In case you missed it, the majority of this week’s content was already sent:

- Mid-week news – Uber Confidence & Partnerships; Meta Content Moderation; Disney’s Fubo deal; DraftKings Developments; Lemonade California News.

- Portfolio & Performance vs. Benchmarks Update.

Table of Contents

- 1. My Investing Rules

- 2. Meta (META) – TikTok Ban & eBay

- 3. Disney (DIS) – Various News

- 4. CrowdStrike (CRWD) – Public Sector Win

- 5. Nvidia (NVDA) – Jensen Huang Consumer Electroni …

- 6. Headlines & Macro

1. My Investing Rules

As part of the ongoing, inter-earnings season investing concepts theme, I wanted to discuss some personal stock market rules that I have imposed on myself.

Options:

First and foremost, I do not speculate with naked options. I very sparingly use them as a hedging tool or what I call “disaster insurance” surrounding earnings reports, but that is rare. Why do I avoid this type of investing vehicle? We do not personally control the outcomes of these companies. We aren’t insiders with access to real-time information on how things are progressing. We rely on backward-looking earnings reports, and uncertain guidance to gauge a company’s health in increments of three months, with some disclosures sprinkled in here and there. This isn’t me saying public stocks are dangerous. I think the U.S. stock market is the most powerful and reliable wealth builder ever created. But I think pursuit of that wealth creation must be slow, calculated and responsible. Options are not that.

Being right about a stock’s direction is hard enough. Forcing ourselves to need to be right about that direction and the timing of it is something I do not find worth pursuing. It’s speculating on how exogenous factors that affect day-to-day stock prices and sentiment will play out. You will constantly see people post pictures of their options trades on social media and how they made several hundred percent in a day. We have to know that this sharing is immensely cherry-picked. These folks are not showing you the dozen other options trades that went to zero and they’re probably not showing you how their portfolios are performing either. Not a coincidence. There are successful options traders, but I find boring old equity to be far easier and less stressful

Margin:

Next, I never use margin. Debt is not for speculative assets where we don’t enjoy the benefit of asymmetric information. Debt is not for things that violently fluctuate in price. Debt is to be carefully and sparingly used to put roofs over our heads or to be able to drive to work. Unless carefully, obsessively monitored, margin is asking to blow up an account. It is inviting the magnification of losses (and gains) and accepting the risk of margin calls and required sales. It is begging to force ourselves into a corner and liquidate winning positions that we’d otherwise hold for the long term. And? It’s also expensive. I’d rather focus on fundamental research. Markets are stressful enough without worrying about margin calls and upside is more than compelling enough without it too. I find most options and margin approaches to resemble gambling more than investing.

Shorting:

Thirdly, I don’t short. My favorite part of public investing is the profit potential of each position. Upside is uncapped while downside is inherently finite. When you short, you are intentionally flipping that equation and willfully uncapping your potential downside. I see no reason to do that. If I think a company is ridiculously overvalued or toxic, I’ll just find a different investment case that I’d like to buy into. There are always plenty of opportunities out there on the safer long end and it’s just harder to make money going the other way. Expensive can get more expensive, crazy can get crazier, and “markets can stay irrational for longer than you can stay solvent.” A good reminder from King Buffett.

Maximum Allocation:

Over the last several years, I have toyed with the idea of “maximum investment allocation.” I do think diversification matters a lot, as, again, we do not have direct control over the outcomes of our companies and some failure is inevitable. Nobody comes close to batting 1.000, and putting all of our eggs in one basket means one measly ground out to third is the end of our portfolio.

As I’ve grown more experienced and confident in my ability to assess companies I’ve gradually raised the allocation ceiling. As of right now, 8% of total net worth is the current cap. This is based on capital outlay, rather than what the position is worth, as I’m more than happy to let winners like Amazon and SoFi grow larger on their own. There’s one large caveat here. The 8% is for profitable companies. The cap is just 4% with companies that have yet to inflect to profitability (just Lemonade in my portfolio). That lack of positive margins make firms more speculative and more volatile, considering they haven’t proven they can accomplish the only thing that matters for long term returns… profitable growth.

I am more flexible with this rule than the other three. While this hasn’t happened yet, I do think I’d entertain breaching that 8% clip if a world-class blue-chip like Amazon sharply sold-off for reasons I found unfair. I don’t think I’d do this for the vast majority of companies.

One Strike and You’re Out:

I’m patient with companies. One blunder is usually never enough to force me out. The most iconic firms in the world have all stubbed their toes on the way to becoming historically successful investments. With that said, there is a red flag that forces me out of positions immediately: Accounting fraud risk and general dishonesty. Because we are not insiders and because we don’t live in the day-to-day operations of a company, we rely on trustworthy leadership. This is to be earned and never unconditionally enjoyed. My assumption will be to trust teams as I believe in innocence until proven guilty. But? If there’s the slightest semblance of shadiness… If it becomes even a little likely that I cannot trust the words coming out of a team’s mouth… if I begin to question the moral integrity of those leaders… if accounting gimmicks surface… I am out. No questions asked. Done. The stock may go up and up and that’s fine, someone else can make that money. I can’t sleep while investing in companies with management I don’t trust.

