Other Reviews to Read From This Season:

- Alphabet Earnings Review.

- Meta, Robinhood & Starbucks Reviews.

- Tesla Earnings Review.

- Amazon & Microsoft Earnings Reviews.

- PayPal Earnings Review.

- SoFi Earnings Review.

- Chipotle Earnings Review.

- ServiceNow Earnings Review.

- Netflix and Taiwan Semi Earnings Reviews.

- My portfolio & performance vs. the S&P 500 as of today.

Table of Contents

1. Palantir (PLTR) – Q1 2025 Earnings Review

a. Palantir 101

Palantir is a software company that helps customers get the most out of their structured and unstructured data. Like many others, it pulls from years of AI/ML work to automate insight-gleaning. It utilizes complex neural networks to power anomaly detection, trend forecasting and natural language processing. It works openly with many database vendors for scalable, interoperable storage and low-latency querying, and offers its own tools there too.

Overall, it frees clients to conjoin disparate data sources while utilizing its software to uncover ideas that manual analytics and legacy competition cannot derive. It gives customers a bird’s-eye view of their operations, with detailed suggestions to help optimize products and workflows. This happens in a zero-stakes-or-risk environment via a process called Ontology. Ontology enables clients to freely test digital twins to actually observe what works and what doesn’t. It’s like split-testing on steroids.

Revenue is neatly split into two buckets – “government” and “commercial.” Government clients predominantly use its Gotham product platform, while commercial clients mainly use its Foundry product platform. With Gotham, Palantir routinely builds custom use cases for individual government clients. Foundry was built to be more malleable, with far more pre-built app integrations and developer kits available. That diminishes the need to conduct custom builds for every single private enterprise. Still, it does materially more custom building than a typical B2B software firm will. That’s more expensive, but has also led to wonderfully sticky client relationships with ample opportunity for up-selling. Like a client purchasing more modules from a vendor raises retention thanks to more unique value enjoyed, this accomplishes that in a different way.

It also seamlessly leverages the commercial platform to cater to industry-specific needs. By-industry models are intuitively named “micro-models.” These boast sector-specific use cases with granular, relevant regulatory compliance help. A financial services model from Palantir, for example, may specialize in assessing credit risk or fraud detection.

Palantir Apollo provides continuous integration and continuous delivery (CI/CD) to automate software package building and deployment. It’s a foundational piece of the firm’s ability to collect, utilize and drive value from broad data ingestion. It’s also how Palantir can help operationalize these learnings to introduce valuable products. It rips on other software firms for (it says) building “slide decks” rather than matching this real-world utility. Apollo ties very closely into Foundry and Gotham as a software enabler for both platforms.

AIP 101:

In the realm of GenAI and Agentic AI, Palantir is not playing the GenAI game of building the biggest model or buying the most GPUs to have the largest infrastructure footprint. It simply gives clients the tools and integrations needed to build apps for their own, more powerful use cases. It also has some products for model customization, along with a large roster of 3rd-party large language model (LLM) integrations. And while that’s absolutely true, where it shines brightest in GenAI is as a leader in GenAI application monetization.

Its most exciting product is called Artificial Intelligence Platform (AIP). This is a highly intricate automation and AI app-building layer that complements Foundry and Gotham perfectly. The company compares AIP to what public cloud vendors did for compute and workload modernization. AWS, Azure, Google and Oracle provided the environment, tools, storage, security and maintenance needed to grow compute capacity without managing it yourself. This made migrations and adoption the rational decision. AIP attempts to do the same thing in terms of pushing enterprises to build and use GenAI applications. This fully manages expedited product creation for client deployment. It allows for open collaboration between software developers, data scientists, models and project managers to ensure effective work. It directly supports Foundry and Gotham by uplifting and augmenting potential use cases to “extract value from GenAI models.” And it does so in a quite compelling way that can craft tools on a by-customer basis.

Considering the lack of finite and structured end products stemming from AIP, I think it helps to hear about some examples of what clients are doing with it:

- Turning inbound emails into automated inventory decisions.

- Automating healthcare documentation for claims.

- The Department of Defense (DoD) is using it to shrink app creation time from hours to seconds.

