Table of Contents

- 1. Quick Service Food & Beverage Intro

- 2. Adobe (ADBE) – Earnings Review

- 3. SoFi (SOFI) – Expensive? Misunderstood?

- 4. Walt Disney (DIS) – India

- 5. Amazon (AMZN) – 2024

- 6. Uber Technologies (UBER) – Miscellaneous

- 7. Meta Platforms (META) – Threads (Twitter Copy C …

- 8. Meta Platforms (META), Alphabet (GOOGL), The Tr …

- 9. PayPal (PYPL) – Data, Regulation & Rule Breakin …

- 10. Match Group (MTCH) – Update and Investor Confe …

- 11. Earnings Roundup

- 12. Macro

- 13. Portfolio

1. Quick Service Food & Beverage Intro

a. Setup

Over the next quarter or so, I will be publishing investment case articles on companies in the quick service restaurant (QSR) industry. To avoid sending a 100-page article, I’m going to send out mini dives into two companies from the landscape at a time. The first piece will be published later this month and will cover Cava and Sweetgreen.

I think this is a better format than the prior deep dives. It will be 90% as detailed as those were, with 100% of the important detail, and I’ll be able to send them out more frequently. This way, the information will be more current and more digestible. Furthermore, I think this approach will give you a better view of my investment thought process. It will also allow you to learn more about the sector overall and compare similar business models. As generalists, it is easier to build conviction by studying multiple companies in a sector rather than a single company in isolation. This tweak is my way of pulling back the curtain on how I dissect a new sector.

b. Sector Demand Intro

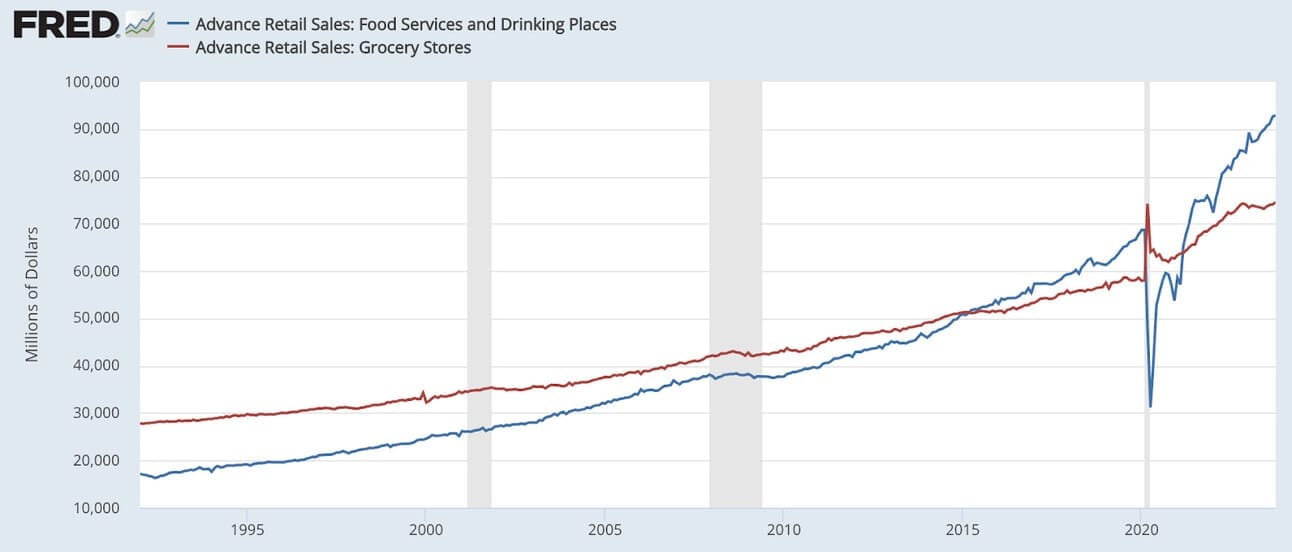

Quick service is a wonderfully stable secular growth story. Around 1992, per FRED, monthly grocery sales of roughly $28 billion were 63% larger than total restaurant service volume. Today, that has entirely flipped with $93 billion in monthly restaurant volume. That’s 25% larger than the grocery space as a whole. The 5.6% compounded annual growth rate (CAGR) for restaurants leaves a compelling opportunity for share takers in the sector. Depending on which research vendor we trust, forward CAGR expectations range from 6%-10% over the next several years. There’s no slowdown in sight.

