Table of Contents

- 1. Snowflake (SNOW) – Investor Day

- 2. Starbucks (SBUX) – Investor Conference

- 3. Nvidia (NVDA) – Computex Jensen Huang Keynote & …

- 4. PayPal (PYPL) – Investor Conference

- 5. SentinelOne (S) – Investor Conference

- 6. Robinhood (HOOD) – Investor Conference

- 7. CrowdStrike (CRWD) – S&P 500 Bound

- 8. Disney (DIS) – Parks

- 9. Earnings Roundup – Gitlab (GTLB) and Samsara (I …

- 10. Market Headlines

- 11. Macro

1. Snowflake (SNOW) – Investor Day

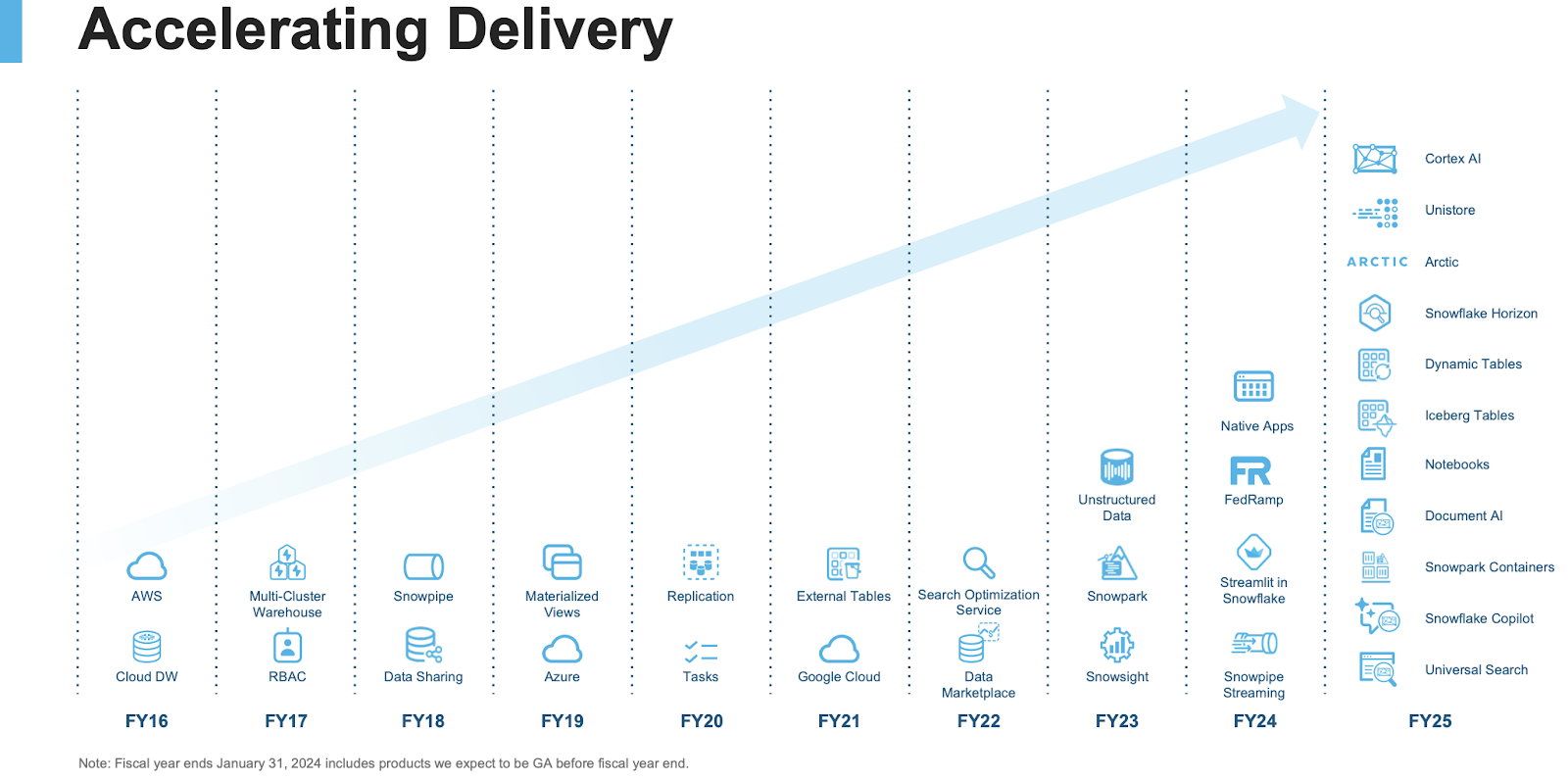

Snowflake conducted an investor day this week in which it discussed its opportunity, innovation and roadmap. There were no multi-year financial targets offered, but plenty of other insight to glean. CEO Sridhar Ramaswamy began the event with how Snowflake needs to (and is) getting better and where it goes from here. Ramaswamy again acknowledged how Snowflake fell behind in product velocity and more specific areas like GenAI. He’s pleased with the progress the team has made in revving up that, with rapid product debuts like its Arctic GenAI model serving as decent pieces of evidence.

What It’s Great At:

Snowflake has a fantastic data core. It can seamlessly ingest massive sums of structured and unstructured data from any public cloud and a near-endless roster of data integration partners. Its upcoming hybrid table product will also plug an important product gap by unlocking demand for transactional and analytical workloads. Snowflake has specialized in analytical workloads to date.

This means customers can tear down database silos and enjoy broader interoperability. That represents more data-rich context to guide analytics and app creation. With new support for Iceberg (open source) data tables, Snowflake is also making it easier for customers to onboard data into its environment for better algorithm seasoning and stickier usage. It also debuted its Polaris open source catalog to bolster support for Iceberg and open source data sharing. While this is a clear headwind for its storage business (10% of revenue) it could be a clear tailwind for consumption as clients enjoy access to more data and more opportunities to use it.

What it Needs to Get Better At:

Snowflake thinks it needs to improve with collaboration, data apps and AI innovation. Starting with collaboration, it is already delivering a significant network effect to its customers. 33% of customers have “stable edges” (or open data sharing with the Snow ecosystem) vs. 24% Y/Y. This not only creates a richer data ecosystem, but routinely helps it win customers from clients like Fiserv, which requires its vendors to use Snowflake sharing.

Its “Notebooks” product is another pillar for data collaboration. Databricks is considered to be well ahead of Snowflake here, but SNOW just released its competing product. Notebooks are collaborative and secure virtual environments for data science work. They allow for working on workflows remotely with colleagues in multiple source code languages.

Data apps are the second area of improvement. Candidly, I don’t see this as an area where Snow needs to improve. I see this as an area where their market needs to mature and evolve to a point of inspiring more usage. As with MongoDB (earnings review sent this week), consumption-based data and app-building models will be valuable, but aren’t highly needed right now. What is needed is the hardware foundation already laid out in the Nvidia section of this article. That is where the money is being made today. Not in apps stemming from this work… yet.

Snowflake is positioning its product suite to enjoy monetization when the sector is ready. Its native apps launch is a key focus area here. The product is fully sandboxed, which ensures the apps are separated from the core data engine. That ensures customers build apps and work in the environment without impermissible data access/sharing. That removes some anxiety and friction associated with unleashing data to somewhat unpredictable GenAI models. By combining complete data ingestion and analytics capabilities with app creation, Snowflake can “bring work to the data” for customers and cut transfer and storage costs in the process.

This is why Iceberg (open source) storage eroding demand for Snow’s competing storage service actually could turn out to be a net tailwind. Storage represents 10% of its business. The other 90% should enjoy higher consumption from giving customers easy access to more of their data on Snowflake’s platform. This should mean more app creation, more collaboration and more querying.

