Welcome to the 509 new readers who have joined us in the last week. We’re thrilled to have each & every one of you and determined to provide as much free value as we can.

1. Duolingo (DUOL) – Q3 2022 Earnings Review

a) Demand

- Beat its internal bookings guide by 7.5%.

- This is a telling forward looking indicator for growth.

- Beat its revenue guide by 1.7% & estimates by 1.8%

More Context on Demand:

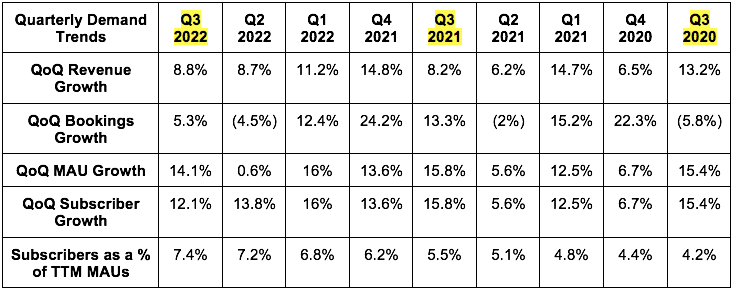

- 7 million sequential MAU adds is Duolingo’s best gross add number to date. And the best part? It was predominantly powered by word-of-mouth growth just like it always has been. Not more external marketing spend.

- Conversion rate of this larger cohort of new users to paid subscribers is similar to previous cohorts.

- As the vast majority of Duolingo’s revenue is via subscriptions, subscribers as a % of trailing 12-month (TTM) MAUs is the key metric to track.

- Duolingo’s 45.7% 2-year revenue CAGR compares to 46.6% last Q and 70% 2 Qs ago.

- This was the 5th straight quarter of accelerating user growth.

- Daily Active Users (DAUs) as a % MAUs rose from 24% to 26% YoY as users became more engaged.

- Advertising demand is weak for Duolingo just like for other companies. Luckily, it represents just 11% of its total revenue and still grew 18% YoY.

- During the call, CEO Luis von Ahn reiterated that the subscription business (75%+ of sales) has seen ZERO macro-related weakness to date.

- FX neutral bookings growth was 50% YoY. That is the demand line that is hit the hardest by dollar strength as it counts annual subscriptions (90%+ of its total subscriptions) as 12 months of business vs. 1 month for revenue. So there’s 12 months of the current FX impact included vs. 1 for revenue.

- Every 1% rise in the U.S. Dollar vs. major foreign currencies means $500,000 less in bookings. The sharp fall in the U.S. Dollar this week following the cool CPI report is wonderful news for this company and countless others (like Match Group, Meta, PayPal etc. – woot woot!).

b) Profitability

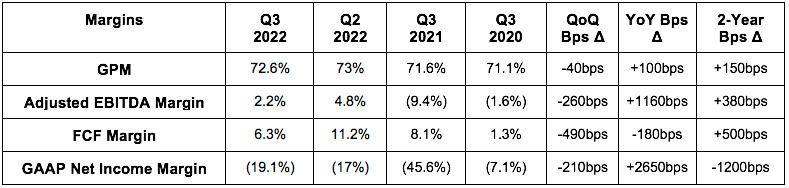

- Beat its ($3M) EBITDA guide & analyst estimates by 170% or $5.1M.

- Beat analyst GAAP net income per share estimates of ($0.55) by $0.09 or 16%.

More Context on Margins:

- Duolingo is intentionally trying to operate at break-even while investing all excess profits back into more growth. The positive EBITDA is in spite of that philosophy.

- Duolingo continues to enjoy brisk sales & marketing (S&M) leverage DESPITE the demand outperformance. GAAP S&M was 18% of revenue vs. 24% YoY.

“We’re going to continue to grow revenue faster than expenses.” – CFO Matthew Skaruppa

c) Balance Sheet

Duolingo has $600 million in cash & equivalents (about $12 per share) and no debt.

Its diluted share count grew by 0.4% sequentially and the company expects 3% total equity dilution for 2022. That’s quite modest compared to other recent IPOs. For now, stock compensation is elevated at 22% of sales (vs. 32% YoY) as IPO-related awards continue. This is why there’s such a large difference between GAAP and non-GAAP margin. Still, it’s slowing mightily as compensation grew by just 2% YoY as compared to the 51% revenue growth.

d) 2022 Guidance Updates

The Q4 2022 guide was in-line on revenue and ahead of expectations on EBITDA. Ideally, I would have loved to see a larger revenue raise after the beat this quarter, but I’m being very picky (especially in this environment) and the company has developed a clear trend of under-promise, over-deliver as well.

