardware independence allowed its “Essentials” loyalty program tier to boom in membership growth; in just 9 months it has 9 million members. Notably, this program involves zero access to discounted products. It only offers early access and a few other perks which is clearly all Lulu needs to do to sharpen its customer engagement by a full 9%.

“Since our acquisition, the at-home fitness space has been challenging. While members love our content, hardware sales did not match expectations. As we continue to invest prudently in this business, we are evolving the model from being focused on hardware-only to offering content through a digital and app-based solution. We think the lower cost of entry will allow us to more easily migrate and attract guests into it.” -- CEO Calvin MacDonald

This past week, rumors swirled around Lulu exploring a sale of Mirror once and for all. Candidly, I don’t really care what the price tag would be on this transaction. Liquidating it for whatever Lulu can get and removing the fixed expenses from its cost base is the right decision. To me, leadership liquidating the asset would mark its willingness to right a previous wrong rather than doubling down. In hindsight, the purchase was a mistake and there’s no need to compound the blunder. Hydrow is rumored to be an interested buyer.

4. PayPal (PYPL) -- Case Study

Seguros Caracas is a large insurer in Venezuela. It wanted to add the ability to receive payments in U.S. dollars, needed to raise buyer confidence and wanted to responsibly juice its approval rate. PayPal allowed the customer to raise volume by 189% and boost approval rates by 13% using its underwriting models.

5. The Trade Desk (TTD) -- Magnite

Magnite is looking to cut demand side platforms (like The Trade Desk) out of the programmatic advertising equation. With a new product called ClearLine, publishers will gain direct access to advertisers with a direct data channel as well. The Trade Desk has been making similar moves with its OpenPath product which allows clients to perform key supply side tasks like yield management on their own. Supply side and demand side ad platforms continue to slowly converge. I think The Trade Desk is in a better position to raise wallet share than supply side players like Magnite. Its services are less commoditized which is why its take rate is so much higher than other supply chain pieces. Its scale and partnerships with essentially all relevant ad buyers while it delivers superior ad returns by cutting booking costs in half makes it difficult to displace.

