Table of Contents

- 1. Cloudflare (NET) – Introduction & Earnings Revi …

- 2. Spotify (SPOT) – Earnings Review

- 3. Earnings Round-Up

- 4. PayPal (PYPL) – Reflecting on a Tough Quarter

- 5. Shopify (SHOP) & Briefly CrowdStrike (CRWD) – P …

- 6. Amazon (AMZN) – Cost Cuts

- 7. Duolingo (DUOL) – GenAI Risk

- 8. Macro

- 9. Portfolio

1. Cloudflare (NET) – Introduction & Earnings Review

In essence, Cloudflare makes the internet faster and more secure. They have a massive global Content Delivery Network (CDN) to move traffic closer to the end user, which cuts web latency. They actively assist clients in optimizing traffic speed and consistency as well. It also has a suite of security tools (firmly within network security like Zscaler) to protect customer websites from Distributed Denial of Service (DDoS) attacks, which aim to inundate and overwhelm networks with traffic. They don’t sell physical firewall hardware, but instead they offer a virtual, cloud-native “Magic Firewall” to supplant these hardware needs. It offers web application firewalls too for application-level security, while Magic Firewall is for network-level security.

A Few Key Product Categories to Know Aside from DDoS and its Next-Gen Firewall Products:

Workers Platform is its serverless (so fully managed by Cloudflare) product suite for developers to build, maintain, secure and deploy applications. This allows for caching of content and applications across Cloudflare’s global network for faster delivery. Its newer Workers AI product allows developers to access models and infuse GenAI tools like sentiment analysis into the apps and networks run on Cloudflare. Workers AI works seamlessly with its “Vectorize,” (and other vector databases). Vector refers to a style of data querying that allows for visualization of data patterns. Another key example of Cloudflare’s GenAI tools is its R2 product. This allows cloud workloads and data to be freely moved among public clouds with no tax. This use case is popular for GenAI model building and implementation as models are voracious users of data and GenAI work often spans multiple clouds.

Cloudflare Access is its Zero Trust Network Access (ZTNA) program. Zero trust means that a user or device must be constantly verified (or never trusted). Cloudflare does this in a seamless manner to minimize user friction. It considers device type, location, usage patterns (or signatures) and other contextual clues to better authorize permission requests and to know when to block those requests or request more information. It then deploys a minimal privilege approach to ensure only the necessary permissions are granted to workers. Nothing more, nothing less. This uplifts environment security vs. legacy identifiers to ensure an adversary can’t breach the most vulnerable part of a tech stack and move freely throughout it thereafter.

Secure Access Service Edge (SASE) platform is a term for how Cloudflare conjoins web performance and security use cases (such as ZTNA). This drives vendor consolidation, controls costs and augments performance. Cloudflare One is its overarching platform and product bundle subscription combining its performance and security use cases.

a. Demand

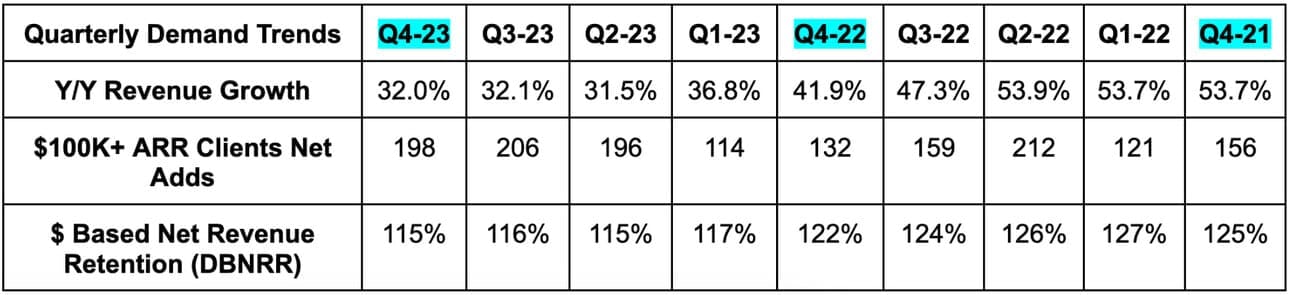

Cloudflare beat revenue estimates by 2.7% and beat its guidance by 2.9%. Its 40.9% 3-year revenue compounded annual growth rate (CAGR) compares to 43.2% as of last quarter & 45.7% 2 quarters ago.