Letting shady and charismatic leaders seduce us into thinking their words are gospel is a clear path to losses. I made that mistake in 2022, believing an Upstart leadership team that promised they wouldn’t use their balance sheet to hold more loans. They also claimed immunity from macro headwinds when no lender is ever immune. I knew better, yet I listened to them anyway, as I thought there was no way they’d be so publicly wrong. What was my lesson? Turning several hundred % gains into a position that slightly underperformed benchmarks through the holding period. I gave up significant alpha, which leads me to my final rule.

Relax:

Accept being a human. We all make mistakes. We are not perfect. These rules above are guidelines designed specifically with that idea in mind and crafted in the spirit of damage control when we do mess up. Our blunders are inevitable and it’s important to structure our approach in a way that makes this entirely ok. If you can’t endure a market downturn, you’ll never enjoy the gradual, long-term wealth compounding opportunities that markets provide. We need to ensure our next mistake and the one after that don’t lead to our financial ruin. And we need to make sure we aren't taking too much speculative risk or acting irresponsibly amid that objective.

As long as that’s the case, we can’t beat ourselves up for being wrong about a name. We can’t get internally angry the next time one of our opinions turns out to be wrong. This isn’t even a matter of “well I’m not Warren Buffett.” Buffett isn’t perfect either. He sold Snowflake at the bottom and has had other failed investments to his name. Just like me and just like you. That’s why we manage a portfolio of quality, diversified companies. And that’s why we must smile, contemplate, grow and move on with our heads held high next time we misstep. If you’re behaving responsibly and doing things the right way, all a mistake represents is an opportunity to learn. I’ll be learning until I die.

Conclusion:

This approach has served me quite well over the last few years. It’s how I can comfortably invest in disruptors and high-growth firms while also remaining calm and sleeping well at night. This is how I allow myself to participate in the generational growth stories and high-fliers without feeling anxious, irresponsible or overwhelmed. It’s how I safely take more risk without sacrificing compelling risk/reward. But? It’s just my approach. You develop the guidelines that work for you.

Everyone does things differently. There will never be a one-size-fits-all strategy for stock picking, as it’s a byproduct of our circumstances and personalities. I simply share this information to offer inspiration as you form your own approach, and I invite you to use or ignore whatever you want (as always).

2. Meta (META) – TikTok Ban & eBay

It is looking increasingly likely that TikTok will be shut down in the USA on January 19th. There are several interested bidders in the company, but it’s unclear if a deal will get done or if TikTok is even willing to sell to a U.S.-based buyer. We will have to see how this unfolds, especially considering the new administration seems to be against a ban.

If a ban goes through, that would clearly deliver a large engagement boost to Meta’s apps and everyone else competing for screen time. Still, there is a small risk with that outcome as well. Meta enjoys a lot of revenue from Chinese-based sellers, and China could easily retaliate by barring those sellers from accessing Meta’s apps. While possible, I don’t think that’s super likely. The Chinese government generally is eager to let its businesses sell to other countries and bring value and money into the country. It clamps down on restrictions when there are foreign companies selling to Chinese buyers and pulling value out of the nation. Meta isn’t even allowed to operate in China at this point and this form of retaliation would be China cutting off its nose to spite its face.

This is not the reason to own Meta. Its fortress ecosystem, AI leadership, world-class team, elite financials and unmatched network effects are the reasons to own this one like I do. Still, we will take tailwinds whenever we can get them and this would surely lead to a bump in its results.

In other Meta news, it will begin including eBay (EBAY) listings on its marketplace. This should improve assortment and monetization.

3. Disney (DIS) – Various News

a. Bullish Analysts

Disney got an upgrade to overweight by Redburn ($147 price target) based on optimism surrounding its streaming business. Like everyone else, it sees this turning into a real profit growth driver in the coming years, with the margin inflection now in the rear view mirror. It now thinks the streaming business is a larger tailwind than the linear business is a headwind. Maybe they read the newsletter. Wedbush thinks the Hulu Live TV + Fubo merger will “create a dominant player” to more effectively compete with the scale of SlingTV and YouTube.

b. Advertising Monthly Active Users (MAUs)

Disney disclosed a new metric this week. It has 157 million ad-supported MAUs across its streaming platform, with 112 million in the USA. This compares to 70 million for Netflix as of two months ago, but the methodology between the two companies is different. We don’t even know how Netflix calculates their own number. Disney counts a customer as an MAU if they have watched more than 10 seconds of ad-supported content over the last month. It multiplies this number by 2.6x, as that’s the average number of users per account.

There’s really nothing to compare this to and no consensus estimates to understand how this stacks up vs. expectations. There were no expectations considering this disclosure was a surprise. I’m hoping this inspires competitors to embrace a similar metric, so we have more of an apples-to-apples comparison across the budding field.

c. Venu

While the proposed Venu sports venture (Fox + Warner Bros. + Disney sports rights in a bundle) resolved legal battles with Fubo this week, the DirectTV Antitrust claims are not going away. Based on all recent developments, Venu is no longer happening. Disney was asked last quarter about this risk and didn’t think it would be material to results.