Within AI, Snowflake isn’t trying to compete with giant model builders like OpenAI and Meta. Instead, it is attempting to combine all of the disparate parts of GenAI to “deliver everything in a simple, tightly integrated way” and with full data access. It will offer full service, out-of-the-box GenAI app support with governance and maintenance handled by SNOW. It will use GenAI to help with data migrations, easier data engineering and chatbots to help with querying. It also wants to provide data scientists the ability to “talk to data” and lower skill set requirements tied to complex data analytics.

An important GenAI app for Snowflake is Cortex Analyst. This is a product extension of Cortex AI, which just added new chatbot functions and no-code tools/broad LLM access, reducing app-building and querying friction. Cortex AI is what Snowflake calls its “AI layer.” It’s a slew of GenAI-powered tools to (as Snowflake always says) bring AI, application-building and analytics right “to a customer’s data.” Cortex can summarize and derive meaning from seemingly unstructured text, help beginners write SQL, gauge human sentiment from jumbled data and help with sharpening pattern recognition to tighten forecasting. Cortex Analyst is the conversational tool that SNOW is using to realize its vision of helping analysts “talk to your data.” And with complete access to a client’s data to nurture these apps, Snow thinks its broader interoperability will help lower model hallucination rates (wrong answers) significantly. Great models still give incorrect answers 25% of the time. SNOW is determined to help lower this. Airbnb, Canva and Kraft-Heinz are early users of Snow native apps and its Cortex work.

“In areas like AI where we got a late start, we’ve shown the ability to accelerate time to be world-class.” – Snowflake CEO Sridhar Ramaswamy

“We are delivering innovation at a very different pace today.”

EVP of Product Christian Kleinerman

Go to Market Updates:

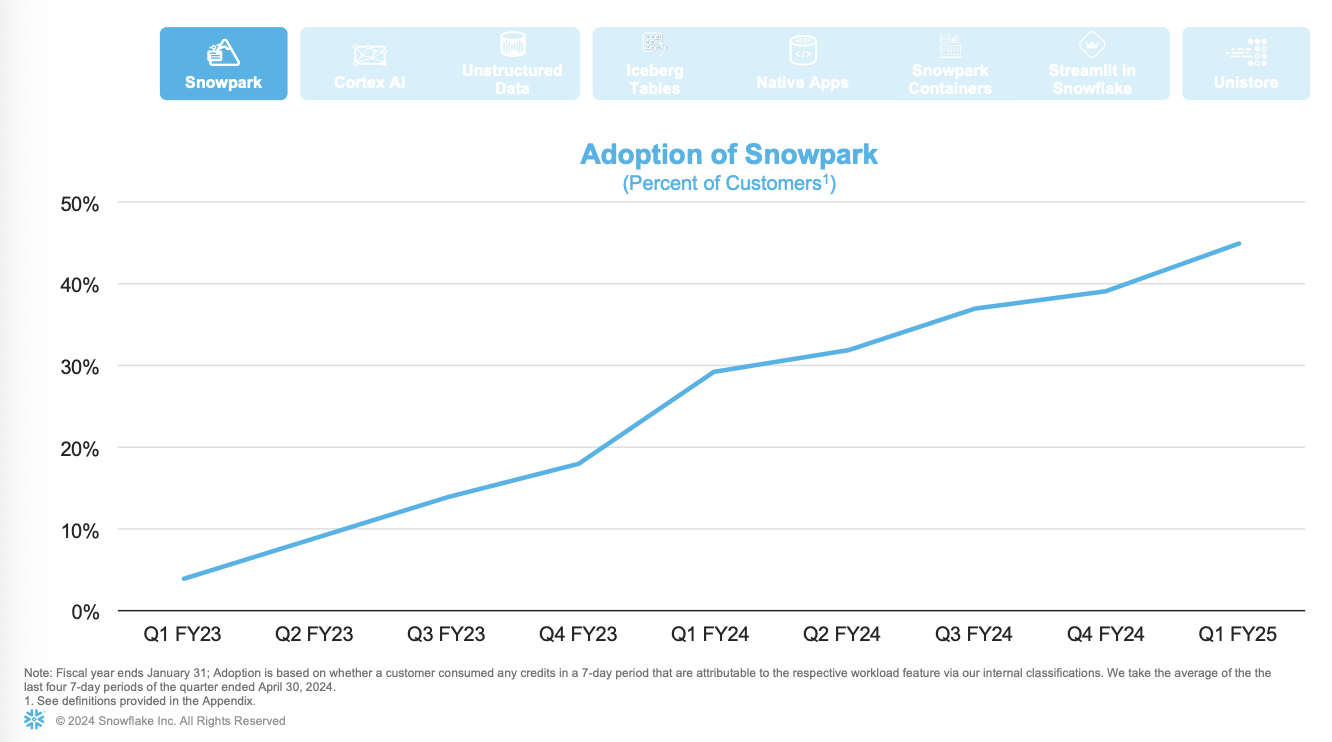

As you can see below, Snowpark adoption is going extremely well. This is its application-building platform that frees developers to work with data in any source code language. With it, developers can process and visualize data and build apps (through Snowpark Native Apps). Snowpark is their data-equipped playground to build new things. Notebooks and collaboration are understandably highly important in app work, creation and delivery. Snowflake’s former product void in this area was holding back this product’s potential.

This is the only new product included in FY 2025 guidance, but that will soon change. Cortex AI adoption strength is leading the team to think the product can meaningfully contribute to FY 2025 revenue. That should mean some modest upside vs. the current forecast.

From a go-to-market perspective, its shifted focus to rewarding workload consumption growth is working well so far. Still early here.

More interesting data points from the event:

- Its top 25 customers contribute $21.9 million in annual revenue vs. $18 million Y/Y and $12 million 2 years ago.

- Its Fortune 500 and Global 2000 customers contribute a small fraction of that $21.9 million. Plenty of runway left.

Partnerships:

Aside from the Polaris catalog launch, which includes partnerships with all 3 hyperscalers and more, Nvidia and Snowflake announced a new partnership as well. Snowflake is adopting Nvidia’s NIM framework to power AI applications from within Snowflake’s app. Everyone in the world wants to be using Nvidia’s software for their accelerated compute transformations. SNOW just made it easier for shared customers to do just that.

“Data is the essential raw material of the AI industrial revolution. Together, NVIDIA and Snowflake will help enterprises refine their proprietary business data and transform it into valuable generative AI.” – Nvidia Founder/CEO Jensen Huang

Some Thoughts:

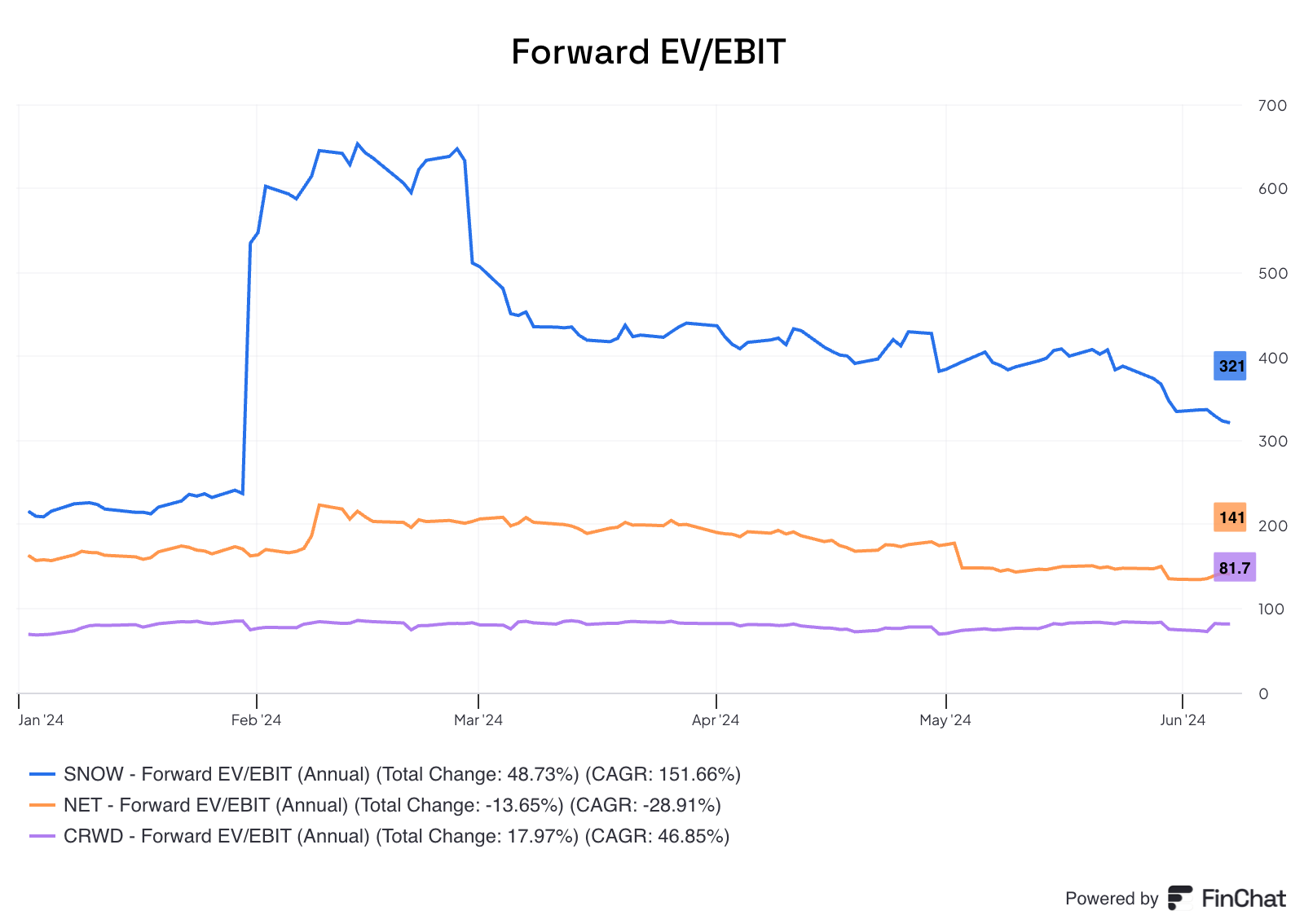

Snowflake’s investment case today is a bit weird. It’s investing heavily in GenAI infrastructure and innovation, which is weighing on margins. It likely over-earned last year while it under-spent on R&D, and we are seeing the catchup. So what does that mean? It means that you’re paying 150x EBITDA for a company showing negative EBITDA growth this year. That’s a lot more expensive than other best-in-class names like CrowdStrike and Cloudflare, which are both very pricey but are growing faster on the top line.

This doesn’t mean Snow is un-investable. It means investors must be confident in these investments bearing fruit and the profit engine exponentially brightening next year and beyond. Sell-side expects a 55% EBITDA CAGR in calendar 2025 and calendar 2026. I’d argue bulls need that to come in a lot better, considering that growth gets you to 66x EBITDA for calendar 2026.

Is this outperformance possible? Sure. Is it guaranteed? No. 2026 is a long way away. The Cortex AI contribution note is a solid positive hint… more positive hints are needed. I reject the notion that Databricks (fiercest competitor, but not yet public) will prevent Snow from succeeding. With the limited private market data we have, it does look like Databricks is ahead in innovation (especially notebooks), but this field is massive and Snowflake already has a sticky, client base. All it needs to do is give its clients all of the tools they’ve been requesting. That’s now happening at an accelerated pace.