- This was also its 2nd best quarter of $100,000 annual recurring revenue (ARR) customer additions in nearly 2 years.

- Remaining performance obligations (RPO) (a forward-looking demand indicator) rose by 37% Y/Y to $1.25 billion.

“We continue to believe that our DBNRR is stabilizing near these levels.” – CFO Thomas Seifert

b. Profitability

- Beat EBIT estimates & beat its same EBIT guidance by 40%.

- Beat $0.12 earnings per share (EPS) estimates & beat its same guidance by $0.03.

- Beat free cash flow (FCF) estimates by 32.3%.

- Note that its target gross profit margin (GPM) is 75%-77%. It’s already above that.

c. Balance Sheet

- $1.7 billion in cash & equivalents.

- $1.3 billion in senior notes.

- Share count rose by 2.5% Y/Y.

d. Annual Guidance & Valuation

Cloudflare’s annual revenue guidance met expectations. Its EBIT guidance was 1.3% ahead of expectations and its EPS guidance was $0.025 ahead of $0.56 expectations. Like Meta, Google, Amazon and many others have done, Cloudflare is extending the useful life of some infrastructure from 4 years to 5 years. That means less depreciation and so more operating income. This added $20 million to the 2024 EBIT and net income guides. Without this help, EBIT would have been about 10% light and EPS would have been $0.03 light. There is nothing shady about this accounting maneuver. It’s entirely legitimate and entirely by the book. Still, this is important context to consider. It also guided to $156 million in 2024 FCF, which is 5% light. It expects to hire at a gradual pace in 2024.

“Mixed macroeconomic data points serve as a reminder that we are operating in a business environment that is showing signs of improvement, but continues to be challenging to predict. As a result, we remain prudent in our outlook for 2024.” – CFO Thomas Seifert

Cloudflare trades for 192x its 2024 EBIT guidance and 187x 2024 EPS guidance. EBIT is set to grow by 28% Y/Y and EPS is set to grow by 19.4% Y/Y. This is among the most expensive names in the market; it has been for years.

e. Call & Release Highlights

The Platform Play:

Cloudflare’s ability to combine app performance and security, network hygiene and Zero Trust all into one interface and platform is resonating. Like other software platform plays, offering more to clients means vendor consolidation, cost savings and better product efficacy. That’s the formula Cloudflare is delivering, and it’s working. It signed a record number of new $500,000+ and $1,000,000+ customers as well as its largest new and renewal deals ever. Average contract value (ACV) booked rose above 40% Y/Y for the first time since 2021. Pipeline closure rates, average deal size and productivity all improved sequentially. All of this is even as “macro remains choppy.” Cloudflare One, defined above, was relatedly called out by CFO Thomas Seifert as a key driver of the strong quarter. Revenue from its largest cohort of clients rose from 63% of total to 66% of total Y/Y.

- Cloudflare’s vendor consolidation was cited as the reason for winning a 3-year, $33 million contract win with the U.S. Department of Commerce.

- It won a $7 million contract due to its simplified delivery of zero trust, easier integrations and a stronger strategic vision than competitors. This client also enjoyed a sharp boost to web performance.

- It won a large contract to displace a hyperscaler that couldn’t protect the client from DDoS attacks.

- It won a UK government agency despite being a late entrant into the bidding process due to tech superiority.