As leadership will tell you, AIP isn’t just another dime-per-dozen chatbot. It’s an aggregator of data, tools and services needed to actually build valuable apps and to embrace GenAI. It’s how Lowe’s cut overdue task rate by 75% and how General Mills saves $14 million a year in expenses. This is how Associated Materials is raising on-time delivery rate from 40%-90%, how Trinity Rail cut $30 million in annual CapEx and how Mount Sinai found $13 million in new revenue opportunities. It’s how the U.S. government cut critical intelligence sharing processes to 3 days to 3 hours. The list goes on and on. AIP is where jumbled data, processes and ideas turn into the operationalized, actionable creation of GenAI products.

Initial go-to-market for AIP has been its “bootcamps” where it hosts events to provide hands-on support and “get clients from 0 to use case in 5 days. It has more recently begun to build out an external sales team to support this segment’s momentum. AIP progress is most noticeable in its impressive U.S. Commercial results.

“We are delivering the operating system for the modern enterprise in the era of AI.”

Co-Founder/CEO Alex Karp

More Products to Know:

- Operation Warp Speed is a modern industrial operating system (OS) that equips companies and governments with cutting-edge enterprise resource planning (ERP), product lifecycle management (PLM) and a manufacturing execution system (MES). It’s a fully managed way to rapidly allow manufacturers to fix how they build things. This is how Palantir plans to help “reindustrialize” the United States and ensure we build everything we need here.

- FedStart is Palantir’s accreditation program for FedRAMP certifications needed to sell software to the government. It shrinks the time and cost it takes to secure this status and makes Palantir more of an ally vs. an enemy for other software companies.

b. Key Points

- Elite quarter & guidance.

- Superb AIP momentum.

- Business is booming everywhere besides Europe.

c. Demand

Overall Demand:

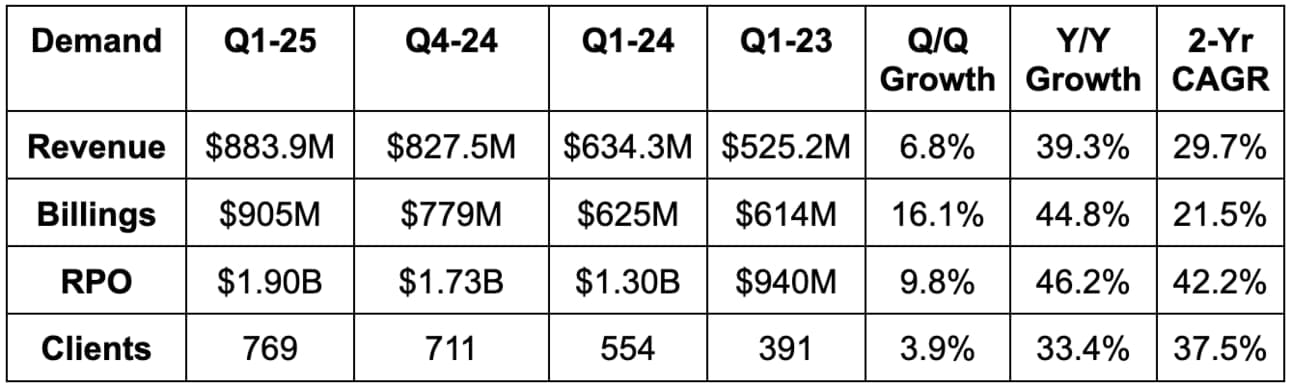

- Beat revenue estimates by 2.4% & beat guidance by 2.8%.

- Beat billings estimates by 12.6%.

- Beat customer count estimates by 19.

- Closed 139 contracts over $1M in value vs. 129 Q/Q 104 2 quarters ago.

- Closed 51 contracts over $5M in value vs. 58 Q/Q & 36 2 quarters ago.

- Cosed 31 contracts over $10M in value vs. 42 Q/Q & 16 2 quarters ago.

Forward-Looking Demand Signals:

- Total contract value (TCV) booked rose 66% Y/Y vs. 42% Y/Y growth last quarter.

- Remaining deal value (RDV) rose 45% Y/Y vs. 40% Y/Y growth last quarter.

- Beat remaining performance obligation (RPO) estimates by 24%.