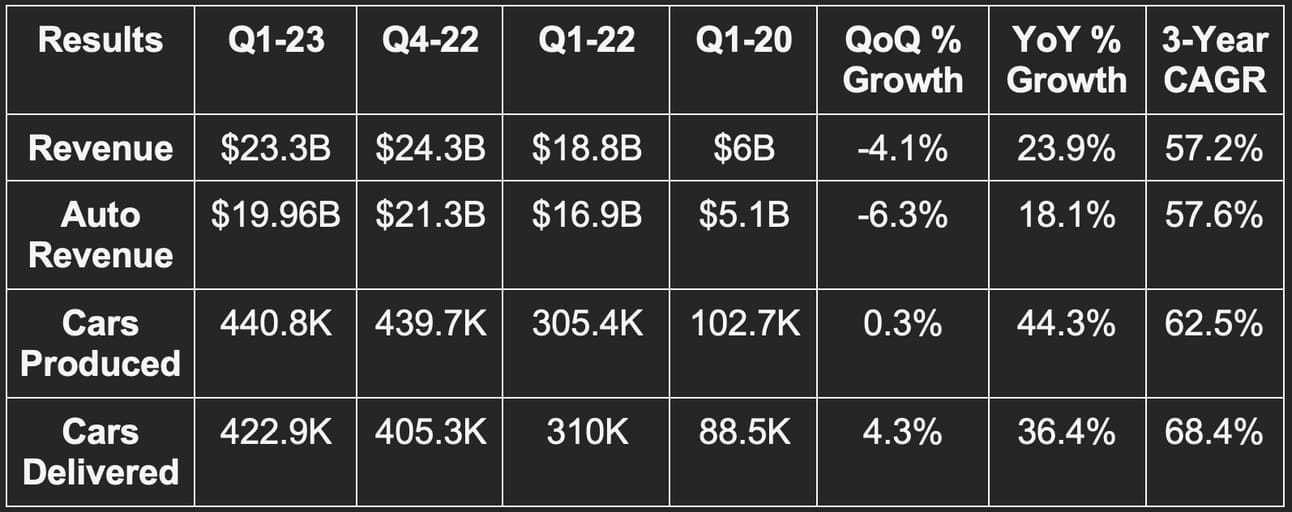

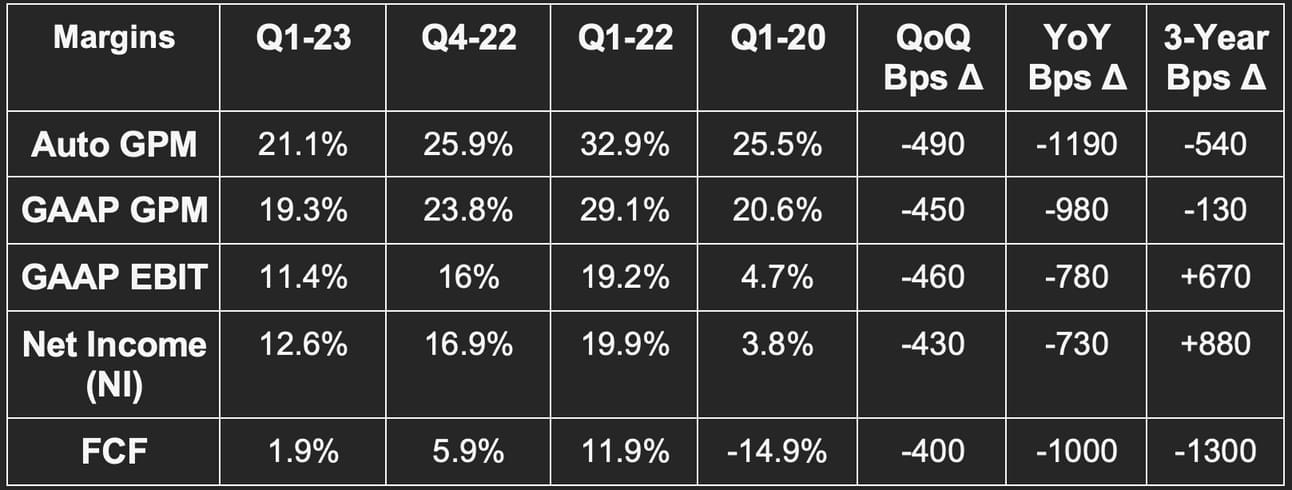

6. Tesla (TSLA) -- Earnings Review

a) Results vs. Expectations

- Met revenue estimates.

- Missed EBIT estimates by 6.5%.

- Met GAAP & non-GAAP EPS estimates.

- Sharply missed FCF estimates by nearly 90%.

- Missed GAAP GPM estimates by 140 basis points (bps).

- Missed auto GPM estimates by 190 bps.

- It also slightly beat both production & delivery estimates as reported last week.

b) Forward Guidance

Tesla reiterated its long-term guidance of a 50% volume CAGR and among best-in-class auto EBIT margins. It also guided to 1.8 million vehicles produced for 2023.

c) Balance Sheet

- $22.3 billion in cash & equivalents.

- $1.5 billion in current debt.

- 2% basic share count growth YoY.

- Inventory rose by 12% QoQ and 115% YoY.

d) Letter & Call Highlights

Tesla’s 3-year revenue CAGR sits at 57.2% vs. 48.6% last quarter and 50.5% 2 quarters ago.

Macro, Pricing, Margins & Production:

Leadership spoke on macro headwinds as providing a “unique opportunity” to grow the company’s production efficiency and share leads over incumbent car makers. It “aims to leverage its position as a cost leader” to accomplish this with continued focus on cost optimization. Projects like vertically integrating controllers and opening its charging network to other EV makers are examples of how it can cut costs while extracting more value from its investments. Still, price cuts this year have lowered Tesla’s 20% auto GPM ex-credits floor for 2023 according to CFO Spencer Neumann.

More sources of cost efficiencies expected via:

- Ramping the Austin and Berlin factories to full capacity.

- One time warranty adjustments on older models not recurring.