Go-To-Market:

Two quarters ago, CEO Matthew Prince made some harsh remarks about his sales team’s underperformance. He spoke about Cloudflare not doing enough in the world of performance management and how sales team momentum needed to greatly improve. Two quarters later, that improvement has already come. Pipeline generated from its new sales cohort is over 100% larger than the year ago hires. Account engagement also rose 350% Y/Y as the new sales team made its mark. Truly an impressive and rapid turnaround here after the Q2 2023 drama.

Cloudflare announced a change in its go-to-market team. Over the last 15 months, Marc Broditisky has been running these efforts. Per CEO Matt Prince, he did a fantastic job. He “operationalized the landing of large clients” and revamped performance management with the “discipline needed to have a world-class sales department.” This quarter, Cloudflare announced that Mark Anderson will take over Boroditsky’s responsibilities as the firm’s new President of Revenue. Anderson comes over from Alteryx (which was taken private) where he was the firm’s CEO. Prince told us that Cloudflare has wanted him in this role for years, but the timing was never right until now. He’s been a Cloudflare board member for a while, which means this should be a very seamless transition. Boroditsky will stay with Cloudflare as an advisor for a few months to avoid any operational disruption.

“I wanted to take this time to reaffirm that Michelle (COO) and I (Matt Prince) aren't going anywhere or changing our roles in any way. I wake up every morning more excited about the opportunities now to fulfill our mission of helping build a better internet. If you study iconic technology companies, they are often mission-driven, founder-led, and include a dynamic, experienced and evolving leadership team to surround the founders.” – CEO Matt Prince

AI:

Cloudflare wanted to have inference tuned Graphics Processing Units (GPUs) in 100 cities by this quarter. It reached 120 cities and reiterated plans to have these GPUs in its entire global network by the end of this year. That is a prerequisite for running GenAI use cases like Workers AI through Net’s platform. 6 years ago, Cloudflare began leaving empty slots in its servers around the world. It did this in anticipation of Worker AI GPU demand. This means it can simply plug Worker AI GPUs into its existing server infrastructure. So? GenAI proliferation will not entail hefty boosts to capital expenditures. Impressive foresight.

Since the firm’s Workers AI launched in September, usage requests are up 900%. Notably, 33% of all Workers AI requests are from clients new to the Workers Platform. This tells leadership that GenAI will not only create new demand streams, but accelerate existing ones too. While Workers AI brings a bevy of model building and usage options, Vectorize allows these models to be visually enriched with a client’s custom first party data to drive more relevant use cases. Worker AI is driving strong, complementary demand for Vectorize thus far.

f. Take – Nothing but Net

Cloudflare is a fantastic company and this quarter made that clear once more. Its platform is clearly clicking with large clients and its margin path is impressive to say the least. The report wasn’t incredible or jaw-dropping, but it was rock-solid across the board. I continue to find the firm too pricey to personally own despite the compelling value proposition. Regardless, congratulations shareholders on nearly 200% returns from the lows less than a year ago. Take a bow.

2. Spotify (SPOT) – Earnings Review

“While I'm pleased with the level of growth we saw in 2023, perhaps what is even more gratifying is that it also marked a very different year for Spotify, a true evolution in how we operate our company. A year where we started to prove that we're not just a company that has an amazing product, but one that also is building a great business.” – Founder/CEO Daniel Ek

a. Demand

- Missed revenue estimates by 1.2% & missed guidance by 0.8%.

- Constant currency revenue growth was 20% Y/Y vs. 17% Y/Y last quarter due mainly to price hikes. Premium revenue rose by 21% Y/Y on an FX neutral (FXN) basis. Ad-supported revenue rose by 17% Y/Y on an FXN basis.

- Its 19.1% 3-year revenue CAGR compares to 19.3% last quarter and 18.9% 2 quarters ago.

- Slightly beat monthly active user (MAU) guidance & estimates.

- Beat premium subscriber estimates by 0.5% and slightly beat its guidance.

b. Profitability

- Beat non-GAAP EBIT guidance by 84%. This excludes €143M in severance charges incurred during the period.