This is a special company. Its share price sharply falling, to me, is more a function of it being relatively overpriced versus everything else. Its multiple demands perfection and does not forgive growing pains.

2. Starbucks (SBUX) – Investor Conference

What’s Currently Wrong with Starbucks?

The headline stemming from the last SBUX earnings report was a breathtakingly large cut to demand and margin guidance. That weakness is coming from a few places. Its occasional consumer in the USA is weakening, its business in the Middle East is showing macro fragility, and its recovery in China has been slower than expected with more pricing competition than it initially forecasted. This three-pronged concoction of headwinds led to it cutting 18% Y/Y EPS growth to nearly 0%. That is not normal for a company like this one.

And while macro is hurting this business a tad, there are reasons to believe that its improving execution can help it weather this storm. Starbucks is struggling with throughput and wait times. People are ordering their drinks and canceling baskets out of frustration with delays. This isn’t an issue of demand. It is an issue of letting people who want to spend money at Starbucks do so in a convenient fashion. Give the people what they want and when they want it. Caffeine and sugar are addictive… wait times are not.

The Recovery Plan & Signs of Progress:

Starbucks is pretty much at the mercy of Middle Eastern and Chinese macro cycles. It also can’t control irrational price wars in China, although those pricing wars seem to be diminishing, per CFO Rachel Ruggeri. What it can control is store efficiency, product offering and brand messaging.

Starting with store efficiency and throughput, its new CEO brought in high-level employees from Toyota to essentially morph Starbucks workflows into an assembly line. Its “Siren Craft System” perfects processes and optimizes machinery to drive this vision. In early test stores, it’s saving 10-20 seconds per order. By comparison, all of the throughput work for SBUX over the last few years has led to a 1 second boost to speed. This could be extremely impactful. There’s no required CapEx to bring this upgraded flow to life.

From a product perspective, it’s trying to tap into more of the Dutch Bros energy drink magic to augment its afternoon and evening demand. The new summer-berry refresher has done very well since the May launch. It has 0 calorie energy drinks coming later this year and plant-based offerings to better cater to younger customers.

Marketing precision and brand value communication are very important too. Starbucks believes it has done a poor job with communicating value to its customers. Its new rewards program, which launched last month, should help address this, along with targeted Monday promotions going forward. Most interestingly, it’s opening up its mobile app to non-loyalty program members for the month of July. This app is right up there with Chipotle in terms of its quality reputation. This will allow non-rewards members to tap into mobile ordering and expose them to the localized Starbucks promotional engine. It thinks this alone could drive $1 billion in incremental revenue for the next three years.

To me, this decision should be made permanent. It has 75 million weekly active users and 33 million loyalty program members. Give these 42 million incremental users more value. Mobile orderers and app users buy from SBUX with materially higher frequency. Why not give everyone access to the app and keep the rewards program exclusive to members? That’s what makes sense to me, and a strong July reception could easily lead to that happening. This is how it can drive personalized experiences to ALL of its consumers and convey real value to its occasional buyers (where it struggled the most in Q1).

Location Growth Notes & Efficiency:

There has been a lot of criticism levied towards the continued Starbucks store proliferation as some markets struggle. I don’t think that’s fair. Its cash on cash returns are fantastic in both China and the USA (40%) and it continues to see new openings as accretive and “incremental to the overall business.”

Finally, Starbucks is well on its way to realizing its $4 billion in cost savings over the next 4 years.

Some Thoughts:

There is no way around how ugly that Q1 showing was. But this is a world-class brand with significant expansion levers and a backdrop that shouldn’t be this bad forever. The tidbit on signs of rationalizing price competition in China is encouraging. I think this is a decent candidate for a turnaround and fixing its customer service should be the main driver.