Notably, food and drink service growth did flatline during the great financial crisis and did tank during the pandemic. Still, the sector has shown impressive resilience in its ability to recapture solid, run-rate growth in excess of U.S. GDP growth. Consumers, more and more, are leaning on restaurants for consumption as younger generations flock to services over goods. That reality has been turbo-charged by the proliferation of convenient delivery options. That is the growth setup for the sector.

c. Sector Margin Intro

Aggressive, macro-based margin headwinds are easing. Input cost inflation of raw ingredients continues to tumble, which helps all QSR margins (assuming at least constant menu pricing). It’s much harder to maintain traffic and profitability with a CPI at 8%. Few companies have the ability to hike menu prices at that clip to hold margins steady. It’s a lot easier to maintain or even grow margin with a CPI falling towards 2%.

A more gradual pace of input cost inflation allows chains to avoid sticker shock in their quest for margin preservation and makes traffic easier to maintain. In some cases, as we’ll see in the deep dives, price growth for some input costs like salmon has actually turned negative for players like Sweetgreen.

Further, in terms of expansion, the falling cost of capital should accelerate the pace and profitability of new restaurant chain openings as expansion becomes cheaper. Sky-high rates have weighed heavily on fixed business investments. Now, they appear to have peaked. That is the simplistic set-up. Using this as the 30,000 foot view, we are set to explore specific company investment cases. Expect the first part of this sector dive to be published this month.

2. Adobe (ADBE) – Earnings Review

Adobe is a software giant. It provides programs to create and imagine, handle customer interactions and process documents. Revenue is split into two main buckets: Digital Media and Digital Experiences. Digital Media is made up of its “Creative Cloud” and “Document Cloud.” The Creative Cloud includes Photoshop and Illustrator. It’s what empowers creation, iteration and perfection of digital design. The Document Cloud, including the ubiquitous Adobe Acrobat, allows for secure PDF management and collaboration – among other things.

Finally, its Experience Cloud includes Adobe Analytics and other products like “Campaign.” Campaign is its intuitively-named marketing campaign tool. Experience Cloud covers end-to-end customer interactions with a real-time customer data platform (CDP) to ensure those interactions are optimized. It also publishes some great macro data on overall commerce spend.

a. Demand

- Beat revenue estimates by 0.6% and beat its guide by 1.0%.

- Its 13.9% 3-yr revenue compounded annual growth rate compares to 14.8% as of last quarter & 15.5% 2 quarters ago.

- Beat Digital Media revenue guidance by 0.9%.

- Beat Digital Experience revenue guidance by

b. Margins

- Beat $3.11 GAAP earnings per share (EPS) estimates by $0.12 & beat guidance by $0.10.

- Beat $4.14 EPS estimates by $0.13 & beat guidance by $0.15.

- Earnings per share rose by 17% Y/Y in 2023 as a whole.

- It slightly missed EBIT estimates by a fraction of a percent. It doesn’t provide guidance for this metric.

Operating cash flow (OCF) margin was impacted by an $826 million U.S. tax payment that was deferred from Q2 and Q3. Without this one-time hit, OCF margin would have been 48.1%.

c. Guidance

Next quarter guidance missed slightly on revenue, but beat slightly on both GAAP and non-GAAP EPS.

For the full year guide, revenue was 1.4% light. GAAP EPS was $0.18 (or 1%) light vs. $17.98 expectations. Non-GAAP EPS was $0.37 (or 2.8%) ahead of $13.28 estimates. It generally likes to offer highly conservative preliminary annual guidance.

d. Balance Sheet

- $7.84 billion in cash & equivalents.

- $3.6 billion in debt.

- Basic share count fell 2.2% Y/Y; diluted share count fell 1.5% Y/Y.

- It has $3.15 billion in current buyback capacity.

e. Highlights

GenerativeAI:

Adobe plans to lean on what it sees as its two strengths to capitalize on the GenAI wave: Data and model-building. The data item is simple. Its scale is massive. Generative AI models need massive sums of data to be trained. The model building part is a bit more subjective. Adobe Firefly is its group of GenAI models. It enhances use cases among its current products, infuses new layers of automation into them and tears down the barriers to content creation.

Figma:

Figma is a platform for next-generation digital design. Adobe plans to purchase this company to introduce incremental value to its already broad toolkit. The European Commission has already pushed back on the deal for competitive concerns, but Adobe is responding to these concerns and pushing hard to close the deal. Ideally, that will happen some time next year.

Digital Media – Creative Cloud:

Creative Cloud had a strong quarter. The company did hike pricing here last month, but growth was driven by paid subscriptions. Most of the benefit from the hike has yet to be realized.

New GenAI product integrations are allowing clients to keep up with increased consumer demand for beloved brand content. These integrations are diminishing friction and vastly expediting content creation to meet enterprise needs. Across imaging, design, video and 3D, Creative Cloud + Firefly is leading to accelerating strength in mid and large client wins.

Along these lines of increased content demand, GenStudio is another key Adobe product. This is essentially an upgraded version of Adobe express – its end-to-end content creation product. GenStudio is GenAI-based and automates that creation from “ideation to delivery.” Automation unlocks a lot more capacity to create more content.

