Table of Contents

- 1. SoFi (SOFI) – Capital Market Access

- 2. Duolingo (DUOL) – Duocon 2024 with More Thought …

- 3. Micron (MU) – Earnings Snapshot

- 4. Meta Platforms (META) – Meta Connect 2024

- 5. Visa (V) – Regulation?

- 6. Uber (UBER) – Interesting Sell-Side Note

- 7. Nu (NU) – Going Global

- 8. Lemonade (LMND) – Hurricane Impact

- 9. Market Headlines:

- 10. Macro

1. SoFi (SOFI) – Capital Market Access

My SoFi investment case is progressing nicely. I will have it for you before the start of next earnings season.

Access to capital market loan buyers matters a lot for SoFi. It’s how the company can continue to originate quality loans beyond its current regulatory capacity, without taking too much balance sheet risk in the process. It allows the company to accept new customers, delight them with acceptable loan terms, generate gain on sale premiums and collect that data for future cross-selling. It can do all of this without requiring them to get overly aggressive or irresponsible in terms of leverage. Simply put, capital market access is vital for SoFi’s flexibility and financial results.

Rate cuts directly help capital market demand. They make future expected cash flows from underlying loan pools worth more and also lower borrowing costs to make hurdle rates more attainable. This happens while SoFi (per the team) will get more aggressive on unsecured originations (thanks to cuts) while enjoying more demand for its secured origination and refinancing businesses. The effect is a positive feedback loop of tailwinds that allows companies like SoFi to get bolder in catering to more borrowers. It’s a perfect storm (in a good way). And again, that means more member growth and more opportunity for cross-selling.

- Please note that none of this will show up in its Q3 results. Cuts happened with one week remaining in the period. The earliest positive impact will come in the Q4 guide, but the largest positive impact probably won’t come until 2025 guidance is issued.

We’ve now gotten a double rate cut and have seen borrowing rates begin to fall. And? This week, a new SoFi personal loan securitization was filed on the SEC’s website. Ratings for this pool have not been released and we don’t yet know what the gain on sale margin metrics are for the assets. Still, considering SoFi’s large capital ratio cushion and its strong gain on sale margins through the worst of this cycle, it’s hard to believe it would accept unfavorable terms. If demand wasn’t there, it could easily and profitably just keep the loans on the balance sheet. I’m speculating a bit, but to me this is common sense.

What we do know is that the securitization is quite large, and so quite material for adding incremental origination capacity. Specifically, the securitization represents more than 14,600 loans, which is roughly 50% larger than its previous two deals. The floodgates appear to be reopening.

2. Duolingo (DUOL) – Duocon 2024 with More Thoughts

Core Business Updates, AI & Updated Investment Thoughts:

As part of Duocon 2024, Duolingo launched a few new AI tools. It added new “immersive adventures” or quests to its app with a boatload more content variations and a new GenAI video call tool as well. With the video product, learners can have real-time, detailed conversations with AI chat bots. These bots are programmed directly into the front-end Duolingo character Lily. This helps any learner feel confident in talking to a fluent counterparty, without feeling nervous about saying something silly.

Lily has memory and can fetch previous, relevant answers to enrich the conversation while tailoring speaking difficulty levels to learners. It doesn’t tell you that you’re wrong when you offer a confusing or incorrect answer. Instead, it asks you to rephrase or clarify something, like you’re actually talking to a person. In true Duolingo fashion, this quirky tool is backed by data science and AI algorithms. It strives to minimize the self-correction part of the brain that prevents us from taking chances and learning via trial and error.

Every time I’ve visited a Spanish-speaking country, I’ve wanted to speak more Spanish but I didn’t for fear of offending or embarrassing myself. For me personally, this sounds useful. Video calls and the new quests will be laced into the more expensive Duolingo Max tier, juicing long term pricing power, retention and engagement. These are the kind of launches that wake investors up to how positive GenAI should be for the firm and the launches that will allow its fabulous financial success to be properly rewarded. We saw that playing out this week as sell-siders lined up to praise the aspects of Duolingo’s business.

For the last several quarters, and especially since the OpenAI translation product launch, bears have been loud and steadfast in their belief that AI will kill this company. I believe they are wrong and I’ve said so many times. Duolingo uses GenAI to vastly accelerate and fuel its content delivery network. It partners closely with OpenAI to gain access to their latest models. And? It is for learning and entertainment, rather than cheating (sorry Chegg). A few months ago when this negative sentiment was peaking, I asked readers to contemplate the following:

- Does talking through a smartphone replace the desire for a spouse to intimately talk to their loved one?

- Does talking through a smartphone seem as appealing to a potential employer as an identical candidate who can actually speak the language?

- Does talking through a smartphone supplant the motivation for world travelers to fully immerse themselves in a new culture?