- Missed -€0.26 GAAP EPS estimates by €0.10 & met GAAP EBIT estimates. €143M in severance charges hit GAAP margins this quarter.

- Crushed FCF (non-GAAP metric) estimates by about 150%.

- GAAP GPM of 26.7% was 10 bps ahead of expectations.

c. Balance Sheet

- €4.3B in cash & equivalents. €1.2 billion in long term investments.

- €1.2 billion in convertible notes.

- Basic shares +0.5% Y/Y; diluted shares -1% Y/Y (layoffs).

d. Next Quarter Guidance & Valuation

- Missed revenue estimates by 0.8%.

- Met GAAP GPM estimates of 26.4%. This implies the smallest Q4 to Q1 GPM decline in years, which is related to the core business and not any one-time benefits.

- Beat EBIT estimate by 124%. Commentary on the call hinted at EBIT outperformance continuing through 2024.

- It also guided to 618 million MAUs (+16 million Q/Q) and 239 premium subscribers (+3 million Q/Q).

For 2024, leadership also told us that revenue growth would accelerate vs. 2023 while user growth remains roughly consistent with 2023. Both items were as anticipated. Margins are expected to expand throughout 2024 as well.

Spotify trades for 50x expected 2024 EBIT and 58x expected 2024 FCF. EBIT is set to grow by 283% Y/Y while FCF is set to grow by 98% Y/Y.

e. Call & Letter Highlights

Advertising, The Spotify Audience Network (SPAN) & Spotify Wrapped:

SPAN is a conduit between ad buyers and content publishers across most podcasting apps. It allows creators to juice traffic and advertising revenue while giving advertisers greater control over advertising segmentation, targeting and impression selection. Ad placement is done programmatically with the dynamic ability to bid on ads on a by-episode, by-impression basis. This quarter, SPAN expanded from 9 to 14 countries, with entrances into India, Japan and Mexico among others. It also enjoyed double-digit sequential growth in participating publishers on the supply side and advertisers on the demand side. Steady growth for both cohorts is vital for maintaining a healthy marketplace with fair pricing and strong returns.

Interestingly, it’s re-thinking exclusive podcast deals as a driver of advertising revenue. The deals have helped drive premium subscriptions, but not advertising revenue. Non-exclusive publishing and SPAN will be two focus areas going forward to try to reaccelerate podcast advertising performance.

Spotify Wrapped, its annual end-of-year campaign, enjoyed 40% Y/Y engagement growth, with 225 million MAUs interacting with it.

Music advertising revenue rose over 10% Y/Y thanks, in part, to stable pricing. That’s wonderful to hear and meshes very well with other digital advertising players like Meta. Podcasting advertising revenue rose over 10% Y/Y as well. This, conversely, was driven by strong impression growth, with the pricing backdrop still somewhat “soft.” Overall advertising demand was called “choppy.”

Margins:

Gross margin tailwinds for the quarter included better podcasting and music profits as well as price hikes. Podcasting gross margin is now nearing breakeven through more partnership scrutiny and continued engagement growth. Gross margin headwinds for the quarter included audiobook start-up costs and a small severance charge in the cost of revenue bucket.

Operating expenses rose 2% Y/Y via severance charges. Without these charges, OpEx would have fallen by 11% Y/Y. Still, OpEx was lower than expected due to “lower marketing spend and personnel costs.”

Audiobooks & Other New Bets:

Spotify added 200,000 audiobook titles to its U.S. content library for premium subscribers in November. It’s already the #2 audiobook publisher and is already accelerating industry-wide revenue growth on its own. It’s very pleased with the start and excited about data pointing to many of these audiobook listeners being brand new to the sector. It’s expanding the pie. This is still a gross margin and overall margin drag for the company as it scales this business to broaden engagement and improve retention.

To continue juicing engagement, Shopify also debuted its very first merchandise tab on the app with personalized recommendations for purchases.