“We will provide our full year 2023 guidance on the Q4 earnings call. I’d like to remind everyone that we believe we are early in our monetization efforts and growth. We will continue to invest to drive growth and invest in more early stage efforts. Even as we do that, we will stay focused on progressing to our long term profit target of 30-35% EBITDA margins.” – CFO Matthew Skaruppa

e) Notes from the Call and Shareholder Letter

In-App Purchases:

Duolingo is making more progress with monetizing unpaid users via a la carte purchases within its apps. This has been powered by “gem” buying which is its virtual currency that can be used to speed through lessons more rapidly or access more gamified content. Specifically, in-app purchases now represent 5% of bookings vs. 3% YoY. It’s focusing more and more on motivating these types of purchases — especially in developing markets where subscriptions tend to be less appealing.

HBO Partnership:

“This partnership has been our most successful PR campaign to date, generating hundreds of press mentions and millions of social views. We attracted hundreds of thousands of new users to the High Valyrian course and nearly half of these will stick around to learn another language with Duolingo. In total we spent under $150,000 on this entire campaign.” – Co-Founder/CEO Luis von Ahn

This rough outline of how the partnership is going implies a worst case customer acquisition cost of $1.50. For reference, Duolingo collects around $7 in revenue annually per user (including free users) meaning it takes them about 60 days to recover all of these costs. That’ll work.

On Other Products:

- Duolingo English test reached adoption of 3,800 Universities (all of the top 25 by volume) vs. 3,700 QoQ.

- The Duolingo Math App is Live on the App Store:

- 2 weeks in, usage and retention is “as expected or better.”

- Interestingly, there are more adults using the product for brain training than children.

- CEO Luis von Ahn is confident that Duolingo can “monetize the app similarly to language learning.”

- As a reminder, Duolingo waits a few years to begin monetizing brand new products. Math will not be a big revenue contributor for a while.

- 50% of the users so far are also language learning users.

- Cross promotion is expected to become a bigger and bigger part of user growth as Duolingo leverages its vast built in user base to support new product launches.

“We’re probably going to be releasing other apps.” – Co-Founder/CEO Luis von Ahn

Discipline, Discipline, Discipline:

“While our headcount continues to grow, we have never gone nuts on hiring. Because of that, we don’t have to implement cost controls like layoffs or hiring freezes to be profitable.” – Co-Founder/CEO Luis von Ahn

f) My Take

This was a solid quarter in every sense. The company continues to demonstrate clear operating leverage while demand growth remains robust. And that’s expected to continue. Its creativity in seeking out efficient customer acquisition via social media or House of the Dragons is admirable to me and its user growth acceleration is wildly encouraging. Some are picking at the beat being smaller than we’re used to. If only that were the largest negative for all reports that I cover. I’m pleased and added to my stake following the price decline.

Based on Friday’s closing, Duolingo trades around 60X what I think it will do in 2023 EBITDA and under ~6X gross profit (which is actually a 25%+ discount to markets today). With all of the margin expansion and consistent growth expected to come, I see this as reasonably expensive.

2. Lemonade (LMND) – Q3 2022 Earnings Review

a) Demand

- Beat its revenue guide by 15.6% & analyst estimates by 14.2%.

- This was aided by its ceded premium rate falling from 75% to 55% YoY. Ceded premiums can’t be recognized as revenue. The ceded premium rate is expected to keep falling over time as Lemonade’s book scales & matures.

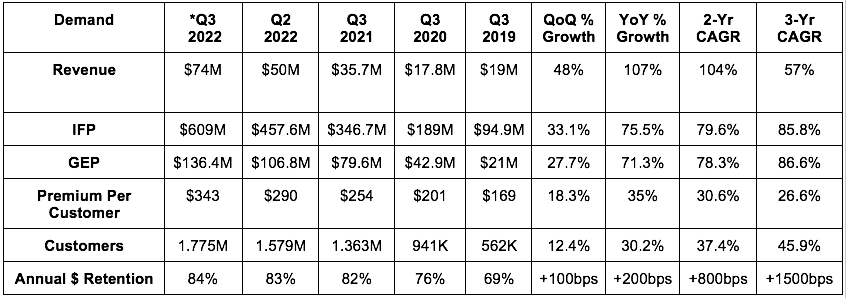

- Beat its In Force Premium (IFP) guide by 2%.

- Beat its Gross Earned Premium (GEP) guide by 6.6%.

More Context on Demand:

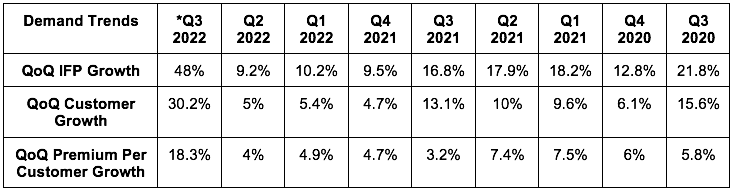

- *All growth metrics were propped up by the more than $100 million in premiums that Lemonade added from closing the Metromile acquisition this quarter. For more context, IFP growth would have been roughly 45% YoY without this help.