I think the answer to all three questions is a resounding “no.” Those are the common Duolingo use cases, and GenAI does nothing to replace them. In reality, GenAI supports Duolingo’s rapid and constant product improvements. Without it, this new video product and a newer Duolingo podcasting product would have never been created. It would have taken too much time, too many developers and too much energy to make pursuit rational. That’s no longer the case. Humans now act as the foundational building blocks of new content, with AI models taking that foundation and driving countless variations. This company, with its wildly impressive team and unmatched dataset, is poised to utilize this new technology to extend its lead over everyone else in the pack.

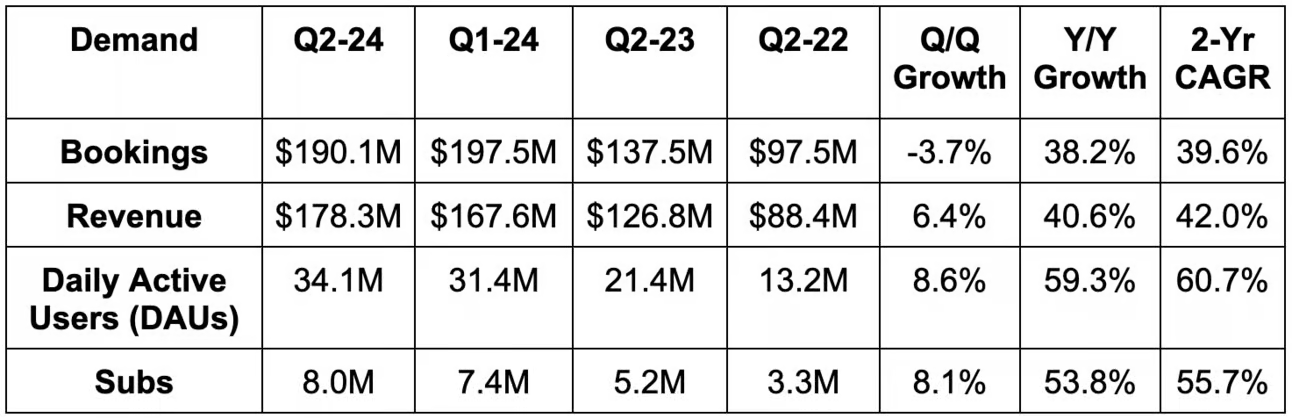

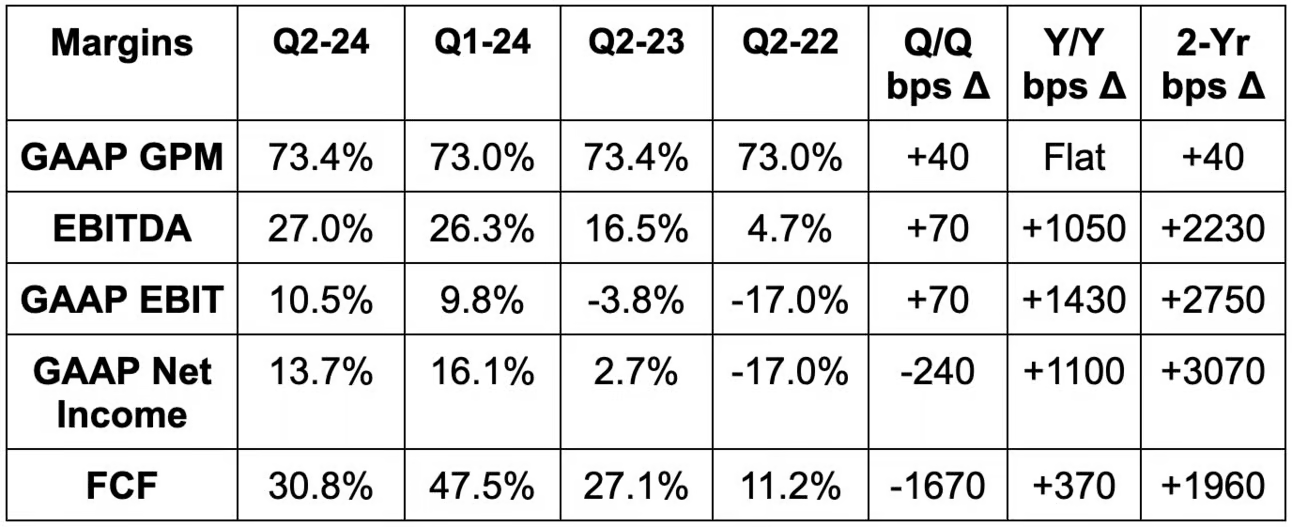

Quantitative Picture:

For evidence of its success, look no further than DUOL’s financial engine (tables below). It’s the unmatched ability to create great products through obsessive, data-driven split-testing to motivate viral, global, word-of-mouth growth that drives this. It doesn’t prioritize sales & marketing like its competition, but rather R&D. Great products are the best marketing engine a company can have. No company on the planet is currently delivering its combination of growth, leverage and GAAP profitability. Furthermore, no software company coming remotely close to its growth and margin profiles trades for as reasonable of a multiple DUOL. Here’s how the company stacks up against two of the highest quality software names on the planet:

- Duolingo 65x 2024 earnings; 54% 2-year EPS CAGR; 33% 2-year revenue CAGR; 1.20x PEG.

