Table of Contents

- 1. Okta (OKTA) — Earnings Review

- 2. Gitlab (GTLB) — Earnings Snapshot

- 3. Zscaler (ZS) — Earnings Review

- 4. Nvidia (NVDA) — Regulation & Thoughts

1. Okta (OKTA) — Earnings Review

a. Okta 101

Okta is a cloud-native identity broker. It is the grantor of access to a client’s apps and devices. It offers single-sign on (SSO), multi-factor authentication (MFA) and manages minimum permissions for global workforces and consumer bases (principle of least privilege).

Okta splits its business into three subcategories. Access management is by far its largest. Access management serves as a gatekeeper for which identities and credentials are allowed to enter a certain environment.

The other two are Okta Identity Governance (OIG) and privileged access management (PAM). Governance gives clients a birds-eye-view of identities and access across various apps to optimize hygiene and observe any potential vulnerabilities. This has been its most successful product cross-sell to date, as it is essentially an extension of the access management for corporate workforces. PAM is Okta’s zero trust approach to identity. It offers access only as needed, doesn’t offer consistent privileges to any devices, flags unfamiliar usage patterns and demands verification at every turn. Like Zscaler in network security, this prevents free, identity-based access to an entire software stack after penetrating the most vulnerable piece of it.

This isn’t an exhaustive list of its products. It also offers posture management to observe and analyze any misconfigurations and proactively flag issues. It prioritizes these issues by how pressing they are. This fully debuted during the quarter.

Still, the products already mentioned encompass all of the revenue drivers today. And for PAM, as well as all other new products in the works, it’s still in product market fit mode. It wants these all to be best-in-class before getting aggressive on selling. It isn’t there yet.

Within access management, Okta further splits its product buckets into workforce and customer management. Workforce is the access management broker for Okta’s clients; customer is its access management broker for the customers of Okta’s clients.

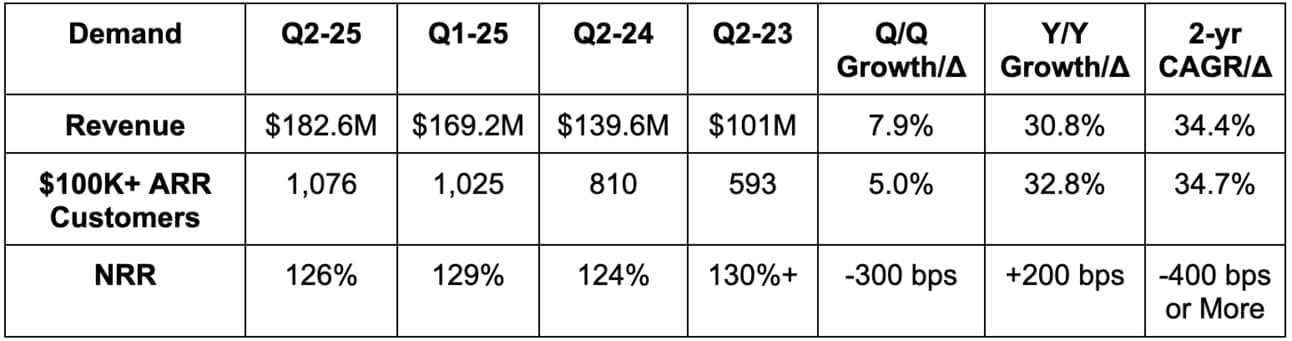

b. Demand

- Beat revenue estimate by 2.2% & beat guidance by 2.1%.

- Beat current remaining performance obligation (cRPO) guidance by 1.9%.

