In case you missed it – my review of the Fed statement and Powell presser can be found here.

Table of Contents

- 1. Alphabet (GOOGL) – M&A Déjà Vu

- 2. Nvidia (NVDA) – CEO Jensen Huang’s GTC Keynote

- 3. The Trade Desk (TTD) – Some Thoughts

- 4. Nike (NKE) – Earnings Review

- 5. Micron (MU) – Earnings Snapshot with a Bit More …

- 6. PayPal (PYPL) – EVP and GM of Large Enterprise …

- 7. Mercado Libre (MELI) & Nu (NU) – Latin America

- 8. Market Headlines

- 9. Macro

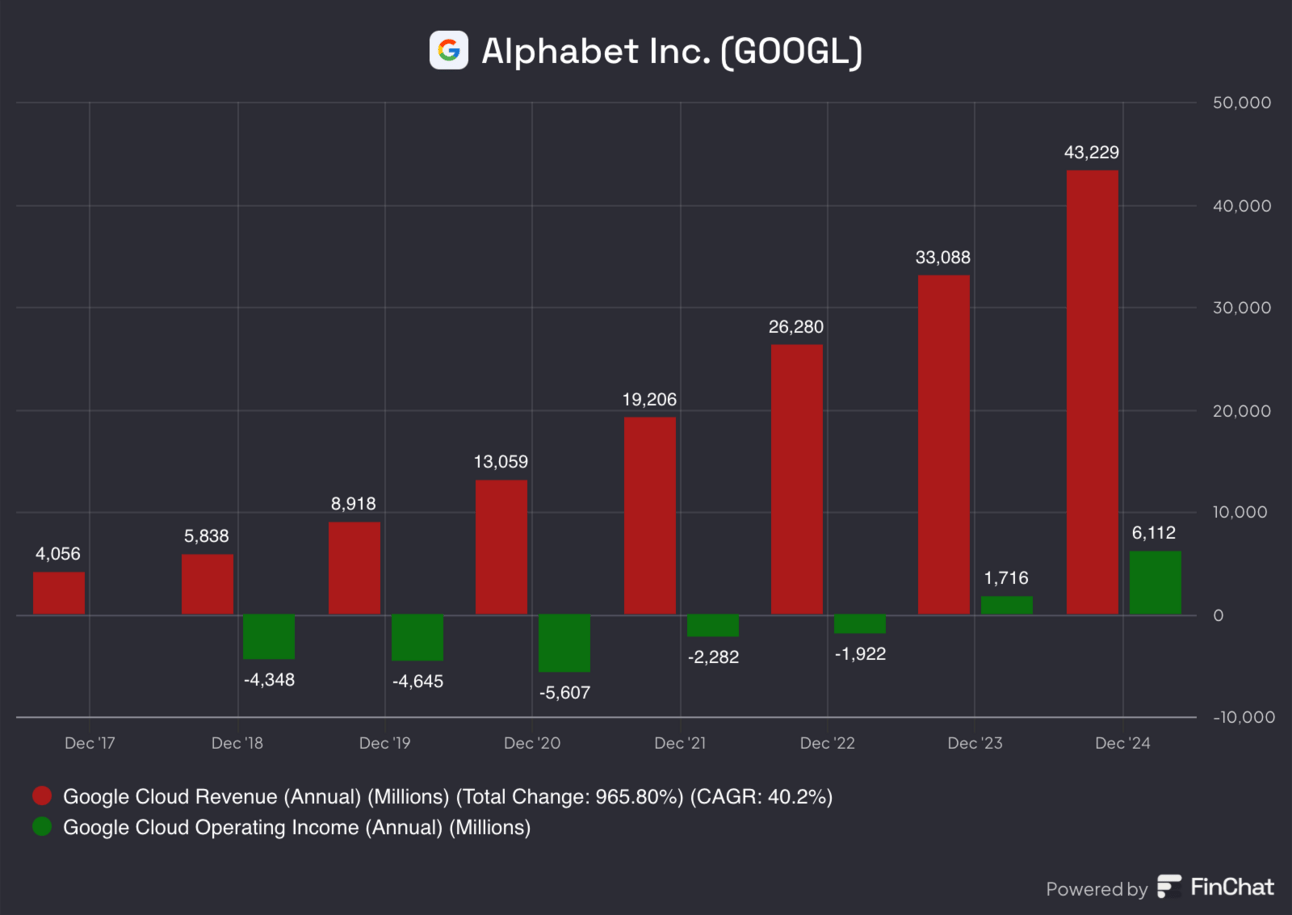

1. Alphabet (GOOGL) – M&A Déjà Vu

Wiz:

Google is reportedly set to purchase a large, privately owned, cloud security vendor called Wiz for $32 billion. Wiz offers a cloud native application protection platform (CNAPP) ranging from cloud configuration, to hygiene and also runtime security with its Wiz Sensor product. It builds graphic visuals of all cloud assets and interactions to provide a birds-eye-view of operations, flag threats/vulnerabilities and rank severity of each risk to prioritize work. It’s very similar to how we’d hear Zscaler or CrowdStrike explain their cloud offering.