- Lemonade is intentionally pulling back on growth spend to ensure it can become profitable before requiring another capital raise. It does not want to have to raise cash from a point of weakness – and I appreciate that. It expects YoY growth to slow to around 23% YoY while it intentionally holds back on customer acquisition spend. It really is in control of its revenue and feels it can economically accelerate growth as soon as conditions improve.

- Lifetime Value to Customer Acquisition Cost (LTV/CAC) ratio “continued to improve” per CFO Tim Bixby. As of the last update we got here it was pushing 3.0X.

“Given our penchant and track record for rapid growth, we thought it sensible to underline our deliberate, tactical slowdown. We’re chomping at the bit, but we’re comforted in the knowledge that the huge growth opportunity before us isn’t going anywhere… still insurance is a business that thrives at scale, and so ever as we optimize for cash vs. growth, we will continue to see growth.” – CEO Daniel Schreiber

b) Profitability

- Lemonade beat its EBITDA loss guide by 9.4% & estimates by 6.3%.

- Lemonade met analyst net income per share estimates of ($1.25)

More Context on Margins:

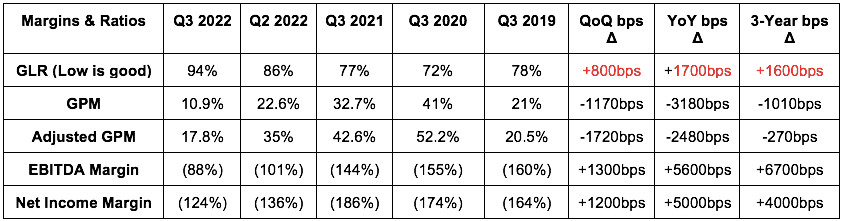

- The Metromile acquisition closing added roughly 400bps to Lemonade’s Gross Loss Ratio (GLR). The other source of the worsening is Lemonade’s rate update filings still working their way through approvals. As a reminder, rising inflation immediately impacts claim values, but not premiums paid. This inherently raises loss ratios – especially when your book is still as small as Lemonade’s is.

- It has filed the needed rate changes and expects that help to begin taking effect next quarter. It expects the faster pace of its filings to now keep up with rates of inflation going forward.

- In my view, this was an operational blunder from the team. It was too slow here compared to its competition. Only 25% of its business has been adjusted for inflation to date. Too slow.

- It expects GLR to continue its long run trend lower for each product with the occasional spike like we’ve seen.

- The GLR hit directly translates to a GPM hit as well. This manifested in a $53 million loss and loss adjustment expense charge vs. just $17 million YoY. Had the expense simply grown in line with revenue (which is still a very pessimistic long term assumption), GPM would have been 35.7% this quarter.

- Operating expenses grew 63% YoY – significantly below revenue growth. That trend is expected to continue.

c) Balance Sheet

- Lemonade still has $1.1 billion in cash & equivalents (about $16 per share in cash for the $23 stock) thanks to the $165 million in cash it added from closing the all-equity Metromile deal. This total is stable sequentially.

- There’s no debt.

- And again, the company reiterated its promise to turn GAAP profitable before it issues another capital raise.

- Share count grew nearly 9% in the last 12 months with a chunk of that due to the all equity Metromile deal. Stock comp was 21% of revenue vs. 36% of revenue YoY.

“A more accelerated rate of growth would, we continue to believe, maximize the Net Present Value (NPV) of Lemonade. Nevertheless, given today’s high cost of capital, we are decelerating spend towards optimal cash burn velocity which we estimate is in the 20-25% annual revenue growth range.” – CEO Daniel Schreiber

d) Guidance

- Raised its 2022 IFP guide by 0.2%.

- Reiterated its GEP guide.

- Raised its revenue guide by 3.8% & beat estimates by 3.3%.

- Lowered its EBITDA guide by 1.7% but beat analyst estimates by 2.7%

- Raised its capital expenditure guide by 10% (from $10 million to $11 million).

- Reiterated its stock based compensation guide of $60 million.

Lemonade began enjoying outperforming marketing efficiency in the third quarter. So? It pulled forward some planned Q4 marketing expenses into Q3. That’s why the quarterly beat was material, but there’s not much of a 2022 guidance raise. The “beat” on the top line was mainly a matter of timing and so demand was largely in line with expectations. The EBITDA outperformance, however, was encouraging considering it coincided with that accelerated spend.