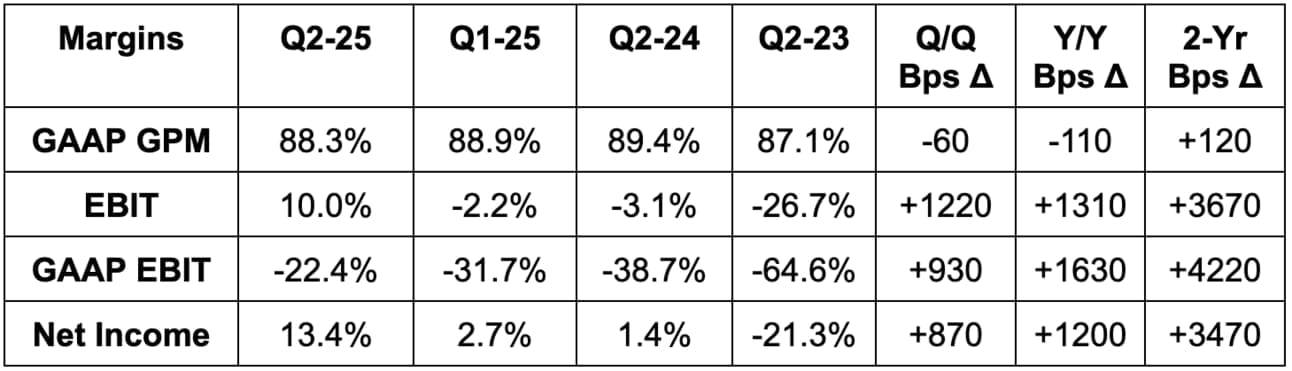

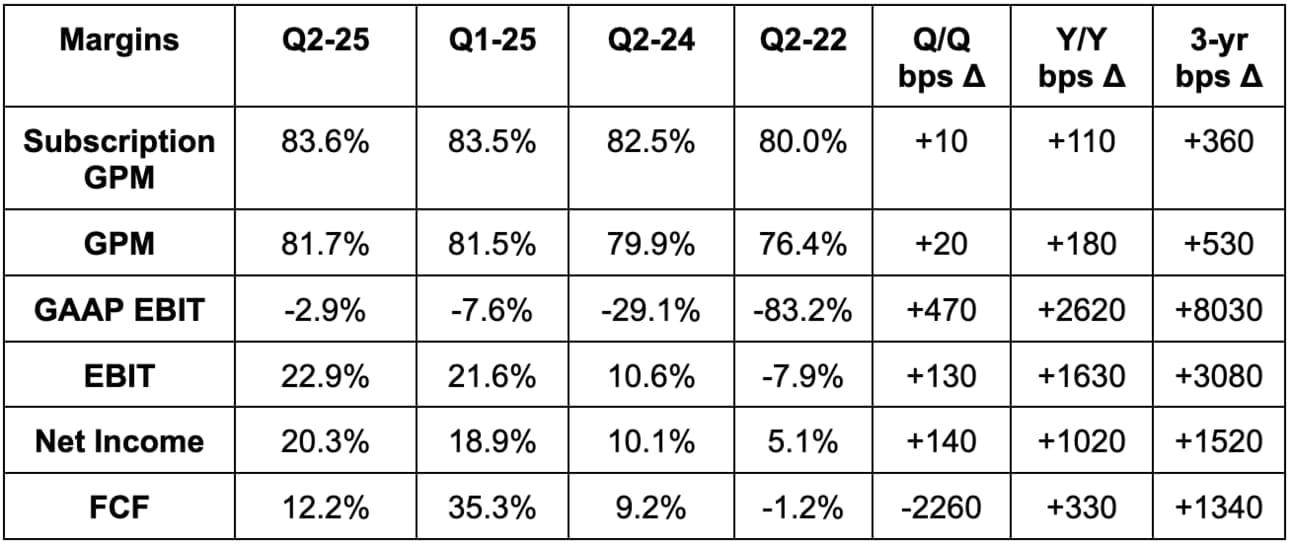

c. Profits & Margins

- Beat EBIT estimate by 18.4% & beat guidance by 19.3%.

- Beat $0.61 EPS estimate & identical guidance by $0.11 each.

- Beat $31 million FCF estimate by $47 million & beat guidance by about $46 million. FCF on a quarterly basis is highly influenced by timing of payments & receipts.

d. Balance Sheet

- $2.35B in cash & equivalents.

- No traditional debt; $1.11 billion in convertible senior notes.

- Diluted share count rose by 7.1% Y/Y (Auth0 M&A still) while basic share count rose by 4.2% Y/Y.

e. Guidance & Valuation

- Raised annual revenue guidance by 1.0%, which beat by 0.8%.

- Raised annual EBIT guidance by 9.1%, which beat by 8.0%.

- Raised annual $2.38 EPS guidance by $0.23, which beat by $0.19.

- Raised annual FCF guidance by 7.1%, which beat by 5.7%.

- Next quarter guidance was comfortably ahead across the board.