- Deloitte and Pepsi were among highlighted wins for the quarter as the segment enjoyed a new record for net subscriber additions.

Firefly debuted 3 new models for Creative Cloud during the quarter including the Firefly Vector Model. Per investor materials, the Vector Model is the first GenAI model to transform text into “stunning vector artwork like icons and even entire scenes.” There are a lot of text to image models, but this supposedly goes a lot deeper. As an important aside, it’s adding GenAI credit packs to monetize this new usage growth.

- While strength here was broad-based, emerging market strength was called out as a standout.

- Frame.io (video-based creation and collaboration) enjoyed a record year in 2023 for net new ARR.

Digital Media – Document Cloud:

Adobe Acrobat for Web enjoyed 70% Y/Y growth in monthly active users. It also delivered a 400% Y/Y “surge” in link sharing for PDF collaboration. Thanks to Liquid Mode, Acrobat Mobile reached 100 million users. Liquid Mode is an AI powered tool to automatically retrofit web-based PDFs for mobile viewing.

- Integrated Acrobat with all Adobe Express Workflows to pair powerfully artistic content creation with PDF formatting.

- The segment won Bank of America, the Department of Veterans Affairs, Mastercard and State Farm as new customers during the quarter.

- GenAI tools for the Document Cloud are in private beta.

Digital Experiences:

As we’ve already covered in previous articles, Adobe Analytics is a go-to provider for consumer spend data. It reported 7.5% Y/Y holiday weekend growth, which compares very well to expectations of 5.5% growth. This is where the Experiences Cloud thrives. If consumers want to spend more, brands will have more drive to optimize every interaction to maximize revenue per touchpoint. That’s what this suite does. Its real-time CDP gives companies a holistic, end-to-end control panel of individual customer interaction profiles at near-endless scale.

Adobe Experience Platform (AEP) is its product bundle that combines all of the Experiences Cloud. Like other platforms plays in software that can drive vendor consolidation and cost savings, this platform is thriving in today’s environment. AEP had its first $100 million net new business quarter. Its entire book of business sits at just $700 million, making that feat very notable. Overall, the AEP and native apps business rose 60% Y/Y. Coke, Vanguard, Marriott and Unilever are among large customer wins for this segment during the quarter.

f. My Take

This is one of those wonderfully boring and highly consistent performers. It’s a titan in creative software and a large player in customer relationship management as well. The underwhelming annual guide will likely be raised throughout 2024 if history is any indication. A fine quarter from an elite company. Enough said.

Long-Term Mindset is a FREE weekly newsletter emailed each Wednesday. Each issue contains five pieces of timeless content to encourage you to think long-term. All issues can be read in less than 1 minute. There’s a reason why we are consistent readers and think you should be too. Subscribe here.

3. SoFi (SOFI) – Expensive? Misunderstood?

2022 and most of 2023 have been periods of me consistently and aggressively defending what I see as a pristine SoFi bull case. We’ve gotten into fine detail on accounting practices, its loan book, its balance sheet and more. We’ve dissected and dismantled all of the risks that seem to magically become more pressing when the stock price falls for a few weeks. But it isn’t falling anymore.

With the stock price now responding positively to macro events, the conversation needs to shift. I wanted to unpack my thoughts on when SoFi the stock will become “expensive” if it continues to vertically and rapidly move higher. Further, I wanted to provide a feel for when I’d consider first trimming.

SoFi is a bank that doesn’t look like other banks. It owns its tech stack, it has no branches, it offers lower return products that most banks shy away from, and, most importantly, it has no GAAP net income. That last item has forced investors to value this bank disruptor based on an enterprise value (EV) to EBITDA multiple. Candidly, simply valuing a banking disruptor based on EBITDA makes me cringe. I do it by necessity here. Luckily, I won’t need to as it turns GAAP net income positive this quarter.

I think a lack of GAAP net income up until now is a large, large reason for why SoFi’s stock has been so unloved and misunderstood for most of its public life. Most investors (besides my readers) are somewhat lazy. They’ll go to Yahoo Finance, read a P/E ratio, see that it’s negative, and never give the company a second look. They won’t study margin inflection trends, unique accounting items below the EBIT line, incremental margins, margin catalysts or any other detail. If the P/E looks bad, they’re done.

Well? Again, SoFi’s earnings will turn positive next quarter, and the deal-breaker will go start to away. As of now, analysts expect the firm to earn $0.07 per share next year. Between its consistent shattering of profit estimates, its pessimistic guidance assumptions, easing macro headwinds and commentary on 2024 revenue splits, I think it will keep outperforming. Furthermore, 2024 analyst estimates have more than doubled year-to-date; I don’t think they’re done moving.