- YoY impact of higher deferred revenue from autopilot features normalizing.

- “The beginning of some commodity cost reductions.”

- New 4680 cell battery announced at its investor day requires 70% lower CapEx per gigawatt hour than older models at scale. This will be a large boost to free cash flow.

- Considering OCF was $2.5 billion with $2.1 billion in CapEx leading to just $400 million in FCF, this matters a lot.

- Structural pack battery design comes with 50% less CapEx needs and ⅓ of the factory footprint needs of older models.

- Larger cell capacity also means more range and higher energy efficiency (for lower cost).

- The opening of its lithium refinery in Corpus Christi is set to reduce cost and “produce a byproduct that can be repurposed in construction” as an added layer of efficiency. Tesla DOES NOT WANT to be doing this itself. It’s doing it because nobody else is fulfilling the need.

Notably, Tesla continues to favor production volume and deliveries over optimizing the margin profile. It’s willing to “lay the groundwork today” by selling cars at lower margins and “harvesting more margin” as autonomous driving and software upgrades unlock recurring revenue streams. This willingness also makes Tesla inherently more difficult to compete against. It also could foster an inventory glut over time. Inventory levels are already elevated, but importantly, Elon told us that “orders remain in excess of production.”

“Near term pricing considers a long-term view on per vehicle profitability given the potential LTV of autonomy, supercharging, connectivity and service.” -- Elon

Free cash Flow:

“Q1 was our third quarter in our plan to move to a more regionally balanced mix of build and deliveries. This results in lower deliveries and production within a quarter due to a higher volume of cars in transit at the end of the quarter and has an associated impact on quarter-ending free cash flows. This was particularly prevalent in Q1 for S and X as we began exporting cars for international deliveries.” -- CFO Spencer Neumann

Auto Business Updates:

- Model Y was the best-selling vehicle of any kind in Europe during the quarter and the best-selling non-pickup in the USA.

- Cybertruck deliveries are on track to begin this year.

- 4,947 supercharger stations this quarter vs. 3,724 YoY.

- Launched auto sales in Thailand to a “very positive reception.”

- Thinks it will get to 2 million cars produced this year if macro cooperates and 1.8 million if it doesn’t (which is the base case).

Non-Auto Revenue:

- Energy storage production capacity at its factory in California is ramping nicely with it now working on opening a new energy storage plant in Shanghai.

- 67 solar megawatts generated vs. 100MW QoQ & 48MW YoY. The sequential decline was a result of “volatile weather and supply chain challenges.”

- Energy storage deployed of 3,889 megawatt hours vs. 2,462MW QoQ & 846MW YoY. It will eventually include production and delivery metrics from storage alongside its quarterly auto disclosures.

- Storage and energy generation businesses are expected to carry a “mid 20%” gross margin at maturity. Neither are there yet but both are progressing nicely.

- It continues to open up its charger network with 50% of its Europe stations now open to all EV types.

Dojo:

Dojo is Tesla’s supercomputer project being built to season its AI models. Leadership assured us that while it continues to buy computing capacity from Nvidia in large amounts, it’s also investing heavily on vertically integrating this need. It thinks Dojo could eventually benefit from lower cost of training models by an “order of magnitude.” Tesla wants to eventually sell the service as a white-label tool. Importantly, Elon still sees the success of this project as a “bit of a long shot” but with the potential reward making it worth the bet.

Full Self Driving (FSD):

“I hesitate to say this, but I think we’ll do FSD this year.” -- Elon

7. Netflix (NFLX) -- Earnings Review

a) Results vs. Expectations

- Missed revenue estimates & missed its identical guide by 0.2%.

- Beat EBITDA estimates by 1.2%.

- Beat EBIT estimates by 4.3% & beat its guide by 5%. While Netflix guided to a 20% EBIT margin it posted a 21% margin.

- Beat $2.87 EPS estimates by $0.01 & beat its $2.82 guide by $0.06.

- Obliterated $782M FCF estimates with $2.11B in FCF.

- Missed subscriber net add estimate of 2.3 million by 24%.