Okta trades for 30x forward earnings. Earnings are expected to grow by 64% Y/Y this year and by 11% Y/Y next year.

f. Call & Release

Platform Play & Trust:

Similar to Zscaler in network security or CrowdStrike in endpoint security, Okta wants to be the de-facto, end-to-end identity security platform. This vision manifests in its pursuit of “freeing everyone to safely use technology from anywhere.” Core access management tools are its bread and butter, but it also offers a plethora of customer and workforce identity use cases spanning, password-less management, OIG, PAM, posture management, threat protection etc.

OIG is the most developed cross-sell opportunity for Okta to date and the only non-access management product driving material traction and momentum. This product’s success is great evidence of Okta being able to extend relevant use cases, grow lifetime value, rev the cross-selling engine and become that identity platform. This quarter, OIG passed 1,000 total customers, is delivering tangible retention benefits and continues to gain considerable momentum. Good step in its “platformization” pursuit. For more evidence, contract length and size noticeably increased Y/Y across its customer base.

Larger contracts show you clients are looking to do more with Okta. That not only supports the platform vision but also offers investors another positive. Okta is only a year removed from its security blunder that jeopardized sensitive information. Not great for a security vendor. Clients looking to trust Okta with more of their security needs is a great sign that it’s somewhat seamlessly recovering from this ugly chapter in its history.

- 40%+ of the Global 2000 is now an Okta customer.

- Its fastest growing cohort of customers was within the $1 million+ ACV segment.

Macro & Guidance Methodology:

The macro backdrop did not get better or worse for Okta Q/Q. It remains challenging. Existing client up-selling is holding back usage assumptions on the customer side and total seats on the workforce side. That is hurting existing client growth. At the same time, new client wins are being slowed by continued budget scrutiny.

Guidance doesn’t anticipate any macro improvements next quarter. It also adds incremental conservatism from the unknown impact of last year’s security event. The firm saw no material, direct impact from that issue this quarter. Still, it thinks it’s likely that pipeline size and conversion are likely still being hurt to an unknown degree. To me, this sounds like gearing investors up for another quarter of under-promise and over-deliver.

Product Innovation:

Like every other enterprise software firm, Okta is looking to lace GenAI into its products to uplift utility and breadth of use cases. This quarter, it launched a new Identity Threat Protection Product with Okta AI (its suite of agents and chatbots to automate tasks). This product is trained on an Okta client’s own data and further seasoned by the data network effect Okta has built through years and years of scale. The product boasts constant, real-time threat detection (pre and post initial authorization), "amplifies signal sharing” and instructs remediation.

On the customer ID side, it introduced “Highly Regulated ID.” This caters to clients in industries with especially sensitive data (financial services and healthcare) with “elevated security, privacy and user experience controls.” This is for post log-in use cases.

It also added new bot detection tools for Customer ID. This has reduced credential stuffing (login stealing) by over 90% for some clients. This product ties closely to Okta’s Secure Identity Commitment. This is its initiative and response to the 2023 hack to ensure it doesn’t happen again. It’s about perfecting its architecture and plumbing and establishing needed redundancy. In turn, that is how Okta plans to re-secure client trust and budget. It thinks it has made “significant progress” under this initiative (including the upgraded bot detection tools), which it also thinks is leading to incremental pipeline generation too.

Reignite Growth:

One of Okta’s core operating objectives is to re-accelerate its growth. Reestablishing customer trust and its cross-selling push are two key ingredients… but there’s another to mention.

Okta has been rather slow to embrace channel partners. For others, these partners have not only supported growth engines, but have been the predominant drivers of them. Okta wants a piece of this opportunity and is finding some success in its pursuit of it. This quarter, 80% of its largest deals were procured by Global System Integrators (GSIs). 40% of its total revenue is now generated from partners and average deal size from these partners is 3x larger than direct wins. Good progress.

g. Take

This was a very good quarter. Okta continues to successfully move beyond its security blunders and rebuild client trust. That was not a given. OIG is becoming its first real cross-selling tool and there seems to be more following in its footsteps (PAM the most exciting in my view). The company is determined to reaccelerate growth while maintaining great operating leverage. If they can continue to pull that off, this valuation looks quite compelling. This is one of my favorite non-holding security names.

2. Gitlab (GTLB) — Earnings Snapshot

a. Results

- Beat revenue estimate by 3.0% & beat guidance by 3.4%.

- Beat $10.6 million EBIT estimate by $7.6 million (71%) and beat guidance by $7.7 million.

- Beat $0.10 EPS estimates & its identical guidance by $0.05 each (roughly 50% net income beat).

- Generated $0.08 in GAAP EPS vs. -$0.33 Y/Y. Good for them (truly).