- Cloudflare 115x 2024 earnings; 32% 2-year EPS CAGR; 27% 2-year revenue CAGR; 4.25x PEG.

- Shopify 70x 2024 earnings; 36% 2-year EPS CAGR; 21% 2-year revenue CAGR; 1.95x PEG.

Also consider this: just one year ago, analysts expected $2.30 in 2024 EPS. The stock traded for $150 per share and a PE of roughly 65x. Fast forward to today, and explosive upward profit revisions mean the $275 stock stick trades for 62x $4.33 2024 earnings estimates. This stock’s success is not being driven at all by multiple expansion… just outperforming profit growth. That’s ideal. Duolingo has quickly turned into one of my largest winners and largest holdings, and the (relatively) modest PEG ratio makes it clear why I’m happy to keep it near the top of the portfolio. Plans on the holding were spelled out in a Stock Market Nerd Max article sent earlier this week.

Expanding Beyond the Core:

As part of the Duocon event, the company announced a new partnership with “Loog.” Together, the two will offer a portable piano for Duolingo Music. All of the firm’s financial success to date has been driven by language learning and the Duolingo English Test (English proficiency for universities and employers). Music, Math and all future subjects are future monetization opportunities. Early traction is great, but Duolingo always takes its time on monetizing any new product. It wants to make sure the offering is optimized and reasonably scaled before doing so. Just like Meta.

For the Math product, Duolingo is in content creation mode. It’s adding real life objects such as rulers, dollars and measuring glasses to connect problems to tangible scenarios. It also added 4 new games for brain training and learning and launched the app for Android in 6 languages.

For the Music product, it added a lot of modern songs with its new Sony Music partnership. It also added a more complex curriculum and ear training for listening skills too. Like for Math, this recently launched for Android.

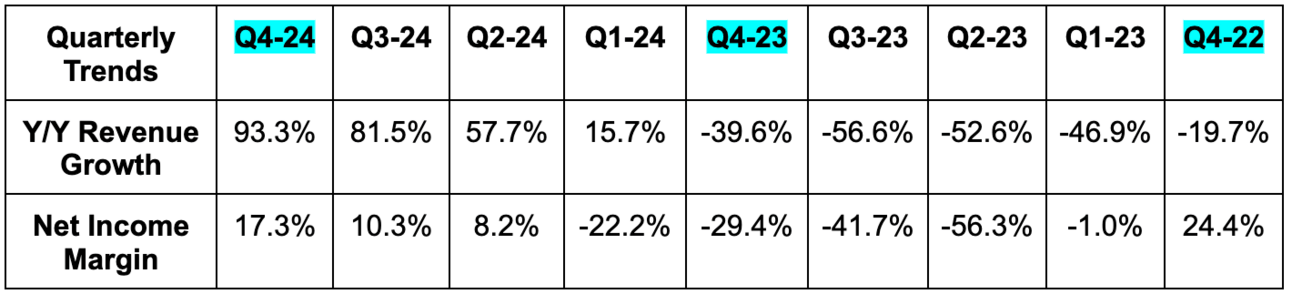

3. Micron (MU) – Earnings Snapshot

Results:

- Beat revenue guidance by 2.0% and beat estimates by 1.3%.

- Beat GAAP GPM guidance by 180 basis points (bps; 1 basis point = 0.01%).

- Beat EBIT estimates by 11%.

- Beat $1.06 EPS guidance by $0.12 and beat $1.12 EPS estimates by $0.06.

- Beat FCF estimates by 17.6%.

Next Quarter Guidance & Valuation:

- Revenue guidance beat estimates by 4.5%.

- Gross margin guidance beat 37.5% estimates by 200 bps.

- EBIT guidance beat estimates by 15%.

- $1.74 EPS guidance beat estimates by $0.21.

Micron trades for 12x forward earnings. EPS is expected to grow by 600% this year, 43% next year and -14% the year after. Very cyclical business.

Balance Sheet:

- $8.1B in cash & equivalents.

- $8.9B in inventory vs. $8.4B Y/Y.

- $1B in long term investments.

- $430M in current debt and $13B in long term debt.

- GAAP diluted share count grew by 2.7% Y/Y and diluted share count grew by 3.8% Y/Y.

- Dividends grew by 2% Y/Y.