3. Nvidia (NVDA) – Computex Jensen Huang Keynote & Some Thoughts

- GPU: Graphics Processing Unit. This is an electronic circuit to display screen images.

- CPU: Central Processing Unit. This is a different type of electronic circuit that carries out tasks/assignments and data processing from applications.

Intro:

Jensen Huang’s (NVIDIA Founder/CEO) Computex keynote drew the kind of crowd and excitement normally reserved for rock stars. Maybe it’s the leather jacket… or maybe it’s the historic financial run we’ve seen this company make over the last two years. Probably a combination. Here, I’ll dig into the details of the conversation and offer some views on the investment case.

Huang opened the chat with a bit of a history lesson. He brought us through IBM’s creation of the CPU/general computing 60 years ago and the subsequent personal computing and mobile computing revolutions. A third revolution is now unfolding as the world shifts from general compute (GP) to AI-enabled accelerated compute (AC).

Hardware:

Nvidia is powering this current infrastructure revolution with both world-class hardware and a suite of software tools to accelerate adoption. Let’s start with hardware. Nvidia’s latest superchip framework (combining specialized CPUs and its latest GPUs) is called Blackwell. Unsurprisingly, it delivers large performance and efficiency gains over its most recent architecture called Hopper. Nvidia is making sizable advancements every year, and is delivering this innovation with explosive boosts in performance. Nvidia routinely delivers 60x performance and 100x speed boosts just from clients switching from a GC-enabled framework to AC. These edges coincide with just a 50% rise in cost. Blackwell deepens those advantages even more.

This is why Nvidia is winning today. It drives massively more computer power with a small relative increase in hardware cost. In turn, this means more value and lower total cost of ownership.

And while Huang has trained us to expect these massive, frequent leaps forward, their impact still shouldn’t be taken for granted. In previous cycles, other legacy powerhouses like Intel operated on a 2-3 year cadence for delivering new chip platforms. We will get into why this is so vitally important in the investment case section of this post.

Blackwell includes two of its latest-and-greatest GPUs infused together by a 10 terabyte/second link. Nvidia’s clients need an ability to tie more of these GPUs together to boost capacity for their dense data processing and model building needs. That’s where its DGX supercomputer offering comes in handy. These combine 4 Blackwell chips with brand new switches to bolster connectivity. It’s called an NV Link Switch (5th gen) and can blaze a connection between several DGX systems to exponentially raise Blackwell superchip connectivity capacity.

But some clients need even more connected capacity than that. Enter the SpectrumX networking technology. SpectrumX is designed to support 10,000s of GPUs with two more generations planned to raise that to the millions. Nvidia is presently enabling more scaled and complex computing than anyone else.

Software:

Existing GP software infrastructure just doesn’t scale to handle the increasingly complex data processing requirements. Still, making that transition is easier said than done, so Nvidia has a suite of software products that make adoption and usage delightfully straightforward. Cuda is its software platform built to facilitate hardware adoption. It helps distribute work across the CPUs and GPUs within its hardware. CPUs still work fine for step-series, formulaic tasks with rigid instructions. This distribution optimizes performance and cost at the same time.

All apps and software that are switching to AC must essentially be rewritten. Nvidia provides the software tools to make new app creation easier. Cuda Deep Neural Network (CuDNN) is its library for industry-and-use-case-specific GenAI applications enabling sectors like telco to turn their GC networks into AC networks.

Unifying all of its software are Nvidia Inference Microservices (NIMs). This software includes Cuda and CuDNN and runs on top of AC data centers (or “AI factories”). NIMs are pre-trained models and software to “bring AI factories and apps to life.” All an end customer needs is Cuda, the compute capacity and then to download a NIM. From there, its desired, out-of-the-box AC, GenAI app is ready to use. Nvidia isn’t just leading in hardware innovation, it’s ensuring it has the software tools in place to optimize the pace of the new computing revolution.