While configuration and hygiene are table-stakes offerings for pretty much every cloud security vendor, its runtime security is considered high-quality and more differentiated. Wiz is also natively multi-cloud, and is expected to be tucked right into Google Cloud Platform’s (GCP’s) infrastructure and bolster its already world-class security, utility and cross-selling engine. It’s widely expected that Wiz will continue to operate as a seamless, omni-cloud platform rather than GCP attempting to create vendor lock. That’s not surprising considering how well entrenched Wiz already is and how popular it is for cloud security operations to be multi-cloud – especially in the new age of GenAI.

Price Tag:

Wiz generated about $500M in annual recurring revenue (ARR) in 2024. It has goals to reach $1B this year, although many view that as ambitious. I cannot stand sales multiples, but I’m going to use them here because Wiz is private and data is extremely limited. This is what we have access to: Assuming it reaches $800M, the mega cap is paying 40x forward ARR for this company. That’s similar to the multiple it offered to buy Wiz last year and is extremely lofty, but not egregious in my mind. I think this is the wildly rare case where 40x ARR actually does make some sense. Why? First and foremost, Wiz is a private market darling in the world of cloud security. And cloud security is the highest growth, most untapped area in a group of product categories that all boast long runways. It’s the shiniest house in a neighborhood of mansions. That’s why a disappointing 2025 would yield 60% ARR growth at scale, while every other high-growth peer in public markets struggles to deliver 25%-30% revenue growth this year. While CrowdStrike and Palo Alto enjoy more scale, at $800M in ARR, the scale difference is not nearly enough to explain this premium growth. And for more exciting context, Wiz was created in 2020 and reached $1M in ARR just 4 years ago. Insane progress in just a few years. This is a hyper-grower at scale that calls 50% of the Fortune 100 its customers.

Furthermore, The Search Giant is going to operate this in a hyper-efficient manner. Wiz will shed hefty cloud hosting costs, go-to-market and brand-building expenses, back-end maintenance needs and all other redundant costs as part of integration. While Wiz probably doesn’t have the margins of a CrowdStrike or Zscaler, the margin ceiling for Wiz under this mega-cap is higher than any pure-play cyber name on their own. There are a plethora of required input costs to nurture and grow a security business that Wiz will no longer incur. Similarly to Broadcom operating VMWare at sky-high margins, I think Google will do that with Wiz too. I do not think a 50% EBIT margin post integration is unreasonable to expect for this specific segment… I don’t even think that’s the ceiling. And considering this, Sundar Pichai probably sees 40x ARR as somewhere around 80x EBIT for one of the most enticing businesses in this equally enticing sector. It’s a lot more reasonable price tag with this in mind.

This deal faces considerable regulatory hurdles and skepticism. There’s a decent chance it’s not allowed. Still, the cloud-agnostic niche should help the company’s case, while its distant 3rd place in public cloud market share should too. If it closes, that will happen next year and could prop up overall growth rates by a low single-digit percentage. I’m also a bit encouraged to see Alphabet attempt this amid Department of Justice (DOJ) investigations. Maybe they’re seeing a more laxed regulatory backdrop and the M&A spigot is turning back on?

Public Peers:

I also think this is good news for all of Wiz’s competition – Cloudflare, Zscaler, SentinelOne, Palo Alto, CrowdStrike, Fortinet etc. Those companies trade at ARR multiples (again using my least favorite valuation metric because Wiz is private) ranging from 6x-18x. All of them, besides maybe SentinelOne, likely have much better margins than Wiz does today. Seeing Alphabet value a quality firm in the space at levels higher than what the public darlings enjoy should be supportive for their own valuations.

Finally, Wiz is an innovation machine and an intimidating disruptor. It is taking its fair share of large logos and storming onto the security scene. When large established companies buy security disruptors, the cliché is for those disruptors to move more slowly and become easier to beat. Just like when Carbon Black was bought by VMWare. I think every single company mentioned would be glad to see this purchased. It’s not that I believe Alphabet will botch this integration (far from it). I just think Wiz being part of a massive organization will inherently slow it down just a tad. More red tape… more bureaucracy.