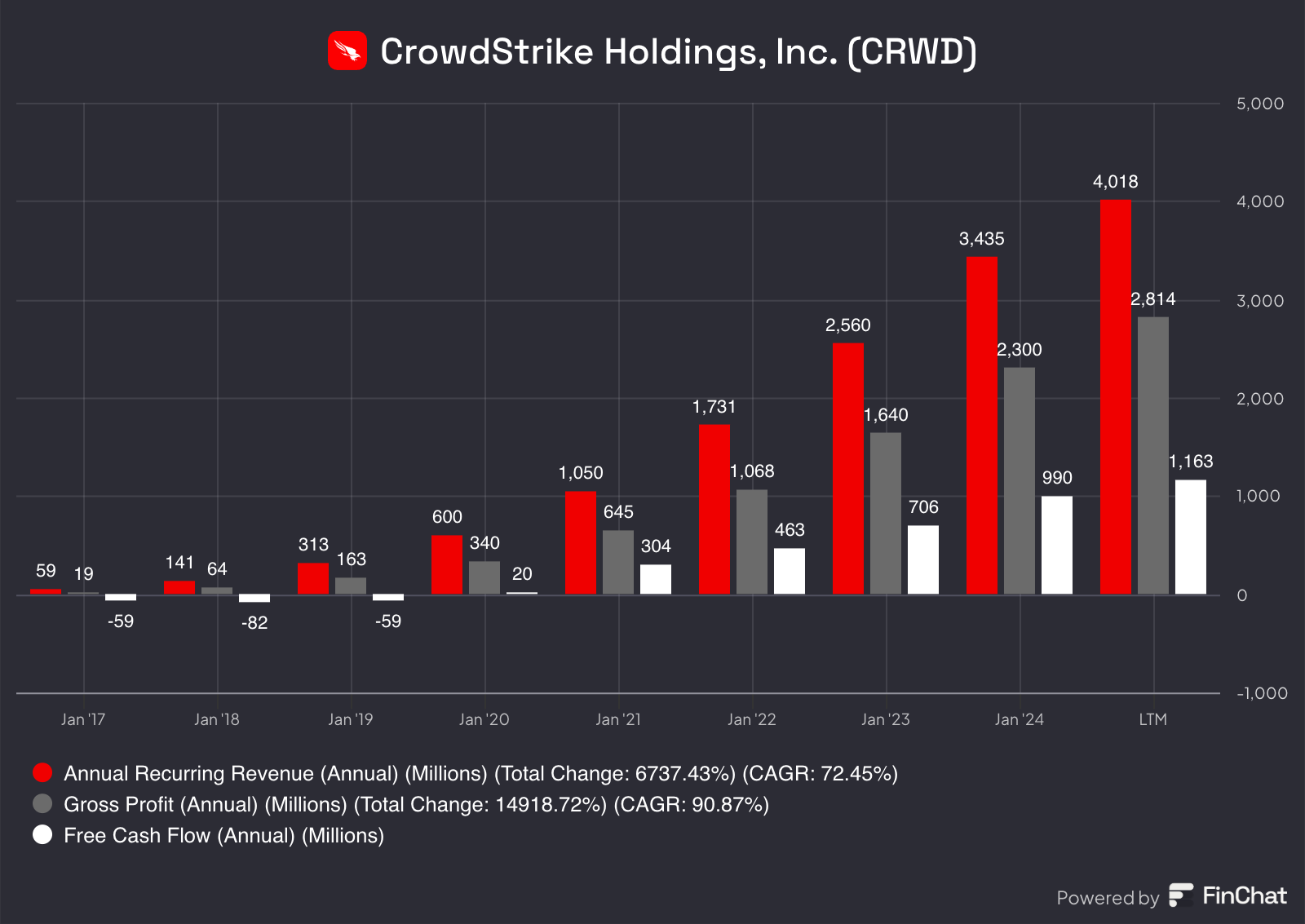

4. CrowdStrike (CRWD) – Public Sector Win

CrowdStrike received FedRAMP Moderate authorization for three additional modules this week: Next-Gen SIEM, Falcon for IT and Data Protection. Notably, this is not FedRAMP High authorization, which would allow it to cater to the most sensitive and secure agencies, but this is still quite meaningful. The 3 modules join FedRAMP authorization for several of its products across endpoint and cloud security. Why does this matter? FedRAMP Moderate clearance is required for various agencies to actually use and deploy software.

In a world obsessed with vendor consolidation and using overarching product platforms, this allows CrowdStrike to be a much more valuable partner for public sector clients. It will surely improve its ability to deliver more compelling product packages to these customers, and also offers more evidence of the company gracefully moving beyond the ugly July outage. Clearly they have not burned the trust of the Federal government.