Segment Demand:

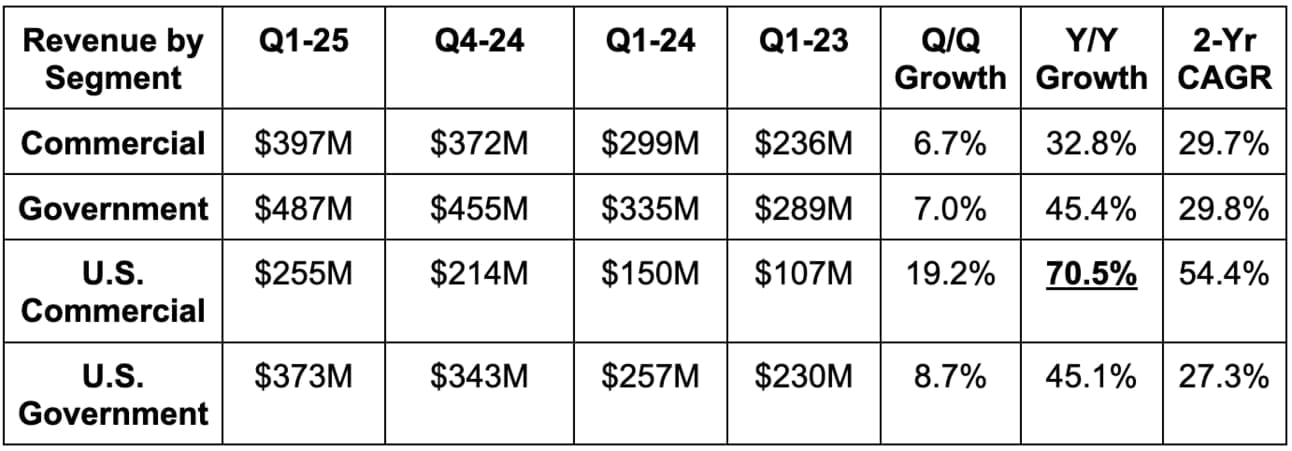

- Beat U.S. commercial revenue estimates by 6.7%.

- Beat U.S. government estimates by 4.2%.

- Overall commercial revenue missed estimates by 0.7%.

- Overall government revenue beat estimates by 6.6%.

More stats on U.S. commercial Demand:

- Highest TCV booked quarter for the segment, with 183% Y/Y growth.

- RDV for the segment rose 127% Y/Y to $2.32B.

- Deal volume doubled Y/Y.

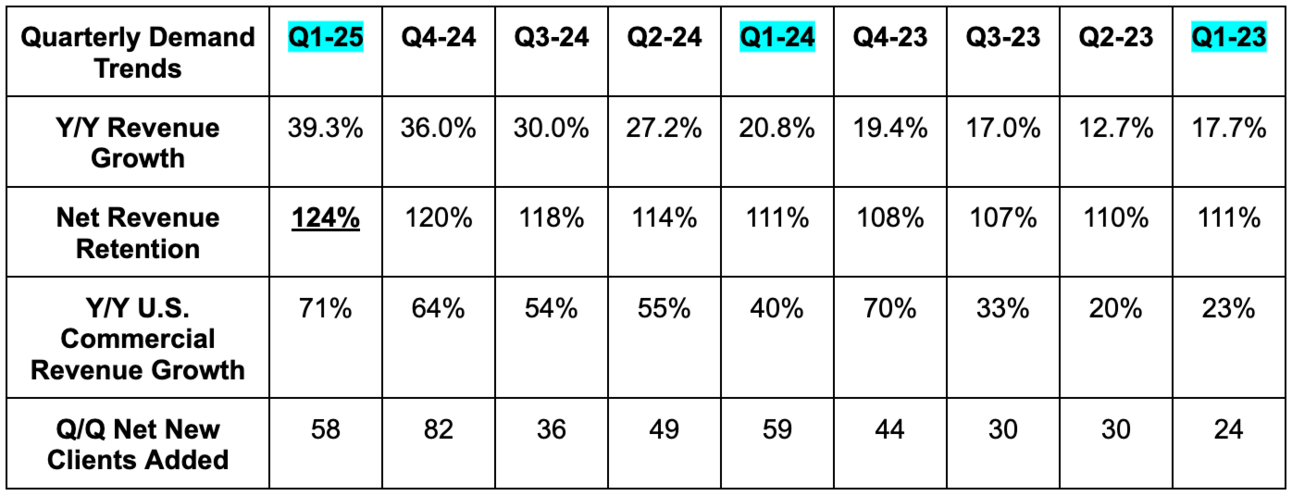

Its existing top 20 customers grew revenue by 26% Y/Y. This helped net revenue retention (NRR) climb to an impressive 124%. Very few companies are delivering this type of Q/Q NRR improvement in this market. Massive billings and RPO beats, as well as rapid TCV and RDV growth, bode extremely well for forward-looking demand.